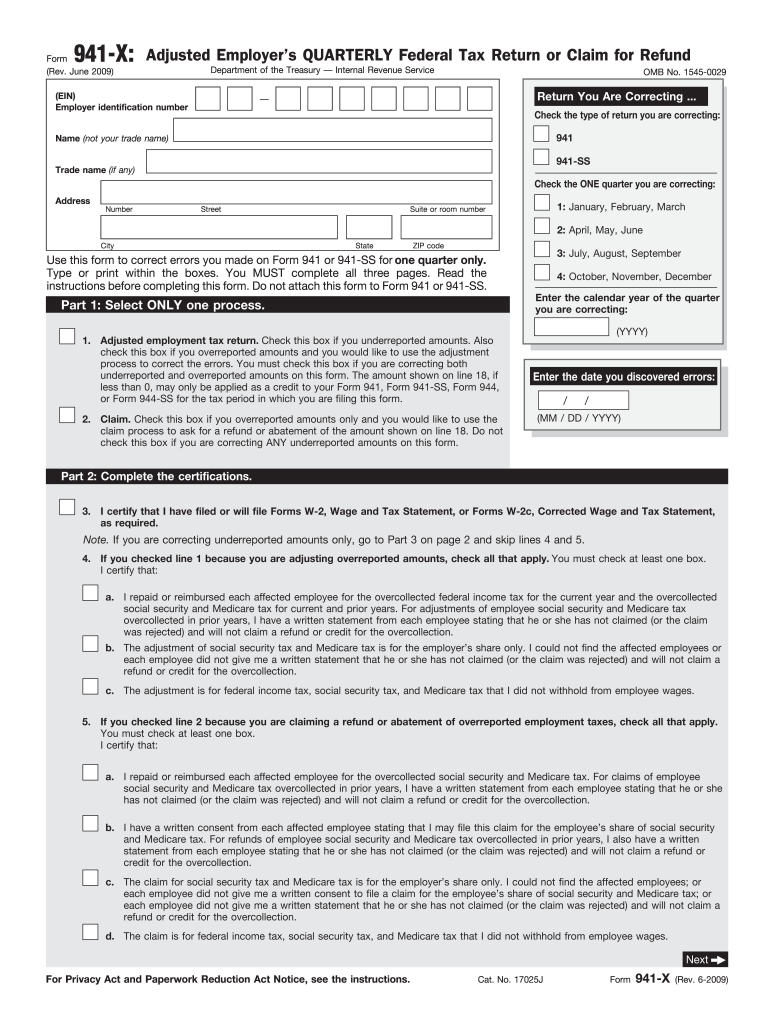

Definition and Purpose of Form 941-X 2009

Form 941-X is employed by employers in the United States to correct errors on the previously filed Employer's Quarterly Federal Tax Return, often referred to as Form 941 or 941-SS. The form targets discrepancies in reported wages, tips, and other compensation. It facilitates the adjustment of taxes, providing employers with a mechanism to correct overreported or underreported amounts, ensuring compliance with federal tax requirements.

- Correcting Errors: The form allows for the amendment of errors related to wages, tips, and withheld taxes. It supports adjustments for Social Security and Medicare taxes, underlining the importance of accuracy in filings.

- Finalization Requirement: Businesses must submit Form 941-X separately from their original returns, emphasizing the need to address corrections promptly and accurately.

Obtaining Form 941-X 2009

Available Sources

Employers can access Form 941-X through various channels to ensure a straightforward filing process. Sources include:

- Internal Revenue Service (IRS) Website: The most direct and up-to-date method for obtaining the form and instructions.

- Tax Professional Services: Accountants and tax advisors can provide the form and offer guidance on correct submission.

- Tax Preparation Software: Integrated into some software packages for ease of preparation and submission.

Digital Access

- PDF Format: Available on the IRS website for download and printing.

- Fillable Forms: From tax software, allowing for electronic completion and filing.

Steps to Complete Form 941-X 2009

- Gather Original Return Information: Begin with information from the originally filed Form 941 to align corrections accurately.

- Indicate Filing Date: Clearly state the quarter for which you are correcting errors.

- Identify Correction Type: Specify whether the error pertains to wages, tips, withheld taxes, or a combination thereof.

- Detail Corrections: Use the provided sections to outline the original and corrected figures, ensuring clarity and accuracy.

- Certify and Sign: The form must be signed by the authorized person, certifying the truth and completeness of the corrections.

- Attach Supporting Documents: If applicable, include documentation that justifies and explains the corrections made.

Why Use Form 941-X 2009

Compliance and Corrections

Businesses utilize Form 941-X to maintain federal compliance and ensure correct tax reporting. Common reasons include:

- Reconciliation: Adjusting discrepancies between payroll records and reported figures.

- Prevention of Further Penalties: Correcting errors expediently to avoid potential fines for inaccurate filings.

Financial Adjustments

- Refunds or Credits: Correcting overreported amounts allows businesses to apply for refunds or tax credits, positively impacting financial statements.

Who Typically Uses Form 941-X 2009

Eligible Entities

Form 941-X is widely used across various business types that require prior tax return corrections. Common users include:

- Small to Large Businesses: Any business entity that electronically or manually processes payroll and tax withholdings.

- Tax Professionals: Accountants and payroll specialists managing tax compliance for clients.

- Human Resources Departments: Managing payroll discrepancies and ensuring correct withholding calculations.

Industry Examples

- Hospitality: Adjusting for tipped employee discrepancies.

- Manufacturing: Correcting wage calculations in fluctuating labor scenarios.

Important Terms Associated with Form 941-X 2009

Familiarization with key terminology aids in understanding the form and facilitating accurate completion:

- Overreported Wages: Amounts initially reported as greater than what was actually paid.

- Underreported Taxes: Instances where not all required tax amounts were initially included.

- Certification: Legal assertion of the truthfulness in the reported corrections.

IRS Guidelines for Using Form 941-X 2009

The IRS provides comprehensive guidelines for employers on how to utilize Form 941-X. These include:

- Time Limitations: Corrections must be made within three years of the original due date of the return or within two years of the date the tax was paid, whichever is later.

- Instruction Compliance: Adherence to the official form instructions to ensure the acceptance of corrections.

- Documentation Requirements: Maintaining records supporting each correction is vital for validating changes and responding to IRS inquiries.

Filing Deadlines and Important Dates

Corrective Timelines

Meeting deadline expectations is crucial for the validity of corrections:

- Quarterly Deadlines: Align any corrections with the relevant quarter of the original filing.

- Specific Corrective Deadlines: Follow the IRS guidelines to ensure corrections are made within the allowable period, avoiding any late submission penalties.

Required Documents for Form 941-X 2009 Submission

Essential Attachments

When filing Form 941-X, supporting evidence may be necessary to substantiate the corrections:

-

Payroll Records: Provide detailed payroll data that led to initial reporting errors.

-

Tax Payment Records: Include payment proofs if adjustments affect taxes previously paid.

-

Copies of Original Returns: Retain the original Form 941 filed for cross-reference and clarification of changes made.

-

Financial Statements: If claiming a refund or credit, provide financial documentation that correlates to the corrections.