Definition and Meaning of Mortgage 3rd Authorization

A mortgage 3rd authorization refers to a specific document designed to allow a borrower to grant permission to a third party, such as a family member, friend, or financial advisor, to obtain or discuss confidential loan and mortgage information on their behalf. This authorization is essential for individuals who may need assistance in managing the complexities of mortgage processes or wish to delegate this responsibility to someone they trust.

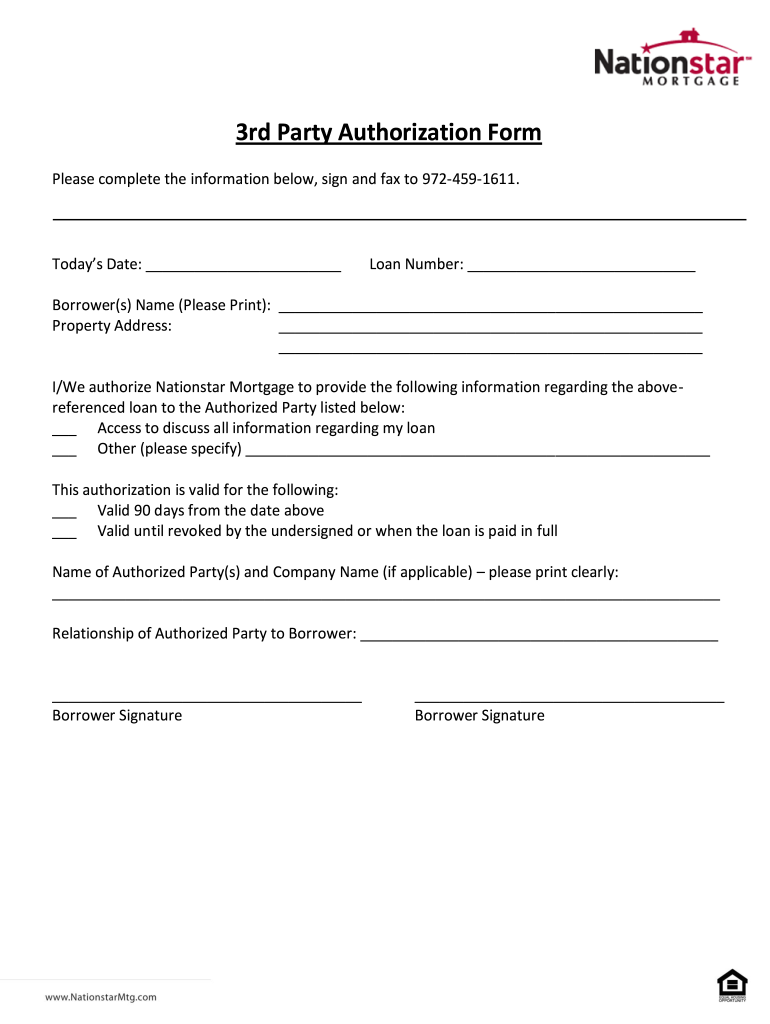

Typically, the document includes critical details such as the borrower’s information, loan number, and the name of the authorized representative. By filling out and signing the mortgage 3rd authorization, the borrower ensures that the specified third party can interact with the mortgage lender, obtain necessary details, and facilitate any required transactions related to the mortgage account.

Key Features of the Mortgage 3rd Authorization

- Confidentiality Protection: This authorization protects sensitive information by clearly outlining who has access to specific loan data.

- Time-Limited Authorization: Borrowers can set the duration of authorization, commonly allowing it for 90 days, but may revoke it earlier if desired.

- Verification of Identity: The form may require the borrower’s signature and potentially additional identification to validate authorization requests.

- Accessibility: Many lenders provide a standardized form or may require a written authorization letter to accommodate various borrower situations.

How to Use the Mortgage 3rd Authorization

Using a mortgage 3rd authorization form is straightforward, involving several primary steps that ensure both the borrower and the authorized party understand their rights and responsibilities. Properly utilizing this form can expedite communication between the borrower and mortgage lenders, simplifying the process of managing a mortgage.

Steps for Effective Use

- Obtain the Appropriate Form: Access the mortgage 3rd authorization form from your lender or a reputable online template. It's crucial to use a form that aligns with the lender's requirements.

