Definition & Meaning

Form 990-PF is a detailed financial report used primarily by private foundations in the United States. It serves as a comprehensive return to report their annual operations, including various financial activities such as revenue generation, expense tracking, and charity distributions. This form is essential for transparency and accountability, providing insight into a foundation's fiscal health and compliance with federal regulations. Private foundations use this document to detail their financial status, ensuring that they adhere to tax-exemption requirements and justify their nonprofit status.

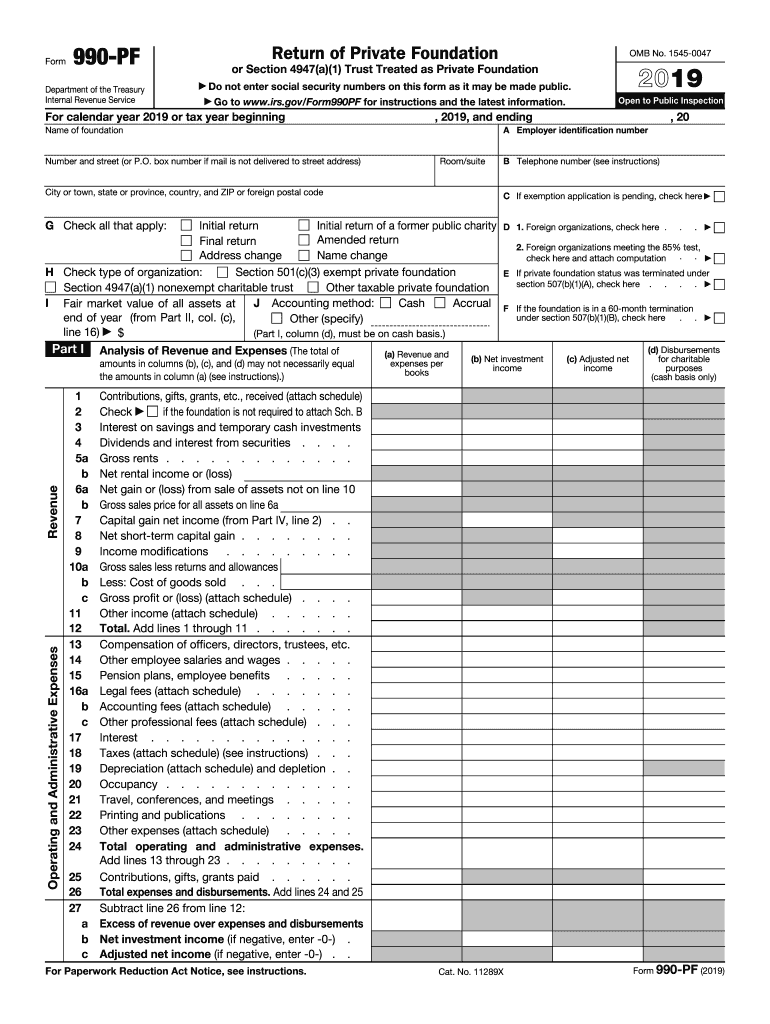

Key Elements of the 990-PF

Form 990-PF consists of several critical sections, each providing specific financial information about the foundation's activities. These sections include:

- Operating Expenses: This section captures all expenses associated with running the foundation, from administrative costs to program-specific expenses.

- Revenue and Financial Summary: A detailed account of all generated revenue sources, including contributions, investments, and other income streams.

- Grants and Contributions: Documents the foundation's charitable activities, detailing how funds are distributed to various organizations or causes.

- Balance Sheets: An overview of the foundation's assets and liabilities, providing a snapshot of financial stability.

These elements allow stakeholders to assess the foundation's financial practices and adherence to its mission.

How to Use the 990-PF

Using the 990-PF involves a methodical approach to ensure all required information is accurate and complete. The process generally includes:

- Assemble Financial Records: Gather all relevant financial documents, including income statements, balance sheets, and records of charitable contributions.

- Populate Financial Data: Enter detailed financial information into the relevant sections of the 990-PF, ensuring alignment with documented activities.

- Review Compliance Requirements: Verify that all entries meet IRS requirements and adhere to tax-exemption rules.

- Prepare for Submission: Ensure the form is thoroughly reviewed for accuracy before filing.

This structured process ensures compliance with IRS expectations and legal stipulations for nonprofit organizations.

Steps to Complete the 990-PF

Completing the 990-PF can be broken down into several clear steps:

- Gather Required Documents: Compile all necessary documentation, including financial statements and records of grants awarded throughout the year.

- Accurate Data Entry: Enter financial information in each section with attention to detail, using spreadsheets or accounting software to minimize errors.

- Seek Professional Assistance: Consider consulting with an accountant or a tax advisor specializing in nonprofit compliance to review the form.

- Final Review: Double-check all entries for accuracy and completeness, ensuring all IRS deadlines and requirements are met.

- Filing: Submit the form electronically using IRS-approved platforms or via mail if preferred. Track the filing status to confirm successful submission.

Following these steps helps maintain compliance and avoids costly penalties.

Important Terms Related to 990-PF

Understanding key terminology within the 990-PF is crucial to correctly interpreting and completing the form. Important terms include:

- Net Investment Income: Income from interest, dividends, rents, royalties, and gains from property sales.

- Distributable Amount: The minimum amount a foundation must allocate each year to maintain tax-exempt status.

- Foundation Manager: An officer, director, or trustee responsible for managing the foundation's assets.

Grasping these terms is essential for accurately completing the form and ensuring correct reporting.

IRS Guidelines for 990-PF

The IRS stipulates specific guidelines for the 990-PF to guarantee compliance with federal tax laws. Notable guidelines include:

- Filing Deadline: Typically the 15th day of the 5th month after the end of the fiscal year.

- Electronic Filing: Mandatory for organizations with assets of $10 million or more or who file 250 or more returns annually.

- Accuracy and Completeness: Insist on full disclosure of financial activities to avoid penalties or revocation of tax-exempt status.

Understanding these guidelines is fundamental to avoiding issues with the IRS.

Filing Deadlines / Important Dates

Foundations are subject to stringent filing deadlines for the 990-PF:

- Standard Deadline: The form is due on the 15th day of the 5th month following the end of the fiscal year. For a December 31 fiscal year-end, the deadline is May 15.

- Extensions: A six-month extension can be requested using Form 8868, which must be submitted before the original deadline.

Meeting these deadlines is crucial to maintaining good standing with the IRS.

Penalties for Non-Compliance

Failure to comply with the 990-PF filing requirements can result in significant penalties:

- Late Filing Penalties: Charges accrue up to $100 per day, capped at $51,000 or 5% of the organization's gross receipts, whichever is less.

- Failure to Provide All Information: Incomplete or inaccurate filings can lead to additional penalties or auditing.

Staying informed of these penalties underscores the importance of meticulous documentation and filing practices.