Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out Form 200 Local Intangibles Tax Return Rev 7-22 with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open it in the editor.

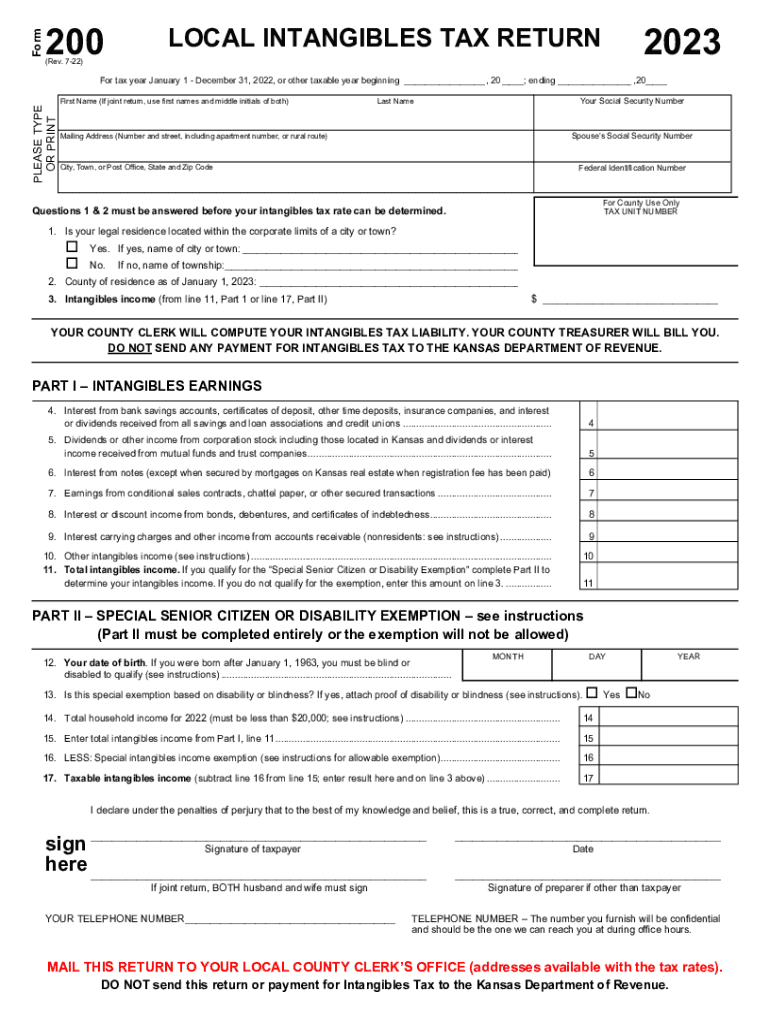

Begin by entering your personal information at the top of the form, including your first name, last name, and Social Security number. If filing jointly, include both names.

Indicate your legal residence by answering questions 1 and 2. Select 'Yes' or 'No' for question 1 and provide the necessary details for both questions.

In Part I, report your intangibles earnings. Fill in each line with the appropriate income amounts from various sources such as bank interest and dividends.

If you qualify for the special senior citizen or disability exemption, complete Part II entirely to determine your exempt amount.

Review all entries for accuracy before signing and dating the form at the bottom. Ensure that both spouses sign if applicable.

Finally, submit your completed form to your local County Clerk’s office by April 15, ensuring you do not send it to the Kansas Department of Revenue.

Start using our platform today to easily fill out and manage your Form 200!

Fill out Form 200 Local Intangibles Tax Return Rev 7-22 The intangibles tax is a local tax levied on gross ea online It's free

See more Form 200 Local Intangibles Tax Return Rev 7-22 The intangibles tax is a local tax levied on gross ea versions

We've got more versions of the Form 200 Local Intangibles Tax Return Rev 7-22 The intangibles tax is a local tax levied on gross ea form. Select the right Form 200 Local Intangibles Tax Return Rev 7-22 The intangibles tax is a local tax levied on gross ea version from the list and start editing it straight away!

Dec 31, 2022 The intangibles tax is a local tax levied on gross earnings received from intangible property such as savings accounts, stocks, bonds, accounts

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.