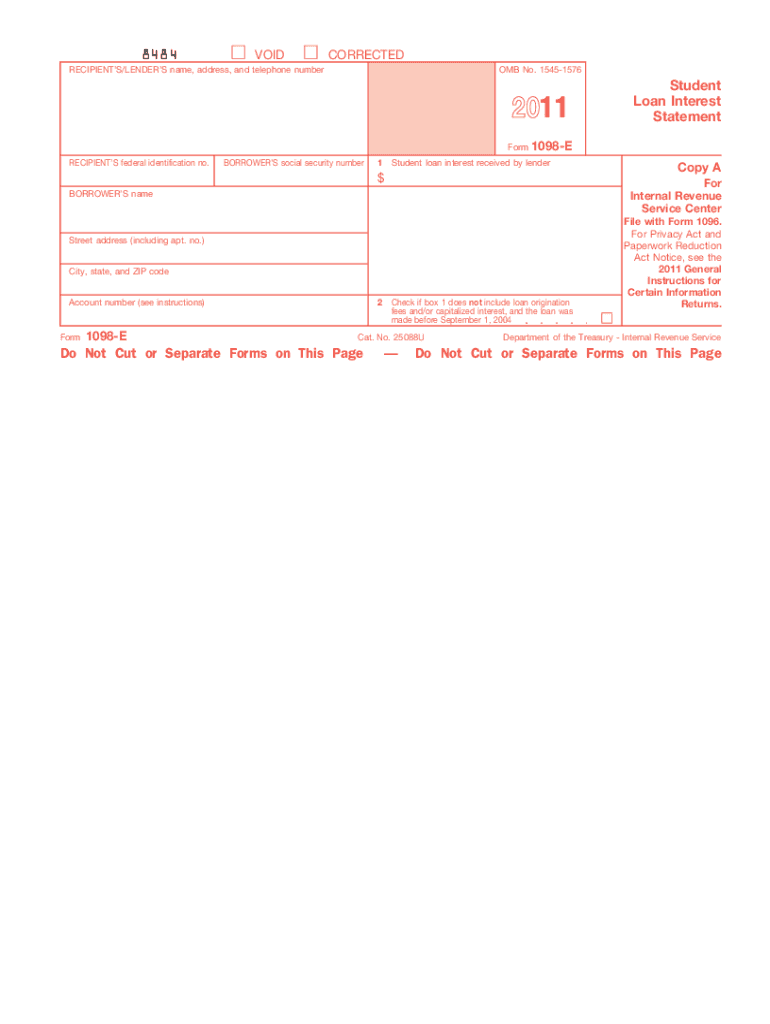

Definition and Purpose of Form 1098-E

Form 1098-E, officially known as the Student Loan Interest Statement, is specifically used by lenders to report the amount of student loan interest a borrower has paid during the tax year. This form is essential for borrowers because it allows them to report and potentially deduct the student loan interest paid, up to the limit allowed by the IRS, from their taxable income. For the 2011 tax year, borrowers and lenders must ensure accurate reporting to avoid any discrepancies when filing taxes.

How to Obtain Form 1098-E for 2011

Form 1098-E for the tax year 2011 can typically be obtained directly from the lender to whom student loan interest payments were made. Most lenders will automatically send this form to borrowers by mail or make it accessible online, often through the lender’s website or borrower portal, usually by the end of January following the tax year. If you did not receive the form, it is advisable to contact the lender or educational institution directly to request a copy and ensure your records are complete.

Steps to Complete Form 1098-E for 2011

-

Verify the Information Provided: Ensure that the lender's information, including their name, address, and tax identification number, is correctly listed on the form. Your name and address should also be verified for accuracy.

-

Check the Interest Amount: Box 1 of the form will contain the total amount of student loan interest paid during 2011. This number is critical as it impacts tax deductions.

-

Include the Form in Your Tax Filing: While the form itself does not need to be filed with your tax return, the information from Box 1 should be used on IRS Form 1040, Schedule 1, for claiming the interest deduction.

-

Store the Form for Your Records: Keep the form in your tax records for at least seven years as it serves as proof of interest paid if the IRS requests verification.

Importance of Form 1098-E

The primary purpose of Form 1098-E is to allow borrowers to potentially receive a tax deduction for the student loan interest paid, which can lower taxable income and, consequently, the overall tax burden. For 2011, the maximum interest deduction allowed was $2,500, and eligibility was dependent on the borrower's adjusted gross income being within specific limits set by the IRS.

Key Terms and Conditions Related to Form 1098-E

-

Student Loan Interest: Interest paid on a qualifying student loan used solely for qualified educational expenses.

-

Adjusted Gross Income (AGI): Your taxable income from all sources, adjusted for specific deductions, which must be below a threshold to qualify for the deduction associated with the form.

-

Qualified Education Expenses: Costs required for enrollment or attendance at an eligible educational institution, including tuition, fees, books, supplies, and equipment.

IRS Guidelines for Form 1098-E

The IRS provides specific guidelines regarding the use of Form 1098-E:

- Borrowers can deduct student loan interest if they are legally obligated to pay the loan.

- You cannot be claimed as a dependent by another taxpayer.

- Married couples should file jointly to qualify for the deduction.

- For 2011, the full deduction was available for those with a modified AGI below $60,000 for single filers and $120,000 for joint filers.

Penalties for Non-Compliance

Filing Form 1098-E is essential for tax compliance. Failure to report the correct amount of student loan interest or including incorrect information on a tax return may lead to penalties imposed by the IRS. Borrowers could lose eligibility for the deduction or face additional tax liabilities if discrepancies aren't rectified.

Filing Deadlines and Important Dates for 2011

- By January 31, 2012: Lenders must have sent Form 1098-E to borrowers.

- By February 28, 2012: Paper submissions of the form to the IRS are due.

- By April 17, 2012: The deadline for filing individual tax returns and using information from Form 1098-E for deductions.

Submission Methods of the Form

Although the borrower uses the form's information for their tax return rather than submitting it, lenders have specific submission requirements. They may file electronically through the IRS’s FIRE system, or by paper mail, though electronic filing is becoming the predominant method due to its efficiency and reduced likelihood of errors.

Digital vs. Paper Version of Form 1098-E

Traditionally, Form 1098-E was mailed to borrowers, but digital versions are increasingly offered. Accessing the digital format via lender websites often ensures quicker receipt and easy record-keeping, although borrowers should confirm the unique IRS identification and ensure it matches their fiscal records. This transition is also environmentally friendly and aligns with the digital-first strategy of modern financial documentation.