Definition and Meaning

The Form 1099-DIV is used primarily in the United States to report dividends, distributions, and certain financial transactions. Taxpayers and businesses utilize this form to report income from stocks and mutual funds to the Internal Revenue Service (IRS). It serves as a crucial instrument for ensuring accurate tax calculations, reflecting earnings such as ordinary dividends, qualified dividends, and capital gain distributions. Financial institutions, investment firms, or brokerage houses typically issue this form, providing both taxpayers and the IRS with vital information about a recipient's investment income.

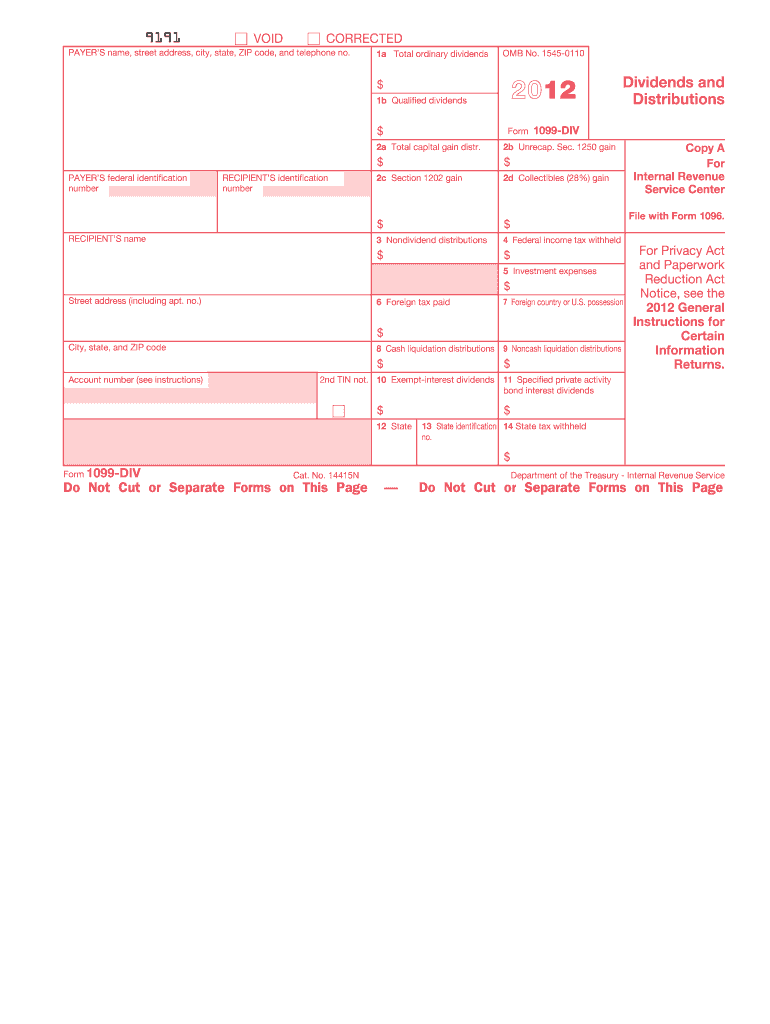

How to Use the 2-DIV Form

The 2-DIV form is utilized to report dividend income and any capital gains distributions received during the 2012 tax year. Recipients of this form should:

- Ensure all reported amounts match their financial records.

- Include the financial details on their individual income tax return, particularly on the Schedule B of Form 1040, if applicable.

- Verify the details for accuracy, such as dividend amounts, qualified dividends, federal income tax withheld, and any foreign tax paid.

- Maintain a copy of the form for their records. This can be crucial for future audits or amendments.

Key Elements of the 2-DIV Form

Form 1099-DIV includes several key components critical for accurate tax reporting:

- Box 1a: Reports total ordinary dividends paid.

- Box 1b: Indicates qualified dividends, which are taxed at a lower rate.

- Box 2a: Details total capital gain distributions.

- Boxes 2b to 5: Provide information on specific elements such as unrecaptured Section 1250 gain, Section 1202 gain, and non-dividend distributions.

- Box 6: Reports foreign tax paid on dividends.

- Box 7: Documents the foreign country or U.S. possession involved.

Understanding these elements is pivotal for correctly preparing tax returns.

Steps to Complete the 2-DIV Form

To complete Form 1099-DIV efficiently:

- Obtain the form from the IRS or a tax software provider.

- Enter the financial institution's information in the payer's section.

- Fill in the recipient's details accurately, including taxpayer identification number.

- Enter all dividend and distribution details in the respective boxes.

- After filling out, review all entered information for accuracy.

- Duplicate the form for both the recipient and IRS submission.

Who Typically Uses the 2-DIV Form

Individuals and entities dealing with:

- Brokerage and investment firms: Need to issue these forms to report dividends to clients.

- Taxpayers receiving dividends and distributions: Use this to report investment income to the IRS.

- Accountants and tax preparers: Assist clients in filing accurately with these details.

Form Submission Methods: Digital vs. Paper Version

The Form 1099-DIV can be submitted in various formats:

- Digital Submission: Efficient and preferred by the IRS through the IRS FIRE system.

- Paper Submission: Traditional method, involves mailing a physical copy of the form to the IRS by the specified deadline.

Both methods require adherence to guidelines ensuring the form’s accuracy and completeness.

Filing Deadlines and Important Dates

- Recipient Copy: Must be furnished to payees by January 31 of the following tax year.

- IRS Submission: Due by February 28 if filed on paper or March 31 if filed electronically.

- Late submissions: Can result in penalties, making awareness of deadlines crucial for compliance.

Penalties for Non-Compliance

The IRS enforces penalties for incorrect or late filing of Form 1099-DIV, which vary based on the degree of non-compliance and the timeliness of correction:

- Late filing without reasonable cause can incur fines starting at $50 per information return.

- Incorrect information that leads to discrepancies between what was reported and what should have been reported can lead to additional scrutiny and fines.

To avoid these penalties, businesses and taxpayers must diligently adhere to the reporting guidelines and deadlines associated with Form 1099-DIV.