- Complete Borrower Information: Fill in your full name, address, and social security number. Accurate details ensure that your request is processed without issues.

- Identify the Authorized Party: Clearly state the full name, relationship to you, and contact information of the authorized individual. This allows the lender to verify and recognize the third party.

- Specify the Scope of Authorization: Outline what information the authorized party can access or discuss on your behalf. Ensuring clarity here can prevent misunderstandings later.

- Sign and Date the Form: Your signature is crucial to validate the authorization. Some lenders may also require witnessing or notarization, depending on their policy.

Steps to Complete the Mortgage 3rd Authorization

Completing a mortgage 3rd authorization accurately is vital for successful processing. By following detailed steps, you can ensure that all necessary information is properly submitted.

Detailed Steps

- Gather Required Information: Collect necessary documents such as your mortgage loan number and any identification required by your lender.

- Download or Request the Form: If you do not have the form, reach out to your lender to obtain it, or find a verified template online.

- Fill in Your Details: Accurately enter your personal details, including name, address, and any additional identifiers required by your lender.

- Provide Authorized Party's Information: Enter the details of the authorized individual, ensuring you include any relevant identification numbers if needed.

- Review and Edit: Check the form for completeness and accuracy. Any incorrect data may delay the authorization process.

- Sign the Document: After reviewing, sign the document and date it. If required, have the form notarized or witnessed according to the lender's rules.

- Submit the Form: Deliver the completed form as directed by your lender, which may include online submission, mailing, or in-person delivery.

Importance of Mortgage 3rd Authorization

The mortgage 3rd authorization serves several purposes that can significantly benefit both the borrower and the lender during the mortgage process. Understanding its importance can help borrowers make informed decisions.

Advantages of Authorization

- Facilitates Communication: It streamlines the communication process between the lender and the third party, eliminating misunderstandings or delays.

- Empowers Borrowers: Borrowers can entrust their mortgage dealings to knowledgeable individuals without losing control over the final decisions.

- Ensures Compliance: By having a third party authorized, the lender remains compliant with privacy laws while addressing inquiries related to loan details.

Who Typically Uses the Mortgage 3rd Authorization?

The mortgage 3rd authorization is commonly utilized by various individuals and parties who may benefit from delegating mortgage-related tasks. Understanding the demographics that use this form can clarify its importance.

Key Users

- First-time Homebuyers: Individuals entering the mortgage process who may lack familiarity with loan terms often enlist help from parents or financial advisors.

- Seniors: Older adults may rely on caregivers or family members for assistance with their mortgage, necessitating this authorization.

- Trustees and Executors: Those managing estates or trust funds often use this form to engage with mortgage providers on behalf of beneficiaries.

- Investors: Real estate investors who delegate property management or financing tasks to agents or representatives frequently utilize this form to maintain effective communication.

Important Terms Related to Mortgage 3rd Authorization

Understanding key terms associated with the mortgage 3rd authorization can help borrowers navigate the documentation and processes involved in their mortgage journey.

Key Terminology

- Authorization: A formal consent that allows a designated party to act on the borrower's behalf concerning loan information access.

- Third Party: An individual or entity that is neither the borrower nor the lender, authorized to handle specific duties regarding the mortgage.

- Lender: The financial institution or entity providing the mortgage loan, responsible for reviewing authorization requests.

- Borrower: The individual who takes out the mortgage loan, holding the primary responsibility for loan repayment.

Legal Use of the Mortgage 3rd Authorization

The legal framework surrounding the mortgage 3rd authorization emphasizes compliance with privacy and data protection laws. Recognizing the legal context of this authorization aids borrowers in understanding their rights and responsibilities.

Regulatory Considerations

- Privacy Laws: The authorization must adhere to the Gramm-Leach-Bliley Act and other privacy regulations, ensuring that borrower information is kept confidential and only shared with authorized parties.

- Contractual Agreement: The mortgage 3rd authorization functions as a binding contract between the borrower and the lender, detailing the scope of information shared with the third party.

- Revocation Rights: Borrowers retain the right to revoke this authorization at any time, typically requiring a written notice submitted to the lender.