Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out fp 161 2012 form with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the fp 161 2012 form in the editor.

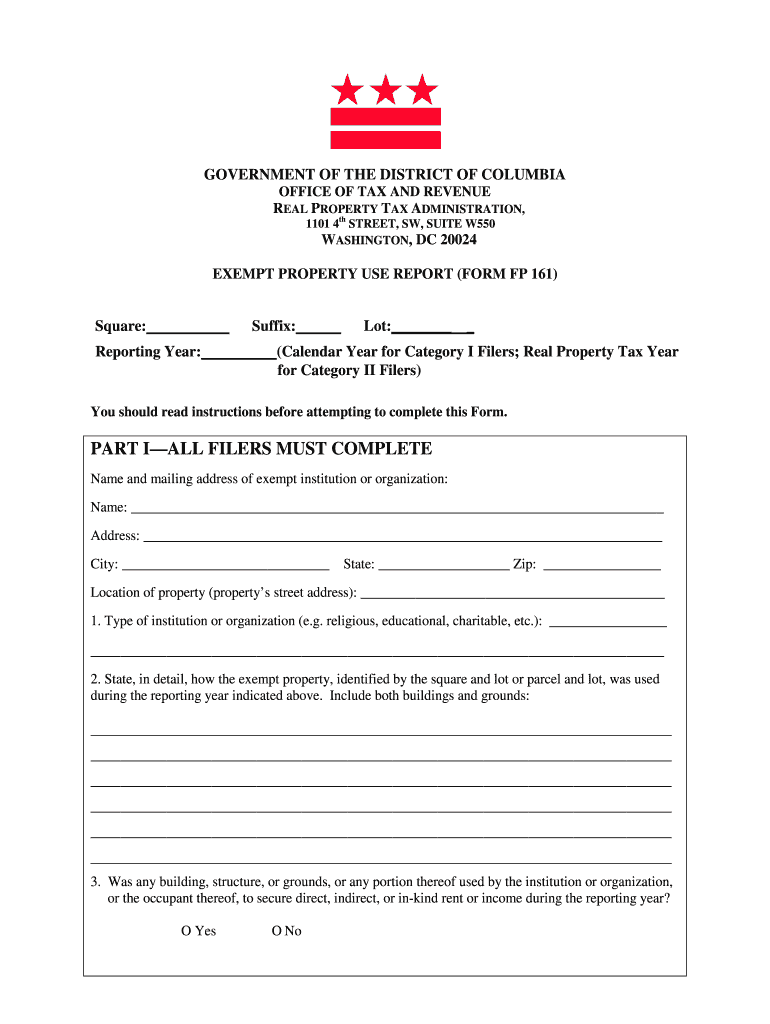

Begin by filling in the 'Square', 'Suffix', 'Reporting Year', and 'Lot' fields at the top of the form. Ensure accuracy as this information is crucial for proper identification.

In Part I, provide the name and mailing address of your exempt institution or organization. Be thorough to avoid any delays in processing.

Detail how the exempt property was used during the reporting year in section 2. Include specifics about both buildings and grounds to comply with requirements.

Answer questions regarding rental income in sections 3 and 3a, if applicable. Provide clear details about any income generated from the property.

Complete sections regarding changes in property use or structural modifications since the previous reporting year, ensuring all questions are answered fully.

For Category II filers, complete Part II by identifying relevant provisions of law and describing community benefits provided during the reporting year.

Finally, sign and date the affidavit section to certify that all information is true and complete before submitting your form.

Start using our platform today for free to streamline your fp 161 2012 form completion!

Fp 161 2012 form pdfFp 161 2012 form pdf downloadFp 161 2012 form downloadFp 161 2012 form instructionsFp 161 2012 form onlineDistrict of columbia real property recordation and transfer tax formDistrict of Columbia FormsDc gov forms

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

Alcohol and Drug Counseling: Addiction Studies Certificate

Nov 14, 2012 Staple the signed Associate of Applied Science/Certificate Revision Signature Page Form to a hard copy of the Certificate Revision Request Form.Read more

form. PFAAs. These precursors include polyfluorinated alkyl substances and a subset of polymer PFAS known as side-chain fluorinated polymers (Washington etRead more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.