Definition and Purpose of the 2 Form

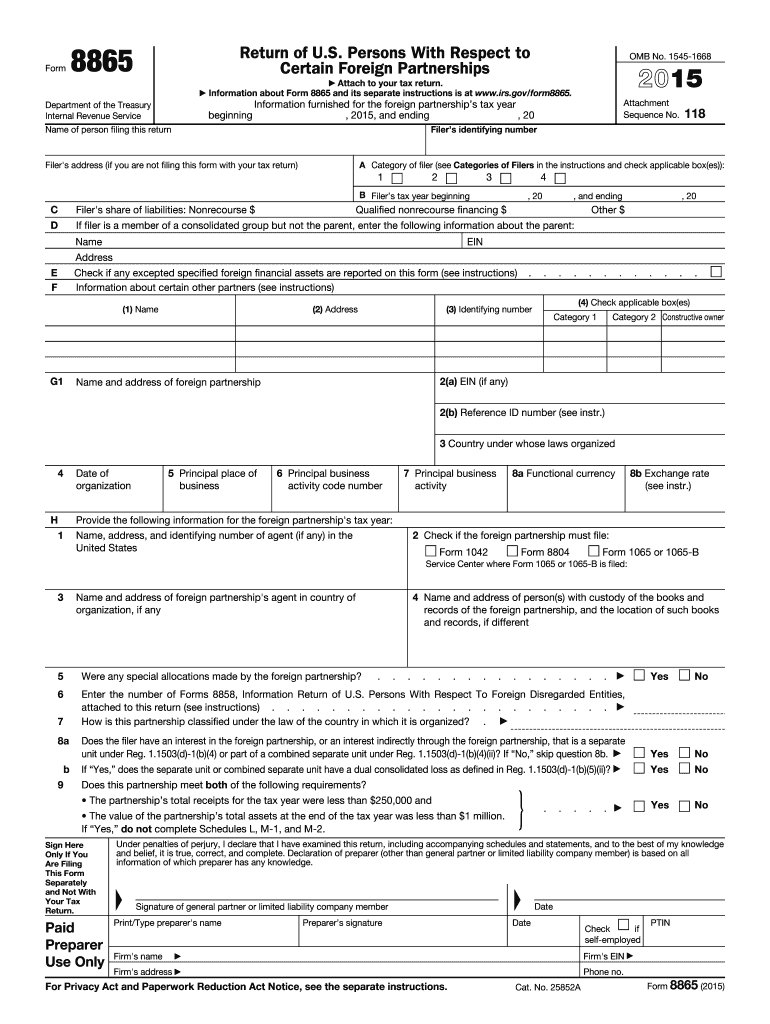

Form 8865, officially titled "Return of U.S. Persons With Respect to Certain Foreign Partnerships," is a tax document required by the Internal Revenue Service (IRS). It collects crucial information on financial activities, ownership structures, and transactions relating to foreign partnerships for U.S. individuals with interests in such entities. This form is essential for ensuring compliance with U.S. tax laws and regulations regarding international financial activities.

U.S. taxpayers use this document to provide details on income, deductions, and other financial aspects of their foreign partnerships. The form helps ensure transparency and accurate reporting of international income, aiding the IRS in monitoring tax obligations of U.S. citizens engaged in global business ventures.

Obtaining the 2 Form

To access the 2 form, you can download it from the IRS website, where it is available in PDF format. Alternatively, you may use tax preparation software that includes IRS forms to fill out the form electronically. Accountants and tax advisors typically have access to the required forms and can guide taxpayers through the process.

If needed, you may also request a physical copy of the form through the IRS by calling their hotline or visiting a local IRS office. Ensure you have the correct version by verifying the year indicated on the form, as tax requirements may vary between years.

Steps to Complete the 2 Form

-

Identify the Applicable Categories: Form 8865 is segmented into four categories based on ownership interest levels and other criteria. Determine the correct category that fits your financial relationship with the foreign partnership.

-

Provide Basic Information: Fill in your name, tax identification number, and the partnership's identification details including the name and address of the foreign partnership.

-

Report Financial Information: Record financial data, such as income, deductions, and balance sheets, related to the partnership. This includes information on the partnership’s trade or business income.

-

Capture Ownership Details: Indicate your ownership percentage and any changes in ownership during the tax year.

-

Attach Additional Schedules: If applicable, include schedules detailing controlled foreign partnerships or separately tracing income attributable to specific partners.

-

Review and Submit: Thoroughly review the completed form for accuracy and completeness before submitting it to the IRS. Forms can be filed electronically or via mail, adhering to IRS submission guidelines.

Key Elements of the 2 Form

- Basic Information Section: Include information on both the taxpayer and the foreign partnership entity.

- Income and Deductions Section: Details on revenue streams, taxable and non-taxable deductions.

- Balance Sheet and Financial Data: Reports on the partnership's assets, liabilities, and equity.

- Ownership Structure: Information on partnership interests and capital accounts.

- Schedule F and M: Information on transactions between controlled foreign partnerships and pertinent trust accounts.

IRS Guidelines for the 2 Form

Following IRS guidelines is crucial for correctly completing the 2 form. These regulations outline reporting requirements, specific form categories, and definitions of key terms like "controlled foreign partnership." IRS guidelines also offer information on reporting regulations for passive foreign investment companies (PFICs) and partnership-related foreign trust activities.

Consult IRS resources or seek professional tax advice for nuanced cases, such as partnerships with complex ownership structures or those operating in multiple jurisdictions.

Filing Deadlines and Important Dates

The regular deadline for submitting Form 8865 is the same as the U.S. federal tax return deadline, typically April 15 of the following year, unless extended. If you file for a tax extension, it applies also to Form 8865. Ensure timely submission, as late filing can result in penalties and additional scrutiny from the IRS.

Electronic filers should verify platform submission cut-off times, while those mailing documents should account for postal delivery times to avoid late submission.

Penalties for Non-Compliance with the 2 Form

Failing to file Form 8865 accurately and on time can result in significant penalties. The IRS may impose a penalty for failure to furnish the required information by the due date. Furthermore, penalties could apply if there is willful or intentional disregard for filing requirements. Correcting errors and prompt communication with the IRS can mitigate consequences, though each case is assessed individually.

Business Entity Types and the 2 Form

Different types of business entities, such as limited liability companies (LLCs), corporations, and limited partnerships, may be required to file Form 8865 if they hold qualifying interests in foreign partnerships. Each entity must evaluate its financial engagements and consult applicable IRS regulations to determine filing obligations under different business structures.

Understanding the form's applicability can aid entity owners in maintaining tax compliance and transparency in their international financial operations.