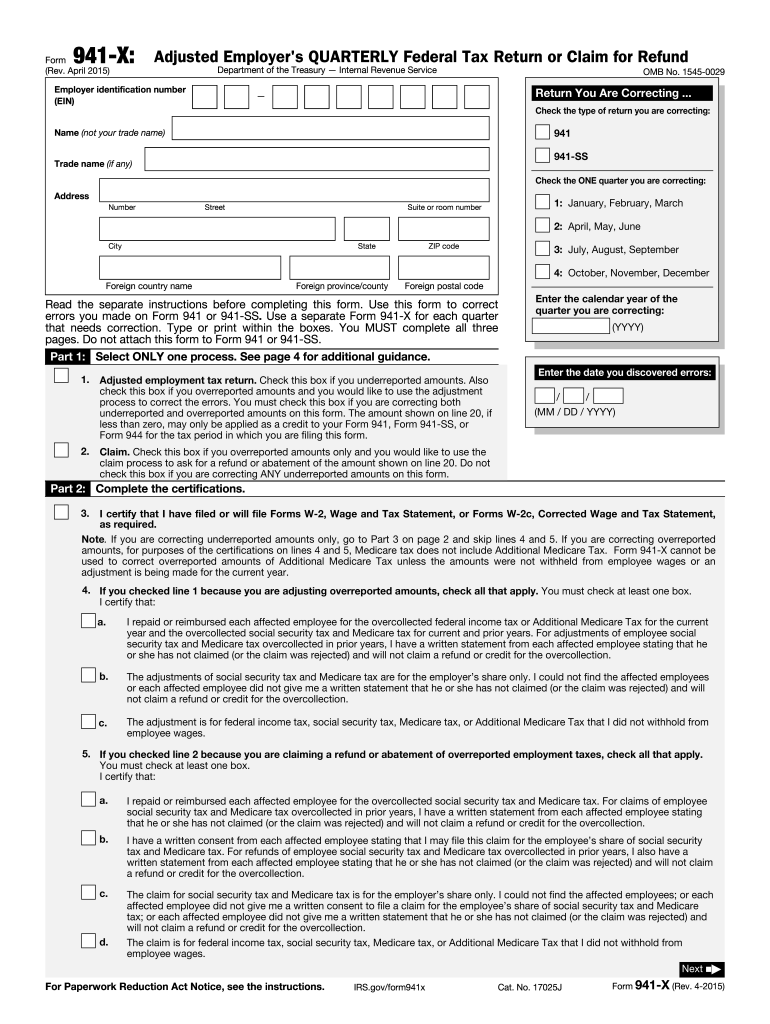

Definition and Purpose of Form 941-X

Form 941-X, officially known as the Adjusted Employer’s Quarterly Federal Tax Return or Claim for Refund, is used by employers to correct errors made on previously filed Forms 941 or 941-SS. It allows employers to amend errors related to Social Security taxes, Medicare taxes, and federal income tax withholding. This form is crucial for addressing discrepancies in reported employment tax obligations after the original filing to ensure compliance with federal tax requirements.

How to Use Form 941-X

To use Form 941-X effectively, identify the specific errors on your previously filed Form 941 or 941-SS. Determine whether the corrections involve underreported or overreported taxes. Complete the appropriate sections of Form 941-X for adjustments and provide a detailed explanation of the changes. The revisions should include the correct amounts as well as the reasons for the discrepancies. Employers must ensure they maintain documentation supporting the adjustments in case of IRS queries.

Common Correction Scenarios

- Underreported Taxes: Adjustments for mistakenly underreporting Social Security and Medicare taxes.

- Overreported Taxes: Claiming refunds for overreported amounts originally paid.

- Wage Miscalculations: Errors in calculating total wages, tips, and other compensations subject to withholding.

Steps to Complete Form 941-X

Form 941-X requires meticulous attention to detail. Here’s a rundown of the steps involved:

- Gather Information: Use your original Form 941 to identify specific errors.

- Refine Details: Correct each line item on Form 941-X to reflect accurate information.

- Include Explanations: Provide comprehensive explanations for each line of correction.

- Calculate Adjustments: Use the form to compute tax adjustments and any applicable refunds.

- Sign and Date: Ensure form credibility by signing and dating the completed form.

Important Terms Related to Form 941-X

Understanding the terminology used in Form 941-X is essential:

- Adjustment: Changes made to the originally reported figures on Form 941.

- Overpayment: Excess amounts paid that can be refunded or credited to future payroll tax liabilities.

- Certification: Employer’s affirmation of the accuracy of the adjustments.

- Error Type: Specifies whether the correction is for overreported or underreported amounts.

Key Elements of Form 941-X

Form 941-X comprises several vital segments that facilitate error correction:

- Part 1: involves basic employer information and specifies the quarter and year for which corrections are being made.

- Part 2: allows detailing of the adjustments by category (e.g., Social Security, Medicare, withheld income tax).

- Part 3: focuses on the explanations for adjustments, requiring concise and clear input about why changes are needed.

Legal Use and Compliance for Form 941-X

Form 941-X is governed by federal tax laws and must be used in accordance with IRS guidelines. Proper filing ensures that employers rectify previous inaccuracies to comply with payroll tax obligations. It's essential that corrections are made promptly upon discovery of errors to avoid penalties and interest that can accrue for late or incorrect filings. The IRS mandates retaining supporting documentation for a minimum of four years.

IRS Guidelines for Filing Form 941-X

The IRS provides specific guidelines for filing Form 941-X:

- Corrections must be filed within three years of the date the original return was due, or within two years of the date the tax was paid, whichever is later.

- The form must be filed for each quarter in which errors occurred, irrespective of whether multiple corrections are related.

- Documentation accompanying Form 941-X, including pay records and jurisdictional information, should be thorough and well-organized to support the accuracy of claims.

Filing Deadlines and Important Dates

Employers must adhere to strict filing deadlines to ensure penalty-free correction of errors. Familiarize yourself with these timelines:

- Three-Year Period: File corrections within three years from the due date of the original Form 941.

- Two-Year Rule: If taxes were overpaid, corrections must be submitted within two years of the payment.

Understanding these deadlines is crucial; missing them can lead to forfeiture of your right to claim refunds.

Required Documentation for Form 941-X

Documentation is key when filing Form 941-X:

- Original Form 941 or 941-SS: Use as a reference for corrections.

- Payroll Records: Clearly signify where errors originated for precise adjustments.

- Supporting Evidence: Include any documents that validate the need for amendments, such as corrected W-2s, pay stubs, or employment agreements.

Maintaining thorough records ensures that any changes made are well-supported in case of IRS audits or inquiries.

Through careful adherence to these guidelines and a precise understanding of Form 941-X, employers can effectively remedy previous tax filing errors, maintaining compliance and smooth business operations.