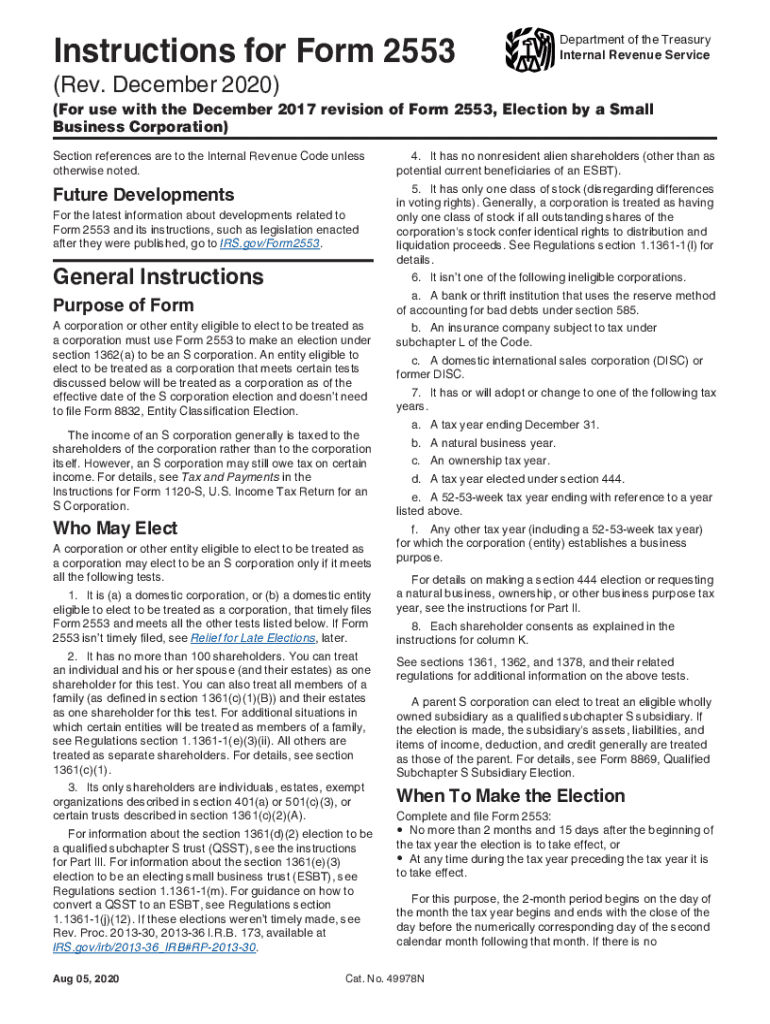

Definition and Purpose of Form 2553

Form 2553 is a crucial document used by eligible small business corporations in the United States to elect S corporation status under the Internal Revenue Code. This election allows corporations to pass income, losses, deductions, and credits directly to their shareholders for federal tax purposes, avoiding the double taxation that typically affects C corporations. The S corporation designation primarily benefits qualifying small businesses by allowing them to pay taxes at the individual shareholder level rather than the corporate level.

Key Objectives of Form 2553

- Facilitate S corporation election to avoid dual taxation.

- Provide a legal mechanism for eligible businesses to enhance tax efficiency.

- Enable shareholders to report income and losses on personal tax returns, potentially leading to favorable tax outcomes.

Overview of Eligibility

- Corporations must meet specific criteria, such as being domestic and having no more than 100 shareholders.

- Shareholders must be individuals, certain trusts, or estates.

- The corporation must have only one class of stock.

Steps to Complete Form 2553

Completing Form 2553 requires careful attention to ensure accuracy and compliance with IRS guidelines. Here is a step-by-step process to guide you:

-

Identify Corporate Information:

- Include the corporation’s name, address, and employer identification number (EIN).

- Specify the state of incorporation.

-

Election Information:

- Indicate the tax year for which the S corporation status is being elected.

- Enter the desired effective date of the S corporation election.

-

Shareholder Consent:

- Obtain consent from all shareholders to make the S election.

- List all shareholders’ names, addresses, and taxpayer identification numbers.

-

Signature and Submission:

- Ensure that an authorized corporate officer signs and dates the form.

- Submit the completed form to the appropriate IRS office.

Practical Considerations

- Early submission is advisable due to the IRS processing time.

- Keep copies of the signed form and any additional documentation for corporate records.

Filing Deadlines and Important Dates

Timeliness is essential when filing Form 2553 to ensure that the S corporation election is recognized for the desired tax year.

Standard Filing Deadline

- The form must be filed no later than two months and 15 days after the beginning of the tax year when the election is intended to take effect.

Late Election Relief

- If the form is filed after the deadline, corporations may qualify for late election relief with appropriate justification under IRS Revenue Procedure guidelines.

Eligibility Criteria for S Corporation Election

Specific criteria determine whether a corporation can apply for S corporation status:

- U.S. Incorporeality: Must be a domestic corporation.

- Shareholder Limit: Must have 100 or fewer eligible shareholders.

- Stock Specifications: Can only have one class of stock.

- Eligible Shareholders: Shareholders must be individuals, qualifying trusts, or estates.

Considerations for Eligibility

- Non-resident aliens or partnerships cannot be shareholders.

- The corporation must adopt a permissible tax year, such as the calendar year, unless exceptions apply.

IRS Guidelines and Instructions

The Internal Revenue Service (IRS) provides detailed instructions for completing Form 2553 accurately:

- IRS guidelines elaborate on completing the form’s sections.

- Specific instructions help identify eligible shareholders and address potential edge cases.

References for IRS Assistance

- Consultation of IRS Form 2553 instructions is recommended for further clarification.

- The IRS provides guidance on calculating tax years and effective election dates for S corporation status.

Legal Use and Compliance

Ensuring legal compliance when using Form 2553 is crucial to maintaining the S corporation status:

- Compliance with Regulations: Corporations must adhere to specific business activities and operational standards as per IRS regulations.

- Audit Readiness: Maintain comprehensive records to promptly address potential IRS audits or inquiries regarding the election.

Key Legal Considerations

- Non-compliance or misinformation may lead to loss of S corporation status and retroactive tax adjustments.

- Timely amendments and corrections must be filed if any discrepancies are discovered.

Common Taxpayer Scenarios

Form 2553 benefits various business entities based on their unique tax situations:

- Small Businesses and Start-ups: Benefit from the pass-through taxation model, which can lead to significant tax savings.

- Family-owned Enterprises: Allows family members to share both profits and losses, potentially reducing overall tax liabilities.

Real-World Examples

- An LLC that defaults to partnership status may elect to be treated as an S corporation for tax efficiency.

- Corporations intending to expand domestic operations might leverage Form 2553 to optimize tax reporting.

Software Compatibility for Form 2553

Completing Form 2553 can be streamlined through compatible tax software:

- Tax Preparation Software: TurboTax, QuickBooks, and other popular programs often support Form 2553 filing.

- Enhanced Features: Software integration may offer error-checking features to ensure compliance and accuracy.

Technological Advantages

- Utilizing software minimizes manual errors and provides access to regularly updated tax law changes.

- Importing existing corporate data can further expedite the filing process, improving accuracy and efficiency.

By understanding and leveraging these detailed aspects of Form 2553, eligible corporations can efficiently navigate the S corporation election process and optimize their tax positions.