Definition & Meaning

Form 1098-E, also known as the Student Loan Interest Statement, is a vital document in the United States tax system. It is used to report the amount of student loan interest a borrower has paid during the tax year. This form is primarily utilized by individuals who make payments on qualified student loans, as the IRS allows for a potential deduction based on this interest. Lenders, such as banks or financial institutions that receive interest payments above a certain threshold, are required to provide this form to borrowers and the IRS.

How to Use the 1098-E Form 2017

Understanding Your Deduction

The 1098-E form allows taxpayers to claim a student loan interest deduction on their federal income tax returns. Eligible borrowers can deduct up to $2,500 of interest paid on qualified student loans. However, this deduction is an adjustment to income, meaning it can be claimed even if the taxpayer does not itemize deductions.

Reporting Interest Paid

To utilize the form, taxpayers must include the reported interest on their tax return. This interest figure is usually found in Box 1 of the form. Taxpayers should ensure that the amounts reported and claimed are accurate, as discrepancies could lead to issues with the IRS.

Steps to Complete the 1098-E Form 2017

- Receive the Form: Ensure that your lender provides you with Form 1098-E by mail or electronically by January 31 following the end of the tax year.

- Review the Information: Check all details on the form, including your name, address, and social security number, to ensure they match IRS records.

- Include in Tax Filing: Use the information in Box 1 to report student loan interest paid. This is entered on the relevant line of your federal income tax return.

- Maintain Records: Keep a copy of the 1098-E and any related documentation with your tax records for future reference.

How to Obtain the 1098-E Form 2017

Lenders typically send Form 1098-E to borrowers who have paid $600 or more in student loan interest over the course of the year. Borrowers should check their mail for physical forms or check their email and online accounts with lenders for electronic versions. If you do not automatically receive the form, contact your lender directly to request it.

Who Typically Uses the 1098-E Form 2017

Borrowers repaying student loans that qualify as education loans under IRS regulations are the primary users of Form 1098-E. These individuals primarily include college graduates and other individuals who have undertaken post-secondary education financing. Additionally, co-signers making payments on such loans may also utilize this form for tax purposes.

IRS Guidelines

The IRS permits a student loan interest deduction subject to income limits. For single filers, the deduction phases out for modified adjusted gross income (MAGI) between $65,000 and $80,000 ($135,000 and $165,000 for joint filers). It is essential for taxpayers to confirm that their income does not exceed these limits to claim the deduction.

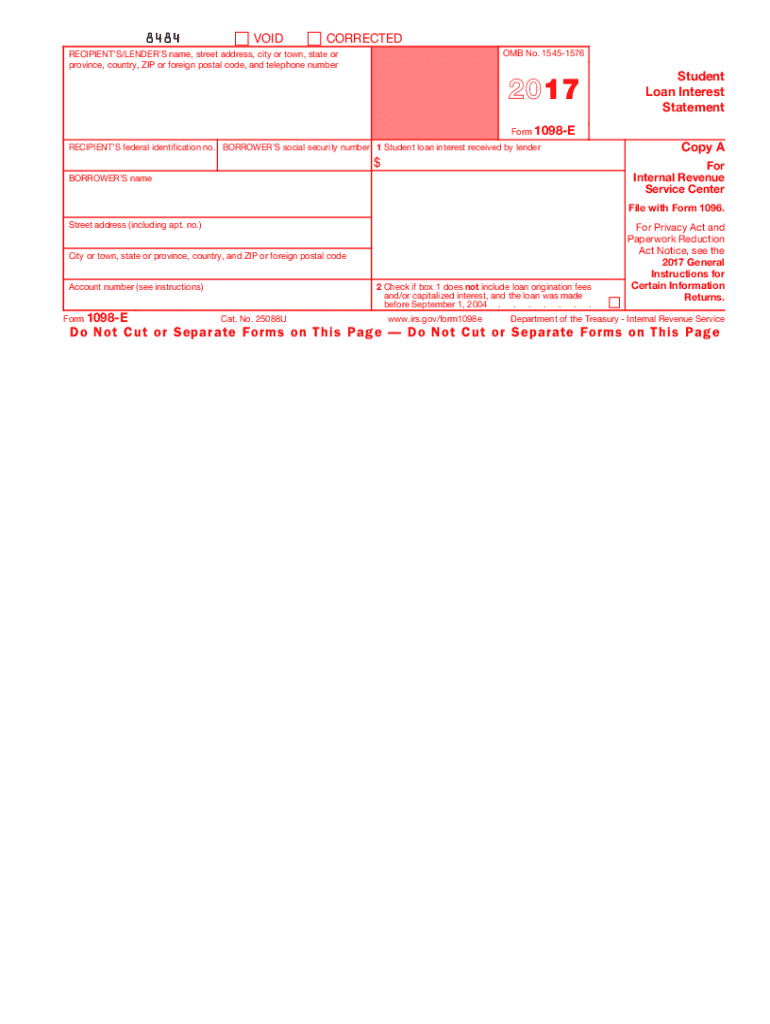

Key Elements of the 1098-E Form 2017

- Lender Information: The name and contact details of the financial institution reporting the paid interests.

- Student Loan Interest: The total amount of interest paid during the tax year, usually captured in Box 1.

- Borrower Information: Details such as name, address, and taxpayer identification number.

Penalties for Non-Compliance

Failing to report the interest paid as documented in Form 1098-E, or misreporting amounts, can result in penalties or interest accruing on unpaid tax amounts. Taxpayers should adhere to submission deadlines and ensure accurate reporting to avoid such consequences.

Digital vs. Paper Version

Borrowers often have the option to receive Form 1098-E electronically or in paper form. Many lenders provide digital forms via secure online accounts, which can expedite the form receipt process. Concurrently, paper copies serve those preferring traditional mail receipt or lacking digital access.

By adhering to the above guidance, taxpayers can ensure they accurately utilize the 1098-E form in their tax filings, maximizing their potential deductions and maintaining compliance with IRS regulations.