Definition and Purpose of 2015 Form 1094-C

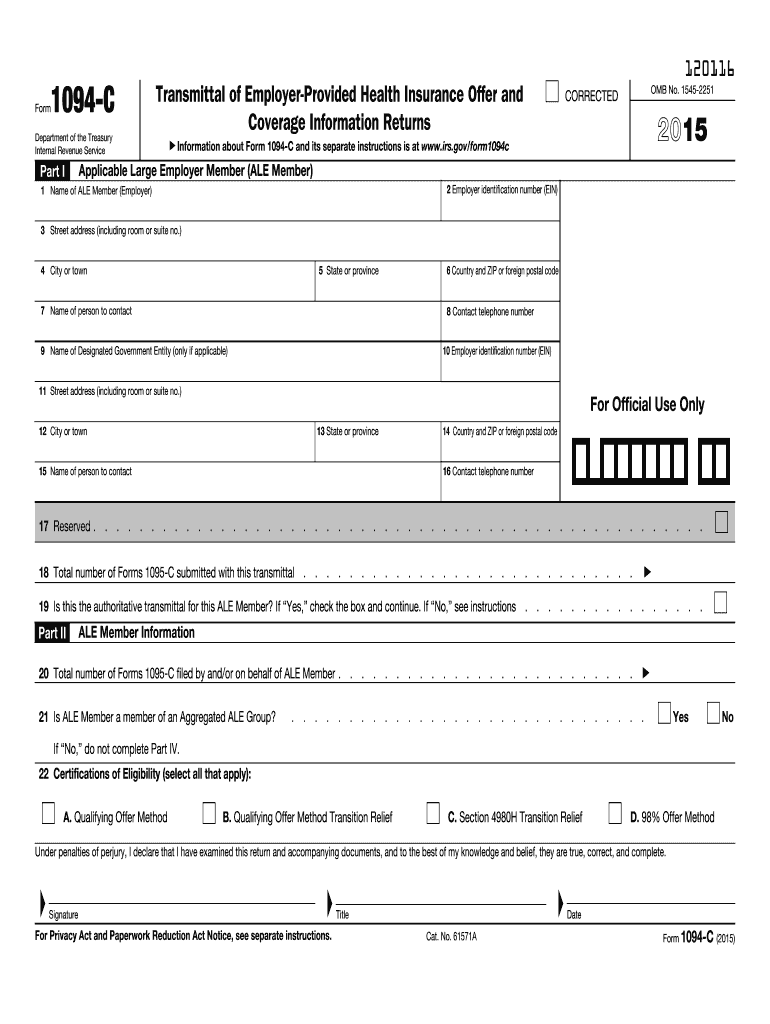

Form 1094-C serves as a transmittal document submitted by Applicable Large Employers (ALEs) to the IRS. It is used to report essential information about health insurance offers and coverage, adhering to regulatory requirements under the Affordable Care Act (ACA). Specifically, the form communicates details about the health plans offered by employers, the number of full-time employees, and certifications of eligibility. This informs the IRS about the employer's compliance with ACA mandate provisions, ensuring transparency in health coverage and assisting with the enforcement of penalties for noncompliance.

How to Use the 2015 Form 1094-C

Employers should start by gathering accurate data regarding their full-time employees and health care coverage options. Form 1094-C is to be completed alongside Form 1095-C for individual employees. It consolidates all individual form submissions into one report for the IRS. While handling this form, employers must ensure correctness in filling out sections related to employer identification, total forms being submitted, and eligibility certifications. Familiarity with specific reporting guidelines and attention to detail during this process are imperative to avoid fines.

Detailed Steps to Complete

- Gather Information: Compile data concerning each staff member's health coverage status and your organization's employer identification number (EIN).

- Fill out Form Details:

- Begin with sections requiring employer identification details.

- Progress to part II, including information about offered health insurance coverage and various certifications.

- Review and Submit: After inputting all necessary information, thoroughly check for accuracy before submission.

Filing Deadlines and Important Dates

Timeliness is crucial when filing Form 1094-C. For the year 2015, the form was due to the IRS by February 28, 2016, if filed on paper, or by March 31, 2016, if submitted electronically. Employers must maintain strict adherence to these deadlines to avoid penalties and ensure compliance with IRS regulatory frameworks. Keeping updated with yearly deadlines is vital for organizational compliance, as dates may change due to policy adjustments.

Key Elements of the 2015 Form 1094-C

This form includes several fundamental sections designed to capture comprehensive data for IRS analysis:

- Part I - Employer Information: Basic details about the employer, such as name, EIN, and contact information.

- Part II - ALE Member Information: Details concerning the type of health insurance coverage and total number of 1095-C forms filed.

- Part III - ALE Member Certification of Eligibility: Clarification on whether the employer is eligible for various reliefs under ACA regulations.

- Part IV - Other ALE Members of Aggregated ALE Group: Additional information for those part of larger conglomerate groups if applicable.

Obtaining the 2015 Form 1094-C

Employers can obtain Form 1094-C directly from the IRS website. It is crucial to ensure usage of the correct year-specific form to meet exact reporting requirements. The form is available as a downloadable PDF, which can be printed and filled manually or completed digitally if software compatibility exists. This accessibility facilitates straightforward submission, aiding in timely filing.

Penalties for Non-Compliance

Failure to accurately file Form 1094-C or to submit it on time can lead to a variety of penalties. For incorrect or incomplete forms, employers may face fines, escalating with the degree of non-compliance. Penalty relief might be granted if an employer can demonstrate reasonable cause. Staying abreast of penalty guidelines ensures employers mitigate risks associated with potential misreporting.

Software Compatibility and Filing Methods

Form 1094-C may be completed using various tax preparation software, including well-known platforms such as TurboTax and QuickBooks. These software options enhance efficiency by facilitating seamless data input and integration with digital filing systems. The form can be filed electronically via IRS-approved e-file providers, offering a more expedited and efficient filing process compared to mailing paper forms.

IRS Guidelines and Compliance

The IRS mandates that ALEs make precise, timely filings of Form 1094-C in conjunction with Form 1095-C. Understanding the IRS guidelines ensures that employers remain compliant and evade penalties. For in-depth information, employers should refer to IRS documentation and updates that provide comprehensive guidance on the form's filing protocols. Remaining informed of any changes to requirements or policies each tax year is necessary for ongoing compliance.