Definition & Meaning

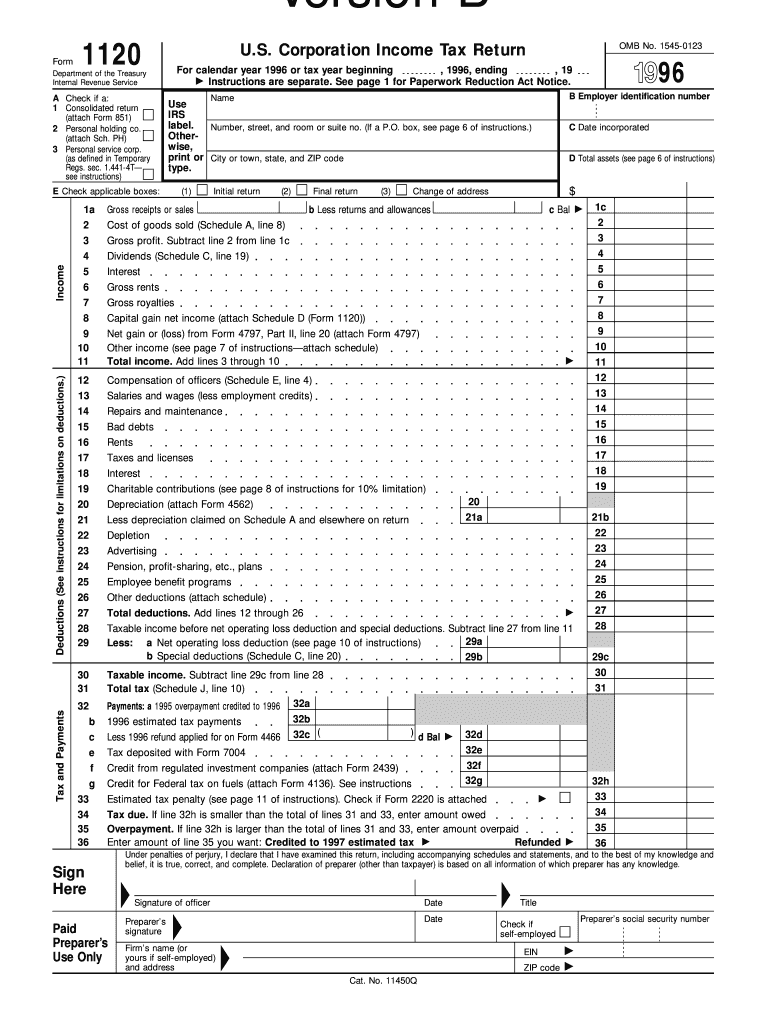

The 1996 Form 1120 is the U.S. Corporation Income Tax Return for the tax year 1996. This form is primarily used by corporations in the United States to report their financial details to the Internal Revenue Service (IRS). It includes sections for reporting income, deductions, and tax computations and requires extensive financial disclosure to determine a corporation’s taxable income and eventual tax liability.

Corporations must complete various schedules within the form, such as Schedule A for the cost of goods sold and Schedule J for tax computation. These sections ensure all sources of income and allowable deductions are accurately documented. Understanding the form's structure and purpose is essential for proper compliance and accurate tax reporting.

How to Use the 1996 Form 1120

Using the 1996 Form 1120 involves systematically completing several sections that record a corporation's financial activities throughout the year. Corporations must provide detailed information on income streams, financial deductions, and other factors that affect their taxable income.

-

Identify Income Sources: Corporations need to document all income sources, including gross receipts and sales, returns and allowances, and other income forms. This provides a comprehensive view of the corporation's earnings.

-

List Deductions: To accurately determine net income, corporations can list applicable deductions, which may include salaries, utilities, and advertising costs.

-

Compute Tax: Carefully apply the tax rates to the net income figure, making use of Schedule J for precise calculations. This ensures that all tax liabilities are correctly assessed and recorded.

-

Complete Additional Schedules: Additional schedules, such as Schedule C for dividends and special deductions, need to be filled out if applicable, based on a corporation's profile.

Key Elements of the 1996 Form 1120

Key elements of this form include:

- Income Section: Where corporations report total income, including sales, rents, and interest.

- Deductions Section: Lists allowable deductions, reducing the taxable income.

- Tax Computation: Schedules like Schedule J help in determining the correct tax owed.

- Balance Sheet: This section provides a snapshot of the corporation’s financial health at the end and beginning of the year.

Accurate completion of these sections is crucial for proper tax compliance and avoiding penalties.

Steps to Complete the 1996 Form 1120

-

Gather Required Information: Before filling out the form, gather all relevant financial documents, such as earnings statements and records of deductions.

-

Fill Out General Information: Complete the top section of the form with the corporation’s name, address, and Employer Identification Number (EIN).

-

Report Income: Document all income in the appropriate sections, ensuring each source is correctly categorized.

-

Claim Deductions: List all deductions the corporation is eligible to claim. Ensure supporting documentation is available in case of an audit.

-

Calculate Taxable Income: Subtract total deductions from the total income to determine the taxable income.

-

Determine Tax Due: Using the IRS tax rate tables, calculate the total tax due.

-

Complete Schedules as Necessary: Fill out any additional schedules that apply to your corporation’s activities.

-

Review and Submit: Double-check all calculations and information before submitting the form. Retain a copy for corporate records.

IRS Guidelines for the 1996 Form 1120

The IRS provides specific guidelines for filling out Form 1120. Corporations should adhere to these rules to ensure compliance:

- Filing Deadline: The form must be submitted by the 15th day of the third month after the end of the corporation’s tax year.

- Extensions: If more time is needed, corporations can file for an extension using Form 7004.

- Accurate Information: Ensure all information is accurate and complete to avoid penalties.

- Attachments: Include all necessary schedules and statements that detail income, deductions, and credits.

Filing Deadlines / Important Dates

The primary deadline for filing the 1996 Form 1120 is the 15th day of the third month following the end of the corporation's tax year. For calendar year corporations, this is generally March 15 of the following year. Timely filing is critical to avoid late fees or penalties.

Corporations unable to meet this deadline may file for an extension, typically granted for an additional six months, by submitting Form 7004. This request should be made before the original due date to ensure compliance.

Required Documents

To correctly complete the 1996 Form 1120, corporations should gather:

- Financial Statements: Income statements, balance sheets, and any audit reports.

- Receipts and Invoices: Documentation for all deductible expenses.

- Previous Year’s Tax Return: For reference and consistency.

- Records of Any Income Sources: To ensure all forms of income are reported.

Having these documents ready ensures a smoother tax filing process and helps in verifying the accuracy of the information entered onto the form.

Penalties for Non-Compliance

Corporations failing to file Form 1120 or pay their taxes on time face potential penalties:

- Late Filing: Penalties are typically a percentage of the unpaid tax per month the return is late.

- Accuracy-Related: For underreported income or significant calculation errors, additional fines may be levied.

- Fraud: Attempting to defraud the IRS with inaccurate information can lead to severe legal consequences.

Ensuring timely filing and accurate documentation helps corporations avoid these penalties, maintain good standing with the IRS, and prevent future complications.

Business Entity Types

The 1996 Form 1120 is primarily for C corporations, which are recognized as separate legal entities from their owners. This form allows such companies to report their income and calculate the federal income tax owed.

- Single-Member LLCs: Typically do not use this form unless they elect to be treated as a corporation for tax purposes.

- Partnerships and S Corporations: Use different forms intended for their specific business structures, such as Form 1065 or Form 1120S.

C corporations must understand their obligations under this form to accurately reflect their financial activities and liabilities to the IRS.