Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

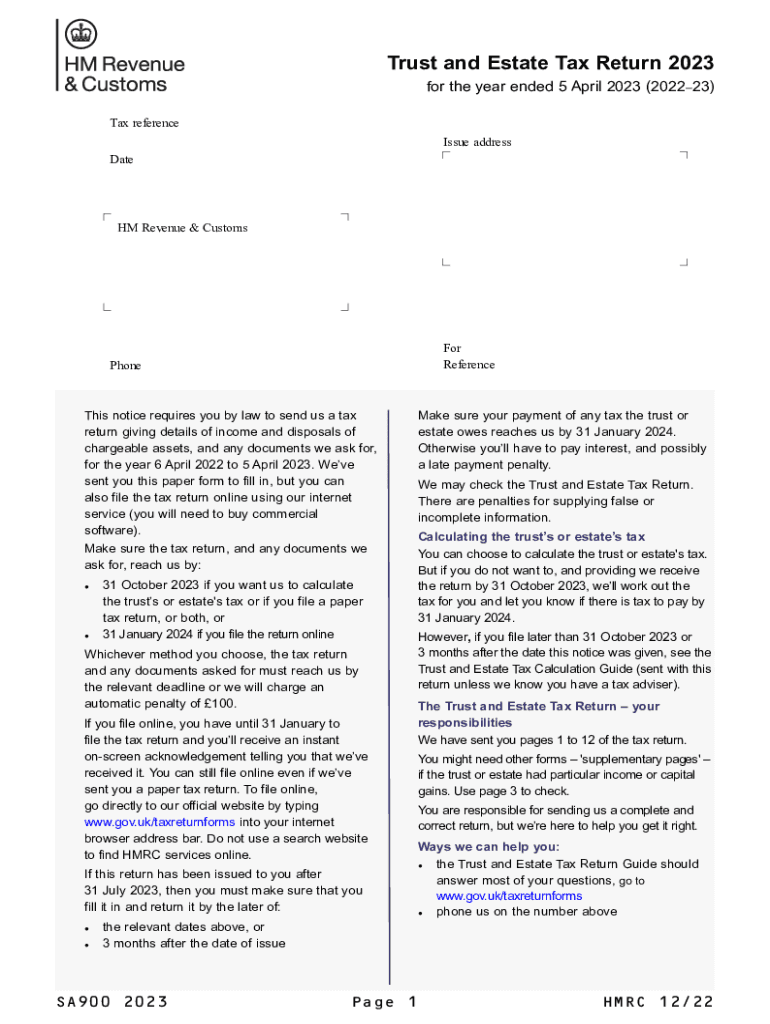

How to use or fill out sa900man Use form SA900(2023) to file a Tax Return for a trust or estate for the tax year ended 5 Ap with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open it in the editor.

Begin by entering your tax reference and issue address at the top of the form. Ensure all details are accurate.

Proceed to fill out the income and capital gains section. Answer questions regarding profits or losses from trades, partnerships, and property income as applicable.

If you need supplementary pages, check Question 23 and download them directly from our platform.

Complete any additional information required in Questions 10A through 22, ensuring all relevant fields are filled accurately.

Review your entries for completeness and accuracy before submitting. Sign the declaration at the end of the form.

Start using our platform today to streamline your tax return process for free!

Fill out sa900man Use form SA900(2023) to file a Tax Return for a trust or estate for the tax year ended 5 Ap online It's free

See more sa900man Use form SA900(2023) to file a Tax Return for a trust or estate for the tax year ended 5 Ap versions

We've got more versions of the sa900man Use form SA900(2023) to file a Tax Return for a trust or estate for the tax year ended 5 Ap form. Select the right sa900man Use form SA900(2023) to file a Tax Return for a trust or estate for the tax year ended 5 Ap version from the list and start editing it straight away!

fill in a Trust and Estate Tax Return (form SA900) and post it to HMRC by the 31 October of the following tax year. send a return online using tax software that supports SA900 reporting by 31 January of the following tax year.

What form do you use to file taxes for a trust?

Form 1041, U.S. Income Tax Return for Estates and Trusts PDF, is used by the fiduciary of a domestic decedents estate, trust, or bankruptcy estate to report: Income, deductions, gains, losses, etc.

What is the software for SA900?

Andica SA900 Trust and Estate tax returns software assists you with completion, calculation of trust and estate tax liabilities and online submission of the returns. Software can be used by personal representatives of a deceased person and their estate, trustees of a trust or tax advisors.

Do I need to complete a SA900?

After youve registered an estate HMRC will send you a UTR for the estate within 15 working days. Use this to either: fill in a Trust and Estate Tax Return (form SA900) and post it to HMRC by the 31 October of the following tax year.

Is it easy to do your own self-assessment?

It is not so difficult if you are self-employed. You just need to prepare some documents and data for it. You can go to the website and fill in your details for a self-assessment tax return. The procedure is very easy.

Related Searches

Where to send trust tax returnTrust tax return softwareSA903When does the administration period of an estate endSA905SA904Deadline for trust tax returns 2024SA907

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

Regardless of the type of income received by the trust, you are treated as receiving one type of income trust income. If you complete a tax return each year, you need to include the income on the Trusts etc pages.

Does a trust have to file a tax return every year?

Q: Do trusts have a requirement to file federal income tax returns? A: Trusts must file a Form 1041, U.S. Income Tax Return for Estates and Trusts, for each taxable year where the trust has $600 in income or the trust has a non-resident alien as a beneficiary.

What is the IRS filing deadline for trusts?

More In File For example, for a trust or estate with a tax year ending December 31, the due date is April 15 of the following year. A trust or estate with a tax year that ends June 30 must file by Oct. 15 of the same year.

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.