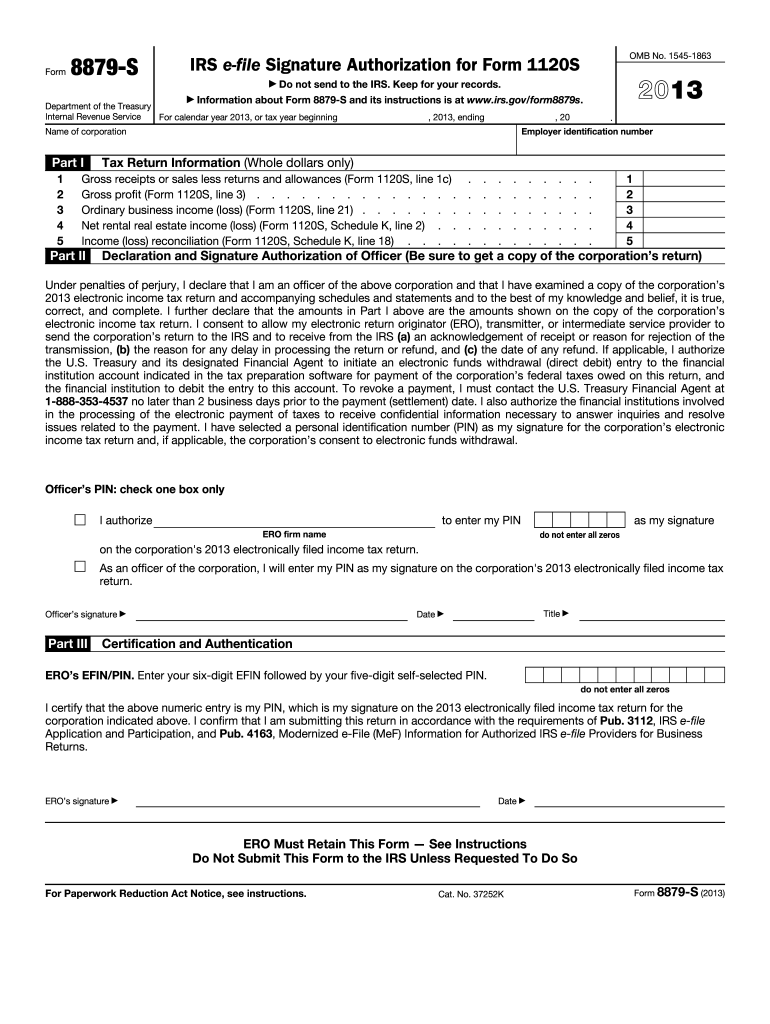

Definition and Purpose of Form 8879-S

Form 8879-S is an IRS document used as an e-file Signature Authorization for Form 1120S, the income tax return filed by S corporations. This form allows a corporate officer to electronically sign the corporation's tax return using a unique personal identification number (PIN). It streamlines the process of filing returns, ensuring both speed and accuracy. The form also clarifies that while it's an official document for signature, it must not be sent to the IRS but should be retained for record-keeping.

Obtaining the 2013 Form 8879-S

To acquire the 2013 Form 8879-S, you can download it directly from the official IRS website. Typically, tax software like TurboTax and QuickBooks also provides access to this form during the return preparation process. Additionally, accounting firms and tax professionals may provide this form if they are managing your tax return.

Completing the 2013 Form 8879-S

- Tax Return Review: Before using Form 8879-S, ensure that the Form 1120S has been reviewed and is accurate.

- Entering Information: Fill out the form with the required tax information, which includes the corporation's identifying details and the total amounts of taxes and payments reported.

- Declaration and Certification: The corporate officer must verify and declare that the information provided is correct. This requires understanding the responsibilities involved in signing off on the form electronically.

- ERO Information: The Electronic Return Originator (ERO) fills in their section, certifying that the officer's PIN has been applied correctly as the signature.

Who Uses Form 8879-S

Form 8879-S is primarily used by S corporations during the e-filing of their income tax returns. The primary users include:

- Corporate officers acting on behalf of the company.

- Electronic Return Originators (EROs) who facilitate electronic filing.

- Tax professionals handling an S corporation's tax matters.

Important Terms Related to Form 8879-S

- Corporate Officer: An authorized executive with signing authority.

- PIN (Personal Identification Number): A unique number used by a corporate officer to sign electronically.

- Electronic Return Originator (ERO): An authorized entity that submits electronic returns to the IRS.

Key Elements of Form 8879-S

- Signature and Authorization: Requires an officer's electronic signature using a PIN, serving as consent to e-filing the tax return.

- Tax Return Data: Essential details like tax liability and total payments should match those reported on Form 1120S.

- ERO Certification: Proves that official protocols for the electronic filing process were followed by the ERO.

IRS Guidelines for 2013 Form 8879-S

The IRS provides explicit instructions regarding the completion and retention of Form 8879-S. Key guidelines include:

- The form should be stored securely as part of the company's records.

- The ERO must ensure the match of the figure entered for the tax return.

- The form should be used only for the designated tax year.

Electronic vs. Paper Version of Form 8879-S

While Form 8879-S supports electronic filing, the data entered must maintain accuracy between digital and paper records. Electronic versions offer the advantage of quicker processing and filing. The retention of digital records is also essential should they be needed for audits or verification by the IRS.

Filing Deadlines and Important Dates

Form 8879-S, like Form 1120S, must be completed and authorized before the IRS filing deadline for S corporations, typically the 15th day of the third month after the end of their tax year. Ensuring timely submission is crucial to avoid penalties and ensure seamless tax return processing.