Definition & Meaning

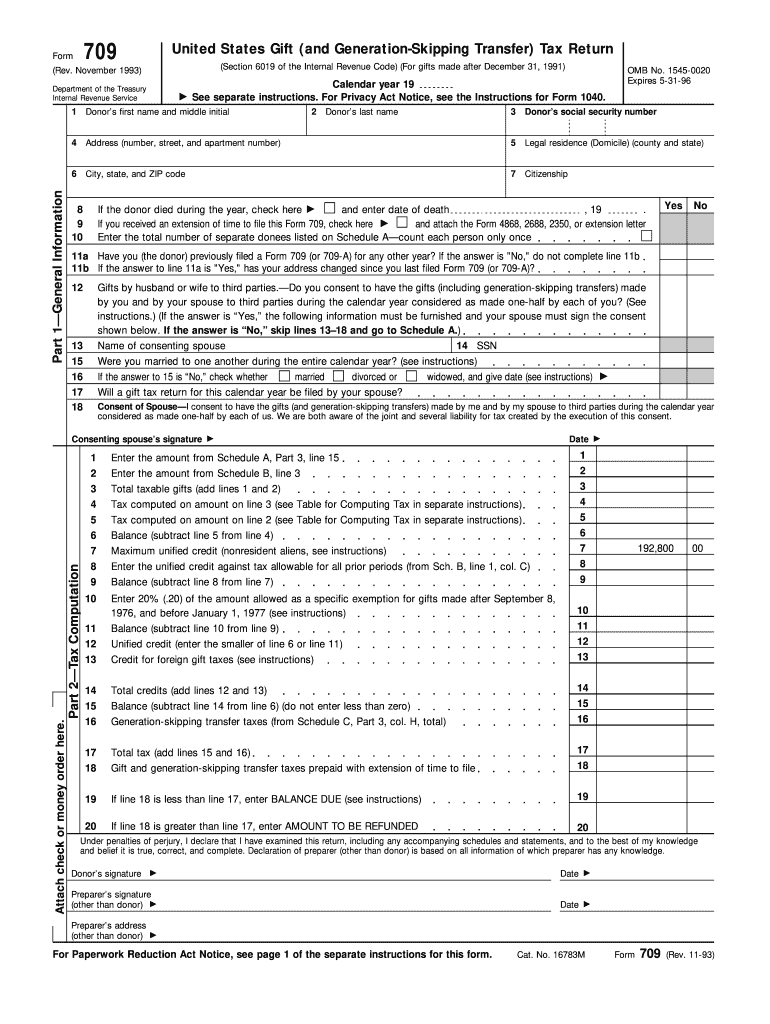

The 1993 Form 709 is the United States Gift and Generation-Skipping Transfer Tax Return form. It is used by individuals to report certain taxable gifts and allocate the generation-skipping transfer (GST) tax exemption to property transferred during the year. This form is particularly relevant for those making significant gifts, as it helps the IRS track gift taxes and ensure compliance with gifting regulations. The 1993 version aligns with tax laws applicable to gifts made after December 31, 1991, maintaining consistency with updated tax guidelines and ensuring proper record-keeping.

Steps to Complete the 1993 Form 709

-

Provide General Information: Enter personal details, including the donor's name, address, and taxpayer identification number.

-

List All Gifts: Document each gift separately in the appropriate sections. Include the recipient's name, the value of the gift, and any relevant descriptions.

-

Calculate Deductions: Specify any applicable deductions, such as marital or charitable deductions, to determine taxable gifts.

-

Compute Taxes: Use the provided tables and schedules to compute the total gift tax liability, considering applicable credits and deductions.

-

Sign and Date the Form: Ensure all details are verified, then sign and date the form to validate its accuracy before submission.

-

Submit with Payment: Attach any required payments and additional documentation before sending it to the IRS by the deadline. Filing late may incur penalties and interest.

Who Typically Uses the 1993 Form 709

The 1993 Form 709 is primarily used by individuals in the United States who have made gifts exceeding the non-taxable annual limit or those involved in generation-skipping transfers. Typical users include:

- High Net-Worth Individuals: To document significant gifts to family members or trusts.

- Estate Planners: To help clients allocate their generation-skipping transfer tax exemptions efficiently.

- Legal and Financial Advisors: To ensure clients comply with gifting and transfer tax regulations.

Filing Deadlines / Important Dates

Form 709 must be filed along with the donor's annual tax return, with the same deadline as individual income tax returns. For the 1993 tax year, this typically means the form should be filed by April 15, 1994, unless an extension is requested. However, it's crucial to be aware that any owed taxes must be paid by this deadline to avoid penalties or interest, even if an extension for filing is received.

IRS Guidelines

According to IRS guidelines, individuals must file Form 709 if they gift more than the annual exclusion amount or engage in taxable generation-skipping transfers. The form captures all relevant details to facilitate tax calculations and ensure compliance with federal tax laws. It is important for individuals to consult the IRS instructions for the 1993 form, as updates may clarify changes or specific scenarios applicable to that year.

Key Elements of the 1993 Form 709

-

Part 1 - General Information: Basic details about the donor and return status.

-

Part 2 - Tax Computation: Sections to calculate the total gift tax liability after deductions.

-

Part 3 - Schedule A: Detailed description and valuation of all gifts made during the year.

-

Part 4 - Schedule B: Areas for specifying deductions and exclusions applied.

Understanding these sections ensures accurate completion of necessary requirements, reducing the risk of audit or penalties.

Required Documents

When filing the 1993 Form 709, several documents are crucial to substantiate the reported information:

- Gift Appraisals: For non-cash gifts, such as real estate or valuable items.

- Proof of Previous Gifts: Documentation of gifts from prior years to verify cumulative totals.

- Contracts or Agreements: Legal documents supporting the terms of complex transfers or gifts.

Providing these documents aids in an accurate assessment and supports claimed deductions or credits.

Penalties for Non-Compliance

Failure to file Form 709, or underreporting the total taxable gifts, can incur significant penalties. These may include interest on unpaid taxes and additional fines calculated as a percentage of the tax liability. In severe cases, intentional noncompliance may lead to criminal charges. Hence, it is essential to complete and file the form accurately and punctually to avoid these repercussions. Consulting with tax professionals for complex scenarios helps mitigate risks associated with non-compliance.