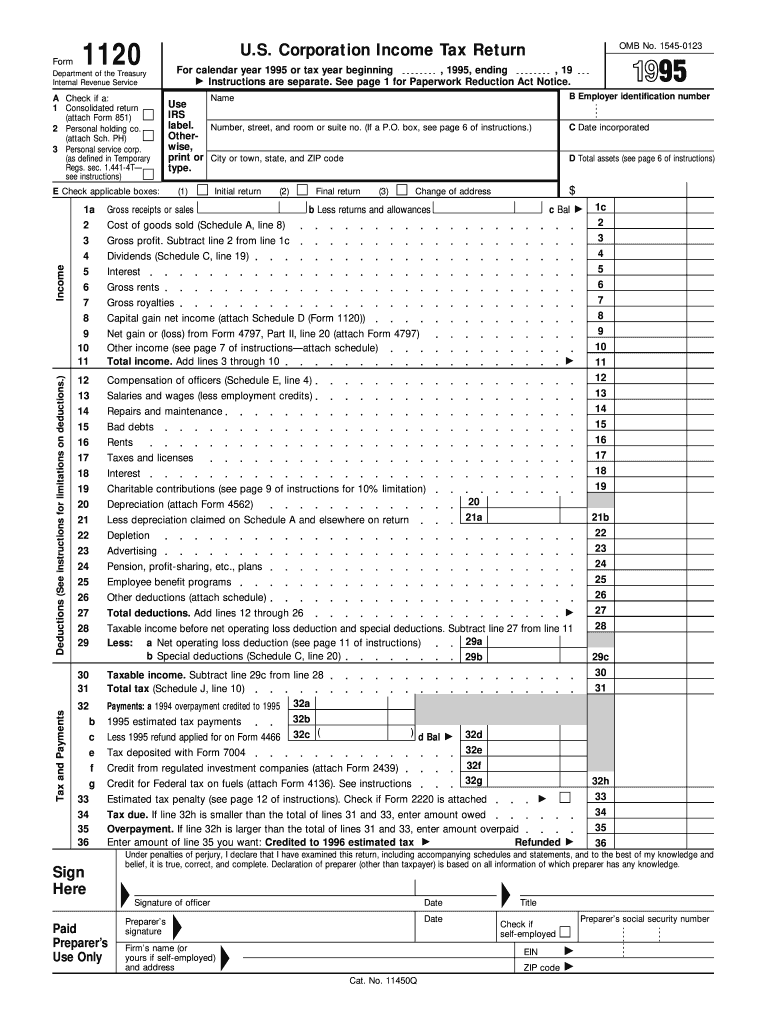

Definition and Purpose of the 1995 Form 1120

The 1995 Form 1120 is officially known as the U.S. Corporation Income Tax Return. It is used by corporations to report their income, deductions, and tax liabilities. This form serves as a comprehensive document that details a corporation's financial activities over the tax year. It is instrumental in calculating the taxes a corporation owes to the Internal Revenue Service (IRS).

Corporations must provide a detailed account of their income, including sales revenue and other types of income, such as dividends and interest. The form also requires corporations to list deductions they are claiming, which can include business expenses, depreciation, and employee compensations. Through careful computations, it aids in determining the taxable income and ultimately the tax that the corporation is liable to pay for that year.

How to Obtain the 1995 Form 1120

Corporations can obtain the 1995 Form 1120 through several basic methods. Although the form is older, it may still be accessible for purposes of amendment or historical accuracy in reporting. The IRS website is a primary source for archived forms. Corporations can download the form directly from the IRS's forms and instructions archive section. Additionally, businesses may contact the IRS directly via their telephone support line to request the form.

Corporations that work with tax professionals or accounting firms may also be able to obtain older forms like the 1995 Form 1120 through these channels. Accountants often maintain extensive archives of tax forms for compliance and advisory purposes.

Steps to Complete the 1995 Form 1120

- Gather Financial Documents: Start by collecting all necessary financial documents, including revenue records, invoices for business expenses, and any previous tax filings that might be relevant.

- Enter Basic Information: Fill in the corporation’s name, address, and employer identification number (EIN).

- Income Section: Document all sources of income, detailing total revenue from business operations and any additional income.

- Deductions and Credits: List eligible deductions such as business-related expenses and relevant tax credits.

- Tax Computation: Calculate the taxable income by subtracting the total deductions from the total income reported.

- Tax Payment: Compute the total tax liability and compare it with any prepayments made during the year to find the balance due or the refund owed.

- Sign and File: Ensure the form is signed by an authorized officer of the corporation and submitted by the filing deadline.

Key Elements of the 1995 Form 1120

- Income Calculations: Sections dedicated to listing all income sources, providing a foundation for tax computation.

- Deductions and Credits: Addresses allowable deductions and tax credits that may reduce overall tax liability.

- Tax Computation: Detailed steps to compute the tax due after accounting for all income and deductions.

- Schedules: Additional schedules like Schedule C for dividends and Schedule J for tax computation and payment to capture detailed information not covered in the main form.

Important Terms Related to the 1995 Form 1120

- Gross Income: The total income before deductions, derived from all business activities of the corporation.

- Deductions: Business expenses permissible by law that lower taxable income, including utility costs, payroll, and rent.

- Taxable Income: The portion of income subject to taxation after all deductions are applied.

Legal Use and Compliance

The 1995 Form 1120 must be completed with accuracy to ensure compliance with IRS regulations. Falsification or misreporting on this form can result in legal penalties. The information provided in the form should reflect truthful financial activity and adhere to IRS instructions.

Corporations are advised to keep detailed and accurate records to support each entry on the form. In case of any discrepancies or audits, having organized records can aid in quickly resolving IRS inquiries.

Who Typically Uses the 1995 Form 1120

The primary users of the 1995 Form 1120 are corporations operating within the United States. This includes C-corporations which are required to file this form annually to report earnings and pay corporate income taxes.

Smaller corporations, such as S-corporations, may not use this particular form as they have different tax reporting requirements, often utilizing Form 1120-S to report income that passes through to shareholders who then report this income on their personal tax returns.

Penalties for Non-Compliance with the 1995 Form 1120

Failing to file the 1995 Form 1120 on time or submitting inaccurate information can attract penalties from the IRS. The basic penalty for failing to file is typically five percent of the unpaid tax for each month the return is late, up to a maximum of 25% of the unpaid tax. Additionally, inaccuracies can lead to further scrutiny or audits, resulting in fines or additional taxes owed.

Corporations are responsible for verifying that their returns are complete and filed promptly to avoid these penalties. It's advisable to consult a tax professional to navigate any complexities associated with the form, especially due to its age and potentially outdated references or rules.