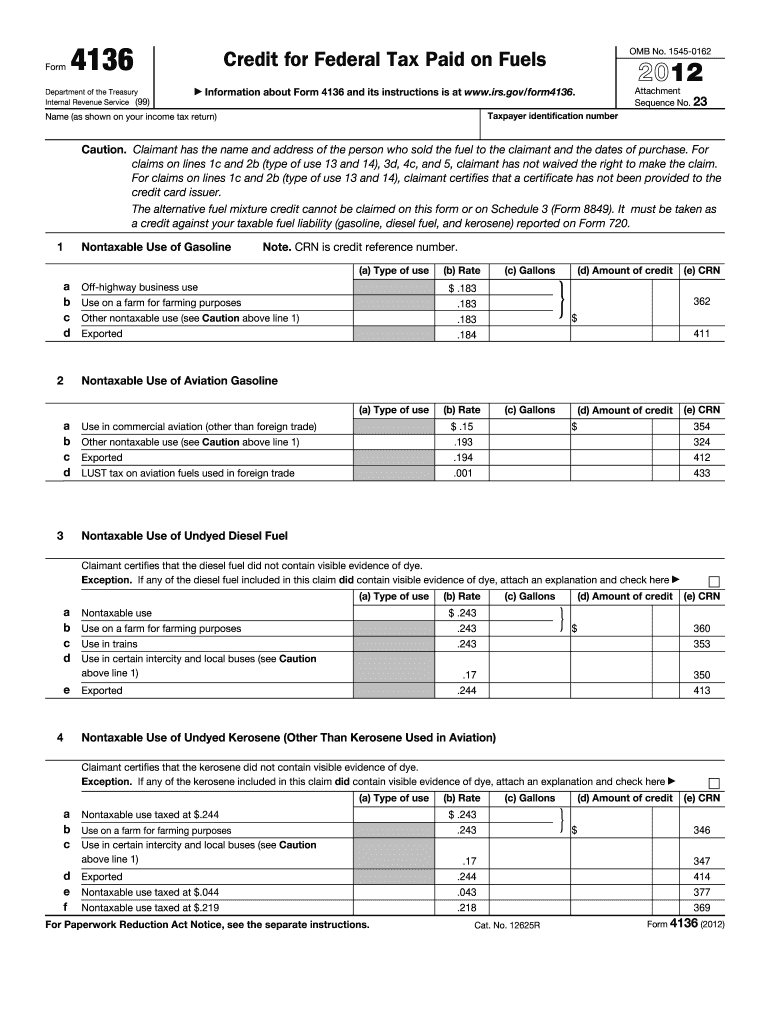

Definition and Purpose of Credit for Federal Tax Paid on Fuels

The "Credit for Federal Tax Paid on Fuels" is a financial mechanism provided by the IRS designed to alleviate the burden of federal excise taxes paid by individuals or businesses on certain fuel types. This credit is claimed through IRS Form 4136, allowing taxpayers to receive a refund or credit for non-taxable uses of fuels such as gasoline, diesel, and kerosene. This includes uses like farming, certain off-highway business purposes, or use in local buses. The aim is to support entities engaging in essential activities by offering a relief form from the fuel taxes that typically apply to these transactions.

Key Elements of the Form

- Nontaxable Uses: Specific guidelines stipulate which uses of fuels qualify as nontaxable, including agricultural use, powering boats, and heating purposes.

- Credit Rates: The form lists precise credit rates for different fuel types and stipulates how these rates apply based on the non-taxable use category.

- Alternative and Biodiesel Fuels: Sections dedicated to alternative fuel credits and biodiesel mixtures outline specific conditions and calculation methods.

How to Obtain the Credit for Federal Tax Paid on Fuels

To claim this credit, taxpayers must complete IRS Form 4136 and submit it with their federal tax return. This process involves:

- Gathering Documentation: Collect records and receipts that detail the total amount of each type of fuel purchased and used.

- Identifying Nontaxable Use: Clearly document how the purchased fuels were used in nontaxable activities.

- Form Completion: Carefully fill out IRS Form 4136, ensuring accurate reporting of usage types and amounts.

- Attachments: Include any required certifications or supplementary documentation that verify nontaxable use claims.

- Submission: File the form alongside the annual tax return to claim the credit.

Required Documents

- Purchase Receipts: Details on quantities and types of fuel purchased.

- Usage Logs: Records of how fuel was used in qualifying activities.

- Certifications: Documentation proving compliance with eligibility and usage guidelines.

Steps to Complete IRS Form 4136

Completing IRS Form 4136 to claim the credit involves several essential steps:

- Download the Form: Access and download the latest version of Form 4136 from the IRS website.

- Section Completion: Fill in sections detailing taxpayer information, fuel types, and usage.

- Calculate Credit: Use the credit rates provided to calculate the total credit for each fuel type based on nontaxable usage.

- Review and Verify: Double-check all entries for accuracy and ensure attached documents support the claims you make.

- Attach and Submit: Include the form with your tax return and submit electronically or by mail as per IRS guidelines.

Form Submission Methods

- Online via IRS e-file: Most recommended for quicker processing.

- Mail: Standard process but involves longer processing times—send it to the correct IRS address noted on the latest instructions.

Eligibility Criteria

Eligibility criteria are stringent and require careful understanding:

- User Types: The credit is open to businesses and individuals using the fuel for specific non-taxable purposes, as outlined by IRS regulations.

- Documentation: Proof of purchase and usage in tax-exempt activities must be substantiated with precise records.

- Adherence to Guidelines: Claimants must comply with detailed IRS guidelines regarding fuel types and applicable non-taxable uses.

Business Types That Benefit Most

- Agricultural Entities: Farms and ranch businesses using fuel for machinery.

- Transportation Companies: Businesses operating local buses and various transport services.

- Construction Firms: Companies that use fuel for machinery in off-highway activities.

IRS Guidelines and Important Terms

Understanding IRS guidelines is crucial to successfully claiming the credit:

- Nontaxable Uses vs. Taxable Sales: Correct differentiation is essential.

- Credit Limits: Restrictions on how much credit can be claimed for certain fuels and allocations.

- Certification Requirements: Necessary steps for acquiring required certifications for nontaxable use claims.

Important Terms

- Alternative Fuels: Specifically defined within the IRS scope—include propane, compressed natural gas, etc.

- Biodiesel Mixtures: Guidelines on acceptable biodiesel blends eligible for credits.

State-Specific Rules and Exceptions

While the credit for federal tax paid on fuels is uniformly designed at the federal level, some nuances may exist at the state level regarding the documentation process and additional state credits:

Examples of State Variations

- State Credits: Certain states offer parallel state-level credits, which can be claimed in addition to federal ones.

- Additional Documentation: Some states might require additional documentation or even pre-approval for specific nontaxable uses.

Penalties for Non-Compliance

Failure to comply with the IRS standards for claiming the credit can lead to potential penalties:

- Misreporting: Inaccurate reporting of fuel use or volume could result in fines.

- Documentation Lapses: Lack of sufficient backup or misplacement of receipts might lead to an audit or denial of credits.

Preventive Steps

- Keep Detailed Logs: Maintain comprehensive and orderly records of all fuel purchases and their applications.

- Regular Audit of Compliance: Periodically review documentation practices and ensure adherence to IRS guidelines.