Definition and Purpose of the 8889 Form 2010

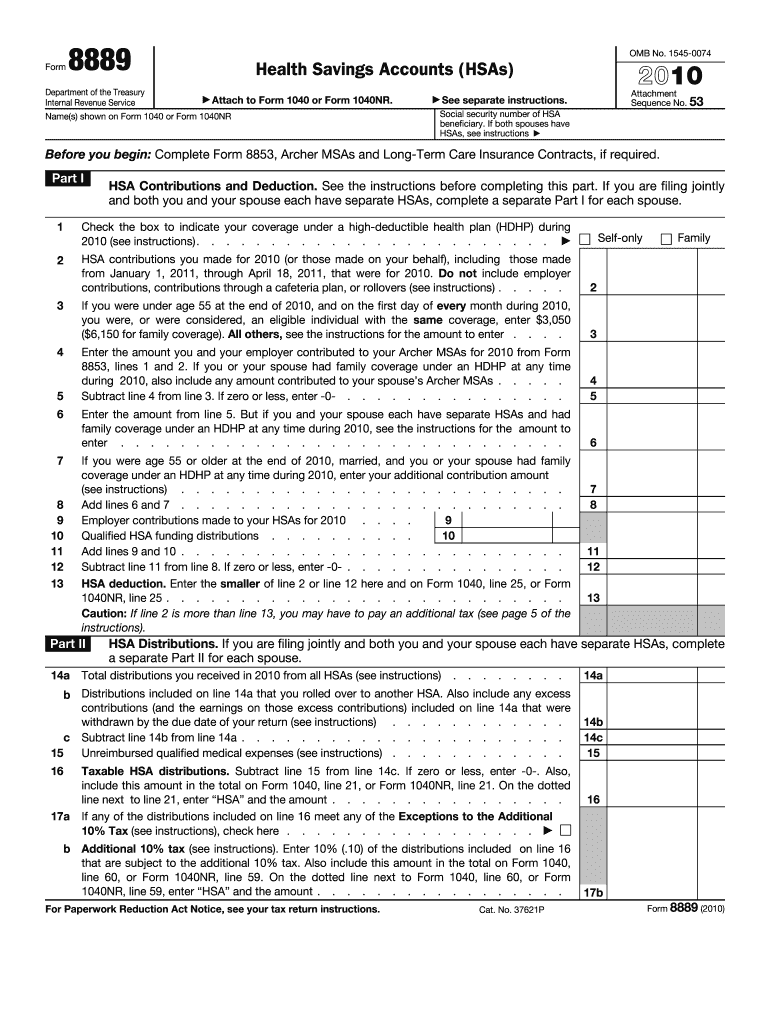

Form 8889, used for the 2010 tax year, is a critical document for taxpayers with Health Savings Accounts (HSAs). This form is necessary for reporting contributions, deductions, and distributions related to HSAs, ensuring that all financial activity is accurately reflected for tax purposes. It plays an essential role in calculating any additional taxes pertaining to maintaining a high-deductible health plan (HDHP).

Role in Tax Filing

The form is primarily used alongside Form 1040 or 1040NR. Taxpayers must detail all HSA-related activities within the year, providing a clear picture of their financial interactions with the account. This form is indispensable for anyone aiming to maximize their HSA benefits while staying compliant with IRS regulations.

How to Use the 8889 Form 2010

When filling out Form 8889, attention to detail is paramount. It involves several sections that require accurate data entry. These sections include those for declaring contributions, calculating deductions available from HSA contributions, and detailing any distributions received.

Completing the Form

- Section One: Document the total contributions made to your HSA. This includes contributions made directly by the taxpayer as well as those by their employer.

- Section Two: Calculate the eligible deduction. The IRS allows deductions based on your contributions adjusted by any employer contributions.

- Section Three: Record any HSA distributions. This is essential for ensuring you are not subject to unnecessary taxation.

How to Obtain the 8889 Form 2010

Acquiring the Form 8889 for tax year 2010 is a straightforward process. It can be downloaded directly from the IRS website. Alternatively, those using tax preparation software can often find the form integrated within the application’s library of documents.

Other Methods

Accessing the form through professional tax preparers or directly from financial institutions holding an HSA can also be an option. Some banks offer these forms for convenience, aligning with their clients' tax preparation needs.

Steps to Complete the 8889 Form 2010

Completing Form 8889 with precision is crucial for correct tax reporting. Here’s a breakdown of the task:

- Gather Information: Assemble all materials related to HSA contributions and distributions for the tax year.

- Fill Out Contribution Details: Enter contribution data in Part I of the form.

- Calculate Deductible Amounts: Part II focuses on deductions allowable against your HSA contributions.

- Distributions and Taxes: Part III captures information on distributions and calculates potential taxes on non-qualified medical expenses.

These steps ensure a comprehensive approach to managing the intricate details of HSAs within your tax return.

Legal Use and Eligibility Criteria for the 8889 Form 2010

Under U.S. tax law, Form 8889 must be filed by any taxpayer who owns an HSA. The form supports the lawful reporting and tax treatment of contributions and distributions.

Eligibility Criteria

- Must have a qualifying HSA linked to a high-deductible health plan.

- Should have had contributions or distributions within the year.

- Eligibility aligns with the broader IRS guidelines surrounding HSAs and HDHPs.

Comprehending these criteria is fundamental for taxpayers to maintain compliance and optimize their tax positions.

IRS Guidelines and Important Dates

Understanding IRS guidelines for Form 8889 is essential. These rules dictate how taxpayers should report, calculate, and claim deductions related to their HSAs.

Filing Deadlines

The form must be completed and submitted by the typical tax return filing deadline, which is April 15 of the year following the tax year being reported. Any extensions mirror those granted for filing Form 1040 or 1040NR, offering taxpayers flexibility in complicated or time-consuming situations.

Penalties for Non-Compliance with the 8889 Form 2010

Failing to accurately complete or timely file Form 8889 can lead to penalties and interest charges. The IRS staff has a spectrum of consequences tailored to varying degrees of oversight or neglect.

Specific Penalties

- Failure to File: Penalties can accrue based on the overall amount of unpaid taxes due.

- Underreporting: If contributions or deductions are inaccurately reported, subjecting the taxpayer to underpayment, additional fines may apply.

Taxpayers should seek to mitigate these risks by ensuring all relevant information is accurately and timely presented.

Taxpayer Scenarios Involving the 8889 Form 2010

Various taxpayers may find themselves needing to complete Form 8889. This includes self-employed individuals, corporate employees with HSA plans, retirees, and students working under particular earning thresholds.

Common Scenarios

- Self-Employed Individuals: Often establish HSAs to reduce tax liabilities.

- Corporate Employees: Utilize employer contributions for tax efficiency.

- Retirees: Occasionally use HSAs for healthcare expenditures, potentially stretching retirement funds further.

These scenarios reflect the form's adaptability and relevance across diverse taxpayer profiles.