Definition and Purpose of Tax Relief for Spouses by the IRS

Tax relief for spouses by the Internal Revenue Service (IRS) primarily refers to specific provisions that allow individuals filing jointly to address past-due debts attributed to one spouse. The form most associated with this relief is the Injured Spouse Allocation, also known as Form 8379. It helps ensure that one spouse can claim their portion of a tax refund, shielding it from being automatically applied to obligations such as child support, student loans, or other federal debts owed by the other spouse. This form of tax relief is essential for promoting fairness when one partner's financial obligations do not impact the other's tax standing.

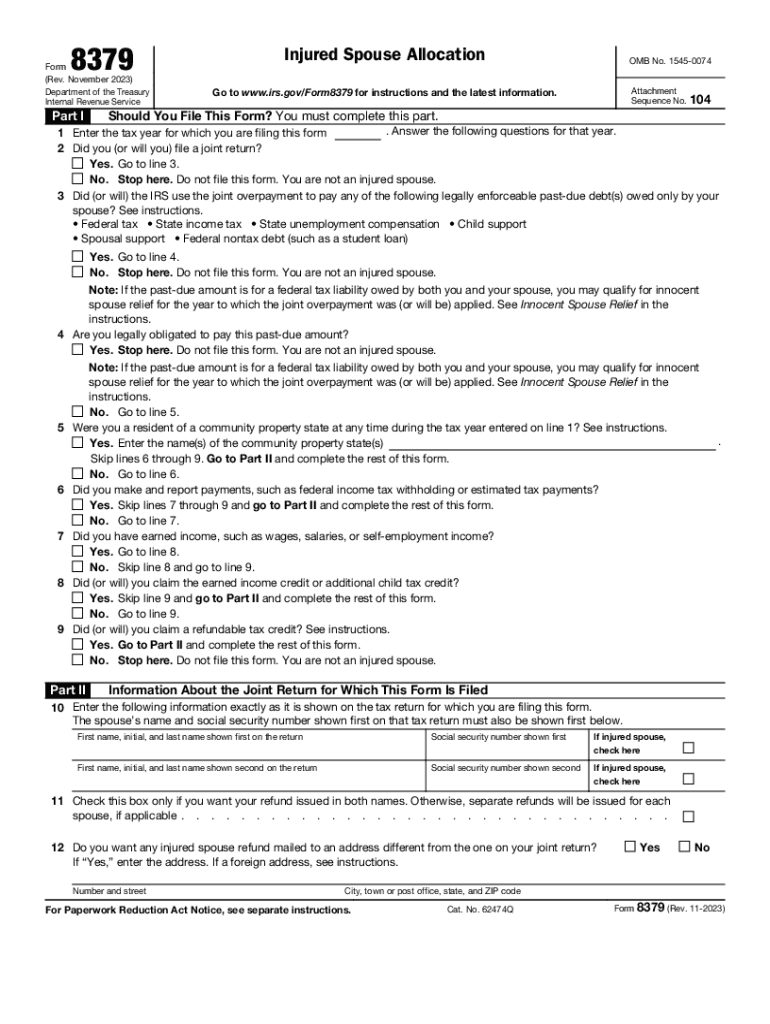

How to Use Form 8379 for Tax Relief

Form 8379 is straightforward to use, provided the instructions are followed meticulously. It is typically filed together with a joint tax return if it is suspected that a refund might be seized to cover the past-due debts of one spouse. The form can be submitted separately if a later need arises. Importantly, you should complete sections detailing income earned and deductions attributed to each spouse, as these are crucial for determining the allocation of a refund. Once filled, the form should be sent to the IRS, either electronically or through the post, depending on the submission of the original tax return.

Steps to Complete Form 8379

- Obtain the Form: Access Form 8379 from the IRS website or through tax preparation software that supports this function.

- Gather Necessary Information: Include social security numbers, income details, and specifics on the debt leading to the refund adjustment.

- Complete Sections for Each Spouse: Thoroughly fill out income and deductions related to both spouses, ensuring accuracy.

- Review and Sign: Double-check all information for completeness and have the appropriate spouse sign the form.

- Submit with Returns or Later: File Form 8379 with your joint tax return or separately, as needed. Keep a record of submission for tracking purposes.

Eligibility Criteria for Injured Spouse Tax Relief

To qualify for the injured spouse relief, the non-debtor spouse must have earned income reported on a joint tax return and contributed to tax entries such as federal income tax withholding. This relief is applicable only when a joint refund compensation might be used to settle debts solely attributable to the other spouse. It is crucial to recognize that those seeking relief must file the form proactively for each tax year affected by potential refund offsets.

Key Elements of Form 8379

- Personal Information: Social Security Numbers and identification of both spouses.

- Income Allocation: Detailed segregation of income earned by each spouse to assist in proper allocation of refund portions.

- Deductions and Credits: Specific entries relating to withholdings attributable to each spouse, such as child tax credits or earned income credits.

- Debt Identification: Clear indication of which debts necessitate the refund offset and which do not pertain to both parties.

IRS Guidelines and Procedures

The IRS sets guidelines to ensure Form 8379 is aptly processed. Filing a joint return by the due date automatically extends the eligibility to apply for injured spouse allocation. When completing the form, be sure to abide by the IRS instructions, ensuring all boxes are checked and signatures are included where required. The IRS will communicate regarding processing times and any additional information required after submission.

Common Scenarios for Filing

Individuals married to partners with significant school loans or unpaid child support often use Form 8379. This is particularly seen when one spouse enters the marriage with existing federal liabilities that do not pertain to the joint financial responsibilities of the couple. Understanding these scenarios helps determine when filing for relief is warranted.

Penalties for Non-Compliance and Missed Claims

There are no strict legal penalties for failing to file Form 8379. However, not filing means forfeiting the protection of your tax refunds from being used to offset the other spouse's debts. To avoid permanent loss of tax refunds that one is entitled to, ensure timeliness in the filing of Form 8379 if applicable.

State-Specific Guidelines and Differences

While Form 8379 is a federal tax provision, state-level variations may exist regarding how states handle joint tax returns and related liabilities. Taxpayers should consult guidance specific to their state or a tax professional familiar with state tax laws to ensure compliance and full relief potential.

Digital Versus Paper Submission

Form 8379 can be filed both electronically and in paper format. Many taxpayers find electronic filing through IRS-approved software or services more efficient, with faster processing times. For those who prefer traditional methods or are unable to file electronically, paper submission remains a viable option, albeit with longer processing periods.