Definition & Purpose of the 2015 Form Injured Spouse

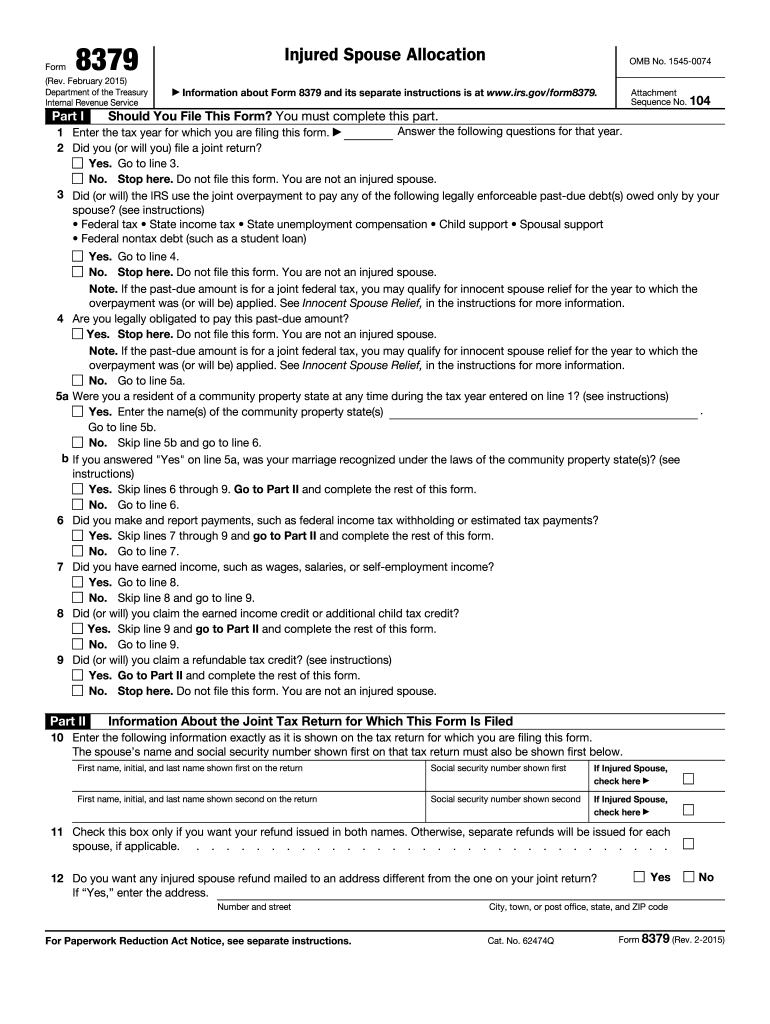

The 2015 form injured spouse, also known as Form 8379, is utilized by individuals seeking to reclaim their portion of a tax refund when a joint tax return was filed, and a part of the refund is used to offset a spouse’s past-due debts. These debts might include child support, student loans, or federal taxes. Its primary function is to allow the injured spouse, who is not responsible for these debts, to claim their share of the tax refund without it being unfairly allocated towards their spouse’s obligations.

How to Obtain the 2015 Form Injured Spouse

Acquiring the 2015 form injured spouse involves several straightforward methods. Taxpayers can download it directly from the official IRS website, ensuring they receive the most recent and correct version. Additionally, tax preparation software such as TurboTax often includes this form in their databases, allowing individuals to access it easily during the electronic filing process. For those who prefer a paper copy, one might request it by calling the IRS and having a form mailed to their address.

Steps to Complete the 2015 Form Injured Spouse

-

Identify Personal Information: Start by entering basic details, including the taxpayer’s and spouse’s names, Social Security numbers, and contact information.

-

Determine Refund Allocation: Specify how the refund should be split by listing income, tax withheld, and credits claimed individually or jointly.

-

Analyze Debt Responsibility: Clearly indicate which debts belong to the liable spouse and confirm that the taxpayer is not legally responsible.

-

Sign and Date the Form: Both spouses may be required to sign, affirming the accuracy of the information provided.

-

Attach to Joint Tax Return: If the form is completed during tax season, attach it with the joint tax return for concurrent submission.

Eligibility Criteria for the 2015 Form Injured Spouse

Not everyone qualifies to use the 2015 form injured spouse. Eligibility requires that the couple has filed a joint tax return, and the injured spouse is not liable for the debts causing the refund offset. The liabilities must solely belong to the other spouse. Furthermore, any refund claimed by the injured spouse should originate from tax payments or credits generated by the injured spouse alone.

Key Elements of the 2015 Form Injured Spouse

- Income Declaration: Each spouse must disclose their individual earnings to determine the proper allocation of the refund.

- Tax Liabilities: A detailed account of liabilities ensures accurate formulation and refund distribution.

- Deductions and Credits: Distributing deductions and credits helps ascertain each spouse's rightful share of the refund.

- Notification: The IRS sends a notice outlining how the debt will affect any refund and whether an injured spouse claim is necessary.

State-Specific Rules for the 2015 Form Injured Spouse

While the 2015 form injured spouse is a federal tax form, community property states such as California, Arizona, or Nevada may have additional considerations. Here, income and property acquired during the marriage are typically shared equally, impacting how the addressed debts and refunds are treated. It is advisable for spouses living in these states to consult state tax laws and potentially seek legal advice to ensure compliance.

IRS Guidelines and Penalties

The IRS provides frameworks outlining proper completion and submission of the injured spouse form. Non-compliance, such as failing to report necessary information or inaccurately representing debts, can have significant penalties, including audits or rejection of the claim. It is vital to follow these guidelines strictly to avoid legal repercussions and ensure timely resolution.

Form Submission Methods

Submitting the 2015 form injured spouse can be done both electronically and via traditional mailing. Electronic submission is generally faster and offers enhanced tracking capabilities. Alternatively, one can mail the form separately to the IRS if filing after the primary tax return has already been submitted. Including all relevant documents and retaining copies for record-keeping is recommended regardless of the submission method chosen.