Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

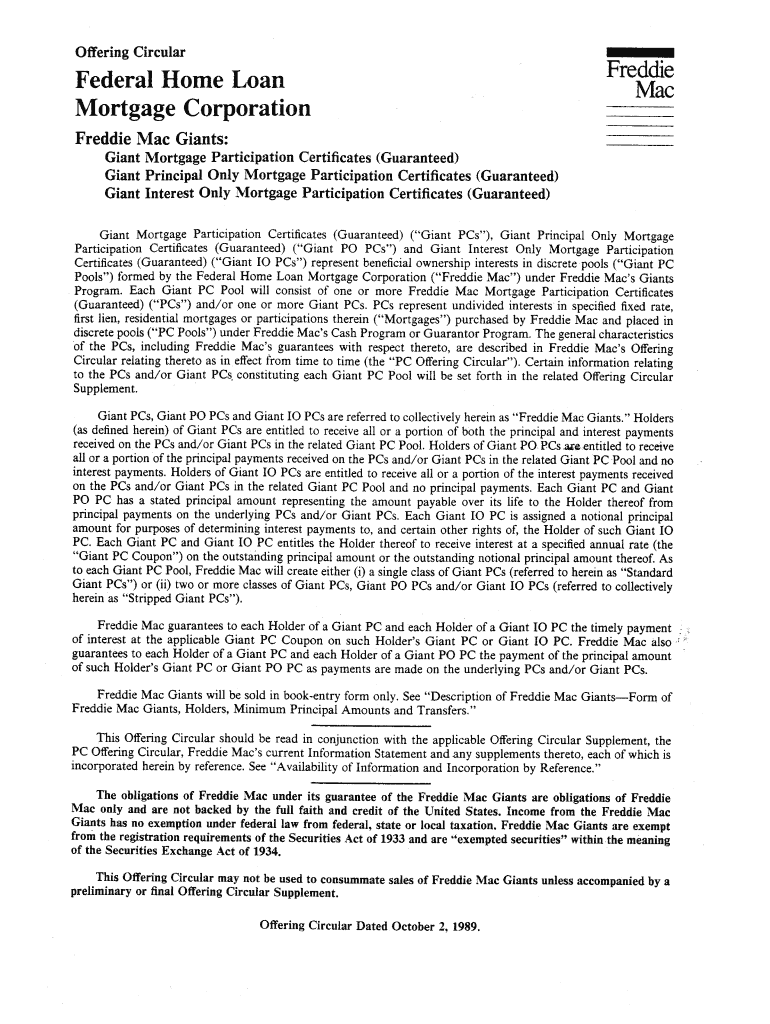

How to use or fill out Federal Home Loan M Fre1C 1,Idai - Freddie Mac with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the Federal Home Loan M Fre1C 1,Idai - Freddie Mac document in the editor.

Begin by entering your personal information in the designated fields. This typically includes your name, address, and contact details. Ensure accuracy for a smooth processing experience.

Next, navigate to the financial information section. Here, you will need to provide details about your income, assets, and liabilities. Use our platform’s tools to easily input numbers and calculations.

Review any additional sections that may require signatures or acknowledgments. Utilize the signing feature to securely sign where necessary.

Finally, save your completed form and export it as needed. You can also share it directly from our platform for further processing.

Start using our platform today for free to streamline your form completion process!

Fill out Federal Home Loan M Fre1C 1,Idai - Freddie Mac online It's free

One of the most notable differences between Freddie Mac loans and FHA loans is the upfront funding fees and mortgage insurance policies. Both the Home Possible and HomeOne Programs do not require an upfront funding fee or mortgage insurance.

What is a Freddie Mac mortgage loan?

Freddie Mac Home Possible mortgages include features that are designed to serve low- and moderate- income borrowers and first-time homebuyers. Features include down payments as low as 3 percent, fixed rates, and reduced mortgage insurance coverage levels.

What are the disadvantages of a Freddie Mac loan?

Freddie Mac Home Possible Pros and Cons ProsCons The program offers competitive rates and fees. The loan must be used for primary residence. You have more flexibility on down payment sources including gifts, employer-assistance programs, secondary financing and sweat equity. There is no flexibility on income limits.1 more row

How to tell if your loan is Fannie Mae or Freddie Mac?

Freddie Mac is a government-sponsored enterprise or GSE, created by the federal government to ensure access to home mortgage credit. Freddie Mac has a statutory mission to provide liquidity, stability, and affordability to the U.S. housing market. Freddie Mac does not make loans directly to homebuyers.

What is the income limit for Freddie Mac HomeOne?

The Freddie Mac HomeOne mortgage is a loan program for first-time homebuyers that lets you purchase a house with just 3% down. Unlike some other low down payment programs for first-time homebuyers, with HomeOne there are no income limits.

Related Searches

Fannie MaeFederal home loan m fre1c 1 idai freddie mac loginFreddie Mac phone numberFreddie Mac addressFreddie Mac vs Fannie MaeFreddie Mac headquartersfreddie mac mclean, va addressIs Freddie Mac a government agency

People also ask

Who qualifies for Freddie Mac loans?

Freddie Mac outlines several eligibility criteria for borrowers including: A credit score of 660 or higher. A debt-to-income rate of 43% or lower. A down payment of 3% Proof of stable employment and income. A combined income for all borrowers of no more than 80% of the areas median income.

Related links

1M tip JM jl airfrrrb | m H Sa TOtXald Today Seminole High School will HOME FOR YOU HOMES 3 bedrooms 1 k 1 baths. Complete and ready (or

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.