Definition and Purpose of an Asset Verification Letter

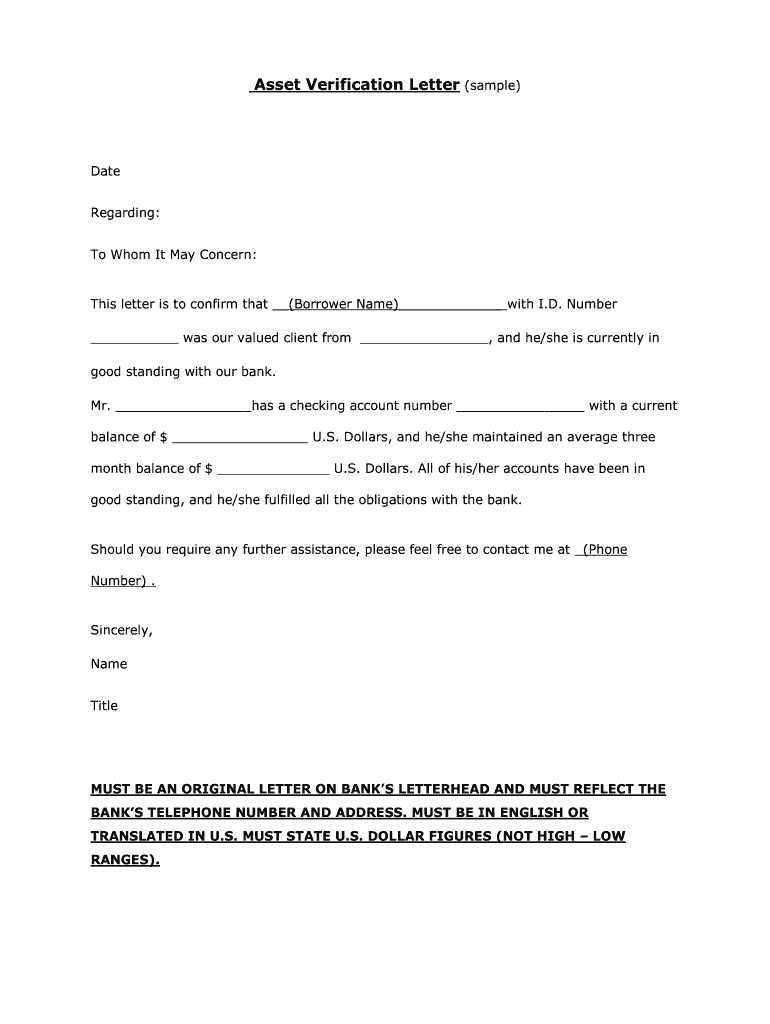

An asset verification letter, often referred to as an asset confirmation letter, is a formal document used to confirm an individual's or entity's financial standing, particularly regarding their available assets. This letter is typically issued by financial institutions, such as banks or credit unions, and it serves as verification of the account holder’s assets, including cash balances, savings accounts, investments, and other financial holdings. The primary purpose of this letter is to provide essential proof of assets for various financial transactions, such as loan applications, mortgage approvals, or other credit decisions.

The asset verification letter typically includes:

- The name and address of the financial institution.

- The account holder’s name and relevant account details.

- A statement confirming the balances or holdings in the account.

- The date the information is accurate as of, ensuring it is current for the requesting party.

- An official signature or stamp from an authorized bank representative, signifying authenticity.

This letter is essential for individuals seeking to prove their financial stability and is commonly required by lenders, landlords, and other entities that need to assess someone's financial situation.

Key Elements of an Asset Verification Letter

To ensure that an asset verification letter serves its intended purpose effectively, it must include several critical components:

-

Institutional Header: The letter should be printed on the official letterhead of the issuing bank or financial institution. This includes the logo, contact information, and other identifying details.

-

Account Holder Information: It should clearly state the name and address of the individual or entity whose assets are being verified.

-

Asset Details: The letter must enumerate specific details regarding the assets, such as:

- Account types (e.g., checking, savings, investment)

- Account numbers (may be partially redacted for security)

- Current balances and their statuses (e.g., good standing)

-

Issuing Date: The document should specify the date on which the verification is valid, as it affirms that the information is current.

-

Authorized Signature: A representative from the financial institution must sign the letter, either in wet ink or digitally, to validate the document's authenticity.

Ensuring that all these elements are included will strengthen the letter's effectiveness when presented to third parties for verification purposes.

How to Obtain an Asset Verification Letter

Requesting an asset verification letter typically involves several straightforward steps, ensuring that the process is hassle-free for account holders:

-

Choose the Right Institution: Identify the bank or financial institution where your assets are held, as this is the entity that will issue the verification letter.

-

Contact the Institution: Reach out to the bank's customer service or your personal banking representative. This can be done via phone, email, or through online banking portals.

-

Provide Necessary Information: Be prepared to offer essential details, including your full name, account numbers, and any specific information the institution requires for identity verification.

-

Specify the Purpose: When making your request, clarify the intended use of the asset verification letter. This might include applying for a mortgage, securing a loan, or validating your financial status for contractual obligations.

-

Review and Confirm: Once the letter is prepared, review it for accuracy. Ensure all asset details are correct and that the letter contains the appropriate signatures before using it for its intended purpose.

Institutions may have varying processing times, so it’s advisable to request this documentation well in advance of any deadlines related to transactions or applications.

Common Use Cases for Asset Verification Letters

Asset verification letters are crucial in various financial scenarios and industries. Here are some common use cases:

-

Mortgage Applications: Lenders typically require an asset verification letter to assess a borrower's financial stability and ability to repay the mortgage loan.

-

Renting or Leasing: Landlords may request asset verification to determine a potential tenant's financial capability to meet rent obligations.

-

Loan Applications: Financial institutions often seek proof of assets when assessing applicants for personal or business loans to mitigate risks.

-

Investment Transactions: Investors may need to present asset verification letters when dealing with large transactions or trading accounts to confirm they have the necessary funds.

-

Divorce Proceedings: In legal disputes, particularly during divorce settlements, asset verification can be utilized to establish the financial standing of both parties.

In all these instances, having a reliable and accurate asset verification letter can facilitate financial trust and provide necessary reassurances to all parties involved in a transaction.

Important Considerations for Asset Verification Letters

When preparing or requesting an asset verification letter, several factors should be taken into account to ensure the effectiveness and compliance of the document:

-

Confidentiality: Asset verification letters contain sensitive information, so it’s vital to safeguard this data during transmission to third parties.

-

Expiration: Asset verification letters typically have a validity period. Always check if the document is still relevant for the specific transaction at hand.

-

State-Specific Regulations: Familiarity with any state-specific legal requirements for asset verification letters can help in ensuring compliance and acceptance across different jurisdictions.

-

Documentation Standards: Different institutions might have their specific formats or requirements for an asset verification letter, so understanding these can expedite the process.

-

Follow-Up: After submitting the asset verification letter, it may be prudent to follow up with the requesting party to confirm receipt and ensure there are no additional questions or requirements.

By considering these factors, individuals can make informed decisions and uphold their financial reputations while managing their assets.