Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send loan tax rate via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out loan tax with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the loan tax document in the editor.

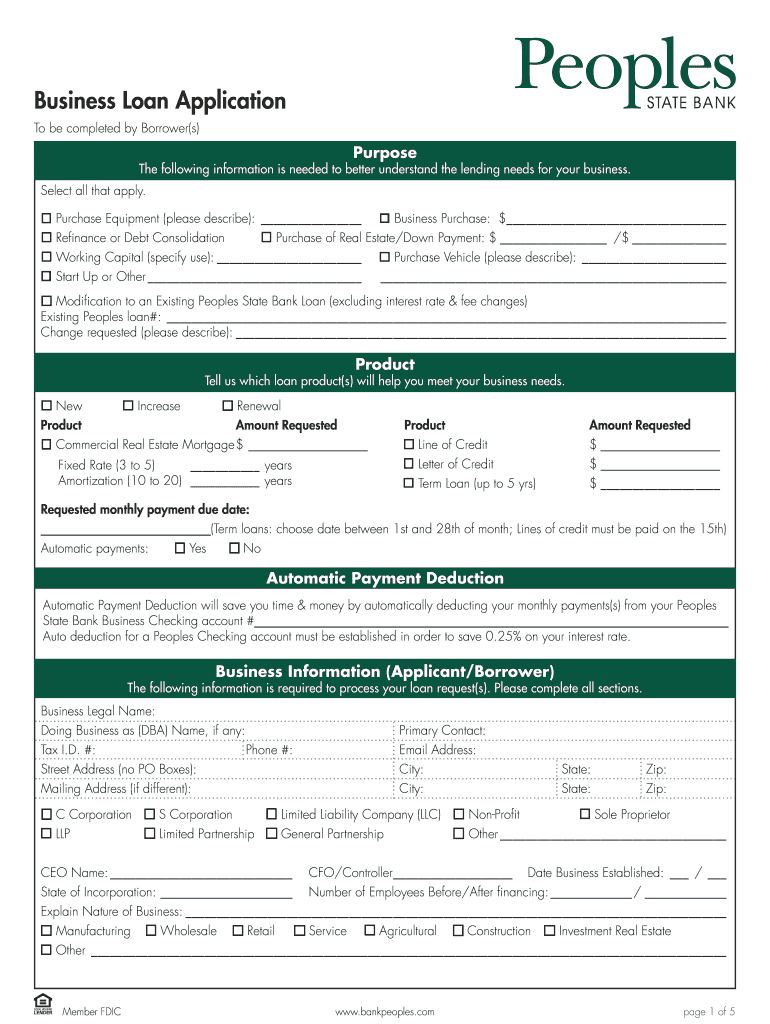

Begin by selecting the purpose of your loan from the options provided. Clearly describe any specific needs, such as equipment purchases or working capital.

In the 'Product' section, indicate which loan products you are interested in and specify the amount requested for each product.

Fill out your business information accurately, including legal name, DBA name, and contact details. Ensure all fields are completed to avoid processing delays.

Provide details about your business obligations and deposit relationships. This includes listing any existing loans and their balances.

Complete the declarations section by answering all questions truthfully. If necessary, provide additional details on a separate page.

Review your entries for accuracy before submitting. Use our platform’s features to save your progress and make edits as needed.

Start filling out your loan tax form today for free using our editor!

The $100,000 De Minimis Exception If the total sum of lending is less than $100,000, the IRS allows you to charge interest based on the lesser of either the AFR rate or the borrowers net investment income for the year. If their investment income was $1,000 or less, the IRS allows them to charge no interest.

What is the 100000 loan exception?

The $100,000 Loophole. With a larger below-market loan, the $100,000 loophole can save you from unwanted tax results. To qualify for this loophole, all outstanding loans between you and the borrower must aggregate to $100,000 or less.

What is the tax on a loan?

Key takeaways Since lenders require you to repay a personal loan, they are considered debt and not taxable income. If a lender forgives some or all of your loan, you may have to pay taxes on the forgiven amount. The IRS allows taxpayers to deduct interest on personal loan funds used for business purposes.

What does a taxable loan mean?

A loan may be taxable if the total amount borrowed exceeds. the limits allowed by the IRS. ➢Limits are based on a variety of criteria, including the present value of. your retirement benefit and any current loans you may have including loan balances with a 457 or 403(b) plan.

How much money can a family member lend you?

Agree On The Amount Being Borrowed Before anything can go into writing, both parties must agree on how much is being borrowed. Theres no legal limit on how much one family member can loan another, but loans over $10,000 will have certain tax requirements, which well look at more closely below.

Related Searches

Loan tax calculatorIs a personal loan tax deductibleStudent loan tax deduction income limitStudent loan interest deduction phase outDo you have to claim student loans on taxesIs a personal loan taxable incomeStudent loan interest deduction 2024Family loan tax implications

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

What are the IRS rules for borrowing money from family members?

Loans are not considered gifts since youre going to get the money back. But the IRS considers money you lend to a family member to be a loan only if you sign a loan agreement, charge interest and try to collect (to the point of hiring a debt collector or taking the borrower to court).

How much tax will I owe on $10,000 in interest income?

So, for example, lets say that you earned $10,000 in interest income and your marginal tax rate is 22% based on your 2025 federal income tax bracket. Using that information, the tax on your savings account interest would generally be $2,200.

Related links

Information on How to File Your Tax Credit from the Maryland

Eligible applicants: Maryland taxpayers who have incurred at least $20,000 in undergraduate and/or graduate student loan debt, and have at least $5,000 in

Student loan interest is interest you paid during the year on a qualified student loan. It includes both required and voluntarily prepaid interest payments.

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.