Definition and Purpose of Form 433-A (OIC)

Form 433-A (OIC), officially known as the Collection Information Statement for Wage Earners and Self-Employed Individuals, is a crucial document used by the Internal Revenue Service (IRS) in the United States. This form collects comprehensive financial information from individuals who owe income tax, excise tax, or certain penalties. The main goal is to assess the financial condition of the taxpayer and determine their eligibility for an Offer in Compromise (OIC), which is an agreement that allows for settling tax debt for less than the full amount owed.

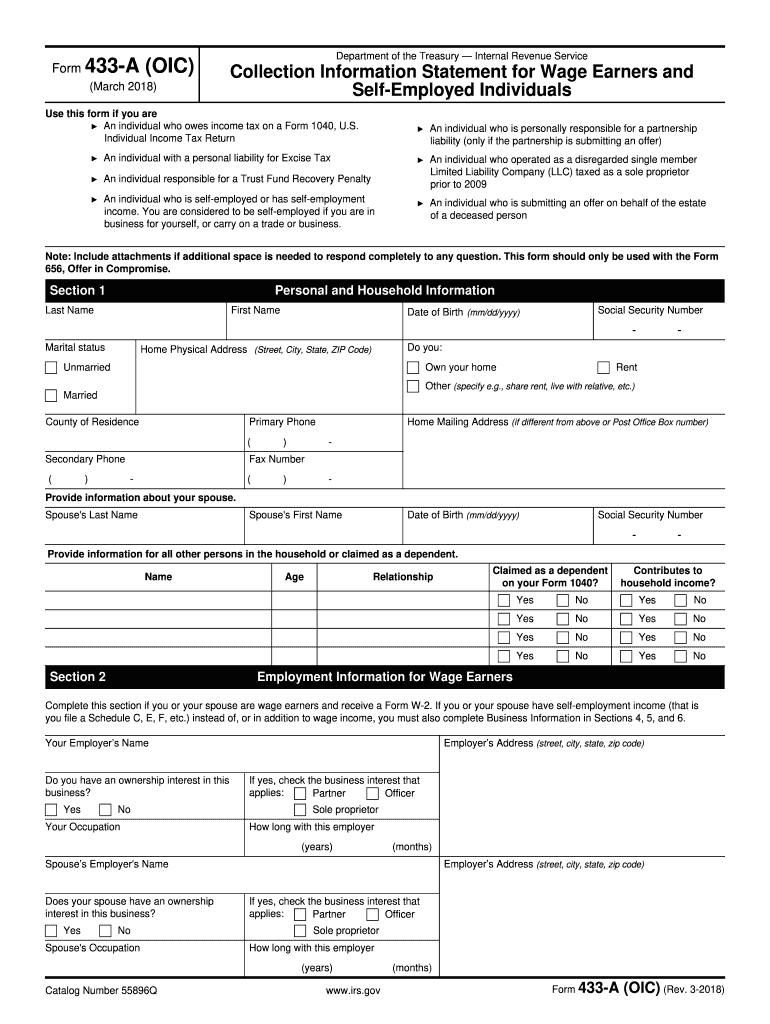

Key Components of Form 433-A (OIC)

Form 433-A (OIC) includes several sections designed to capture in-depth financial details. The completed form provides a snapshot of the taxpayer's financial situation, allowing the IRS to evaluate the legitimacy of the OIC request.

- Personal and Household Information: This section gathers identifying details and household size, which is vital for understanding the living situation and dependents.

- Assets and Liabilities: Information about assets, including real estate, vehicles, bank accounts, and investments, is required to assess net worth.

- Employment and Self-Employment Data: Employment status and income sources are listed, providing insights into the taxpayer's earning capacity.

- Monthly Income and Expenses: This part details all income received and bills paid, helping to portray the taxpayer's financial stability.

- Additional Information for Self-Employed: Specialized data for those who run their own business, including income and expenses related to business operations.

Steps to Complete Form 433-A (OIC)

Completing Form 433-A (OIC) requires careful attention to detail, as it involves supplying exhaustive financial information. Here’s a structured approach to filling out the form:

- Gather Required Information: Collect personal information, financial records, asset documentation, and employment details before starting the form.

- Complete Personal Details Section: Begin with basic personal and household information, ensuring accuracy and completeness.

