Definition & Meaning

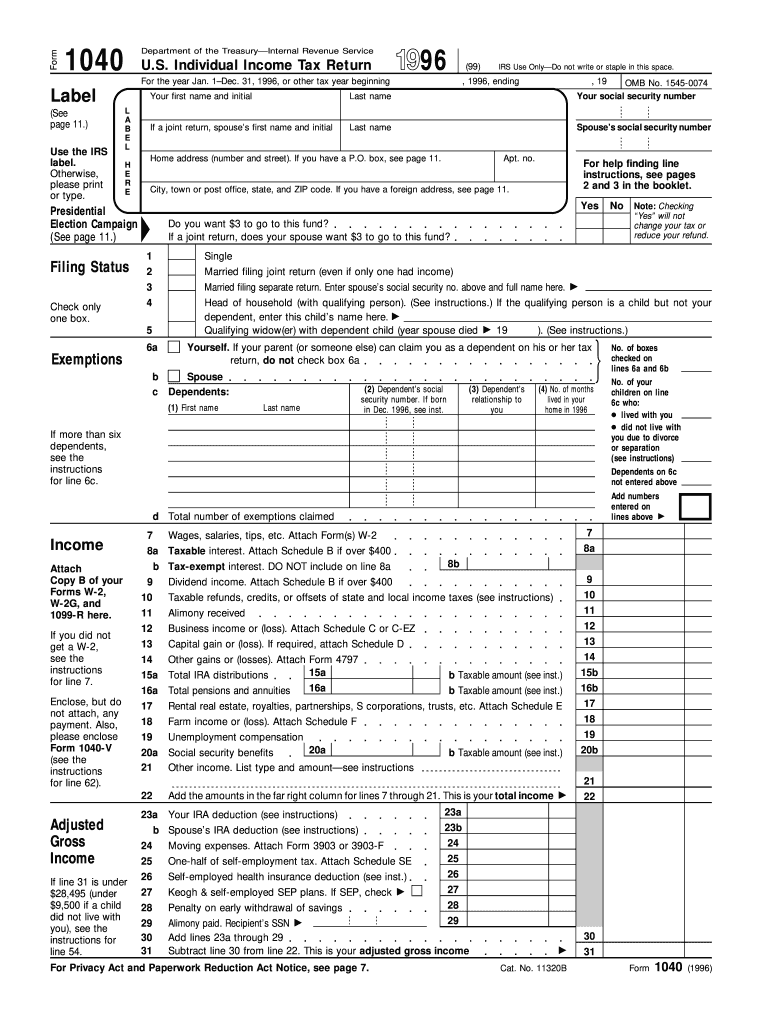

The 1996 U.S. Individual Income Tax Return Form 1040 served as the primary document for taxpayers to report their annual income, claim applicable deductions and credits, and determine their overall tax liability for that year. The form was crucial for ensuring compliance with federal tax obligations and facilitated the accurate calculation of each taxpayer's financial responsibility to the government. Form 1040 included sections for personal information, filing status, various income sources, exemptions, adjustments to income, tax computation, and payment details.

How to Obtain the 1996 Form

Acquiring a copy of the 1996 Form 1040 can be essential for individuals needing to reference their financial information from that year. There are a few methods to obtain a copy:

- IRS Website: The IRS maintains an archive of past tax forms, which can be accessed through their website.

- Request by Mail: Taxpayers can request a copy directly from the IRS by sending Form 4506, "Request for Copy of Tax Return," specifying the 1996 form year.

- Tax Professionals: Consulting a tax professional or accountant who retains copies of previous years' tax filings may also be an option.

Steps to Complete the 1996 Form

Filling out the 1996 Form 1040 required careful attention to detail. Here are the main steps:

- Gather Required Documents: Collect W-2s, 1099s, and any other documents reporting income and potential deductions.

- Personal Information: Fill in your name, address, social security number, and filing status.

- Report Income: Enter income details for wages, dividends, interest, and any other relevant sources.

- Claim Deductions and Credits: Identify eligible deductions and credits that can reduce taxable income.

- Calculate Taxable Income: Subtract allowable deductions from total income to find taxable income.

- Determine Tax Owed or Refund: Use tax tables to compute the tax liability.

- Signature and Submission: Ensure that the form is signed and dated before submitting it to the IRS by mail.

Who Typically Uses the 1996 Form

Form 1040 was utilized predominantly by U.S. residents who earned an income in 1996. It applied to a wide range of taxpayers, including:

- Individuals with Multiple Income Sources: Those receiving different forms of income which needed accurate reporting.

- Self-Employed Individuals: Entrepreneurs and freelancers needing to report business income.

- Investors: Those who received dividends, interest, or capital gains.

- Retirees: Individuals drawing pensions or investment incomes.

Key Elements of the 1996 Form

Understanding the sections of Form 1040 was critical:

- Personal Information: Comprehensive details including filing status.

- Income Section: Various income categories such as salaries, investments, and other revenues.

- Deductions and Credits: These sections allowed taxpayers to adjust their gross income.

- Tax Calculation: Provided framework for computing tax owed based on adjusted income.

- Payments Section: Highlighted any estimated payments and withholding information.

IRS Guidelines

The IRS provided specific instructions for filling out the 1996 Form 1040 to ensure uniformity and accuracy in reporting:

- Filing Instructions: Details on which forms or schedules might add clarity for diverse income sources.

- Deadline Compliance: Guidelines stated the due dates for submitting completed tax forms.

- Supporting Documentation: Recommendations for document retention to substantiate claims and deductions.

Filing Deadlines / Important Dates

Taxpayers using the 1996 Form 1040 had critical deadlines to meet:

- Normal Deadline: April 15th, 1997, was the standard due date for filing.

- Extensions: Taxpayers could file for an automatic extension using Form 4868.

- Payment Schedule: Any taxes owed were due by the April deadline despite extensions.

Penalties for Non-Compliance

Filing inaccuracies or missing deadlines could incur substantial consequences:

- Late Filing Penalties: Fees were calculated based on unpaid tax amounts.

- Underpayment: If taxes were not paid by the deadline, interest accrued daily.

- Audit Risks: Inaccuracies could increase audit probability, leading to further liabilities.

Taxpayer Scenarios (e.g., self-employed, retired, students)

Taxpayers from different backgrounds could face unique reporting challenges:

- Self-Employed Individuals: Needed to manage quarterly estimated payments and business deductions.

- Retirees: Often had to report pension payments and other distributions.

- Students: May have encountered specific education credits or deductions.

Important Terms Related to the 1996 Form

Several essential terms were associated with the 1996 Form 1040 for clarity:

- Gross Income: Total revenue before any deductions or credits.

- Adjusted Gross Income (AGI): Gross income after adjustments reducing taxable amount.

- Taxable Income: Amount on which taxes are calculated post-deductions.

- Standard Deduction: A set amount reducing taxable income relevant to filing status.