Definition & Meaning

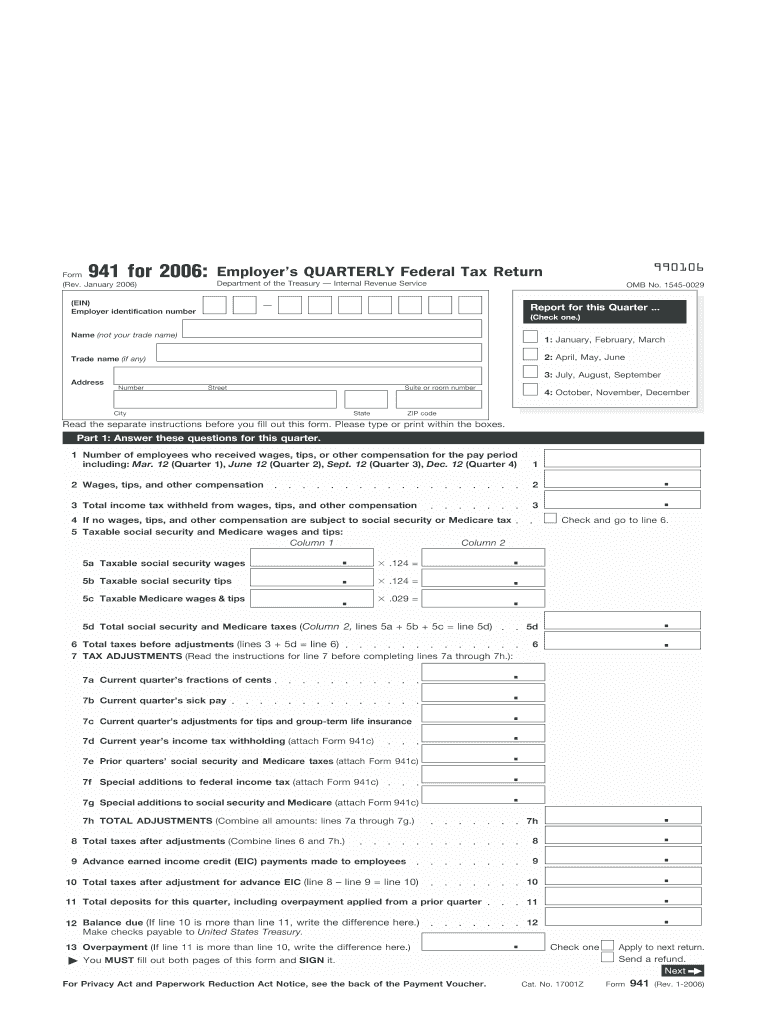

The 2006 Form 941, officially known as the Employer's Quarterly Federal Tax Return, is a critical document used by employers to report wages, tips, and other compensation paid to employees. It details the federal income tax withheld, along with both the employer and employee portions of Social Security and Medicare taxes. This form is issued by the Internal Revenue Service (IRS) and must be filed each quarter by employers to stay compliant with tax regulations. Accurate completion of this form is essential to ensure proper tax reporting and contribution accuracy.

Steps to Complete the 2006 941 Form

-

Gather Required Information: Start by collecting all necessary details, including total wages paid, federal income tax withheld, and Social Security and Medicare taxes. Ensure you have accurate records of employee compensation and tax deductions.

-

Fill in Employer Information: Enter your employer identification number (EIN), business name, trade name, and address. This ensures the IRS can identify your business correctly.

-

Complete Employee Compensation Sections: Report the total wages, tips, and other compensation paid during the quarter. Ensure the Social Security and Medicare wages match your payroll records.

-

Calculate Tax Liabilities: Carefully calculate the total taxes owed, including federal income tax withheld and both employer and employee portions of Social Security and Medicare taxes.

-

Adjust for Deposits Made: Enter the tax deposits already made for this quarter. Ensure these figures match the records to avoid discrepancies.

-

Reconcile and Submit: Double-check the figures for accuracy, ensure totals are correct, and reconcile any discrepancies. Once verified, the form can be submitted either electronically or via mail to the IRS.

Why Should You Use the 2006 941 Form

Filing Form 941 is mandatory for employers as it ensures compliance with federal tax regulations. It provides the IRS with the necessary information to track an employer’s tax responsibilities concerning employee wages. Filing this form correctly helps avoid penalties related to underreporting or failure to pay owed taxes. It also establishes a permanent record of tax liabilities and payments made throughout the year.

Importance of Filing Deadlines

Adherence to filing deadlines is crucial for maintaining compliance. Form 941 must be filed quarterly, with specific deadlines at the end of April, July, October, and January. Late submissions can result in penalties and interest charges from the IRS. Maintaining a consistent filing schedule ensures no gaps occur in reporting and that all tax responsibilities are met on time.

Key Elements of the 2006 941 Form

- Employer Identification Number (EIN): Essential for identifying the reporting business.

- Quarterly Wage and Tax Reporting: Details employee compensation and tax withholdings for the quarter.

- Adjustments and Credits: Accounts for tax credits against the prescribed liabilities, including sick pay and tip conversions.

- Signature Section: Legal affirmation of accuracy and completeness.

IRS Guidelines

The IRS provides comprehensive guidelines for completing Form 941. Employers must adhere to IRS instructions to ensure all fields are correctly filled out and all tax credits are applied appropriately. These guidelines also outline how to adjust for previous mistakes and how to handle overpayments or underpayments.

Penalties for Non-Compliance

Failing to file or filing inaccurately can result in severe penalties from the IRS. These penalties may include fines, interest on unpaid taxes, and potential legal actions. Ensuring timely and accurate filing of the 2006 Form 941 safeguards against these consequences and maintains good standing with tax authorities.

Digital vs. Paper Version

Employers have the option to file Form 941 either digitally or through a traditional paper submission. Digital filing is encouraged due to increased efficiency, quicker processing times, and immediate confirmation of submission. Paper forms remain an option for those without digital access, although processing may take longer.

Software Compatibility

For businesses utilizing accounting software like TurboTax or QuickBooks, compatibility with Form 941 filing is an important consideration. These platforms often provide tools to streamline the data entry, calculation, and submission processes, ensuring accuracy and reducing the chances of errors in the reporting.

Business Entity Types

Form 941 is applicable to a variety of business structures, including LLCs, corporations, and partnerships. Each entity type might have unique reporting needs or tax considerations, making it imperative that the form reflects the correct details pertinent to the business structure in question.