- List Assets and Debts: Provide detailed information on all assets and liabilities, including account numbers and asset values.

- Document Income Sources: Include all sources of income, distinguishing between wages, business income, pensions, and other revenues.

- Record Monthly Expenses: Accurately report monthly living expenses, ensuring to include categories such as housing, food, and transportation.

- Review and Double-Check: Carefully review the completed form for any errors or omissions before submission.

Eligibility Criteria for Filing Form 433-A (OIC)

Assessing eligibility for submitting Form 433-A (OIC) is necessary to avoid rejection. The IRS establishes specific conditions that must be met before considering an Offer in Compromise:

- Financial Hardship: Applicants must demonstrate their inability to pay the full tax liability without significant financial hardship.

- Income vs. Expenses: The applicant's monthly income compared to allowable living expenses is a critical factor in determining eligibility.

- Asset Value: The value of assets and availability of liquid funds impact the likelihood of acceptance.

- Compliance with Other Obligations: Taxpayers must be current with all filings and payments for the IRS to entertain the offer.

How to Obtain Form 433-A (OIC)

Acquiring Form 433-A (OIC) can be done through several methods, ensuring accessibility regardless of preference for digital or paper formats:

- IRS Website: Download a digital copy directly from the IRS website, where the form and its instructions are available in a PDF format.

- IRS Office: Visit a local IRS office to obtain a physical copy if a printed version is preferred.

- By Mail: Request that a copy be mailed to you by contacting the IRS customer service line.

IRS Guidelines for Form 433-A (OIC)

The IRS provides specific guidelines which must be adhered to when completing and submitting Form 433-A (OIC). Ensuring compliance helps mitigate the risk of processing delays or rejection:

- Submission with Offer in Compromise Application: Accompany the form with the complete Offer in Compromise application to facilitate evaluation.

- Documentation Requirements: Attach all necessary supporting documentation, such as pay stubs, bank statements, and asset verification.

- Accurate Representation: Ensure that all reported information is accurate and truthful to prevent further scrutiny or penalty.

Important Terms Related to Form 433-A (OIC)

Navigating Form 433-A (OIC) is made easier by understanding key terms and definitions associated with the process:

- Offer in Compromise (OIC): A program that allows taxpayers to settle debts for less than the full amount owed.

- Allowance Standards: IRS established limits for common living expenses, used to determine reasonable expense deductions.

- Doubt as to Collectibility: A criterion where the taxpayer's debt exceeds their income and asset value.

- Financial Statement: An overview of an individual's financial status, including assets, liabilities, income, and expenses.

Legal Use of Form 433-A (OIC)

Understanding the legal implications of Form 433-A (OIC) is crucial for applicants:

- Settlement Agreement: Acceptance of an OIC results in a legally binding agreement between the taxpayer and the IRS.

- Compliance Requirements: The taxpayer agrees to comply with future tax obligations as part of the offer terms.

- Revocation of Offer: The IRS reserves the right to revoke the acceptance of an OIC if false information is discovered post-agreement.

Penalties for Non-Compliance

Failing to accurately complete or comply with requirements associated with Form 433-A (OIC) can lead to penalties:

- Rejection of OIC: Incomplete or inaccurate responses may result in the rejection of the offer, necessitating full payment of the debt.

- Imposed Fines: Intentional misinformation can lead to fines or additional penalties.

- Future Non-acceptance: Historical non-compliance may impact future IRS proposals and negotiations.

State-Specific Rules for Form 433-A (OIC)

Though Form 433-A (OIC) is a federal document, state-specific regulations might have implications on the processing:

- State Tax Obligations: States with their own tax settlement programs may have additional requirements.

- Impact on State Benefits: Acceptance of a federal OIC might affect state benefits or obligations.

Real-World Examples of Using Form 433-A (OIC)

Practical applications of Form 433-A (OIC) highlight its utility and potential benefits for different taxpayer scenarios:

- Self-Employed Professionals: Individuals with fluctuating income streams use the form to advocate for reduced settlement based on uncertain future earnings.

- Retirees with Fixed Income: Retired taxpayers leverage limited income details to justify the acceptance of a lower settlement.

By following these comprehensive insights regarding Form 433-A (OIC), taxpayers can effectively navigate the complexities of negotiating tax obligations with the IRS.