Definition & Meaning of Form 8606

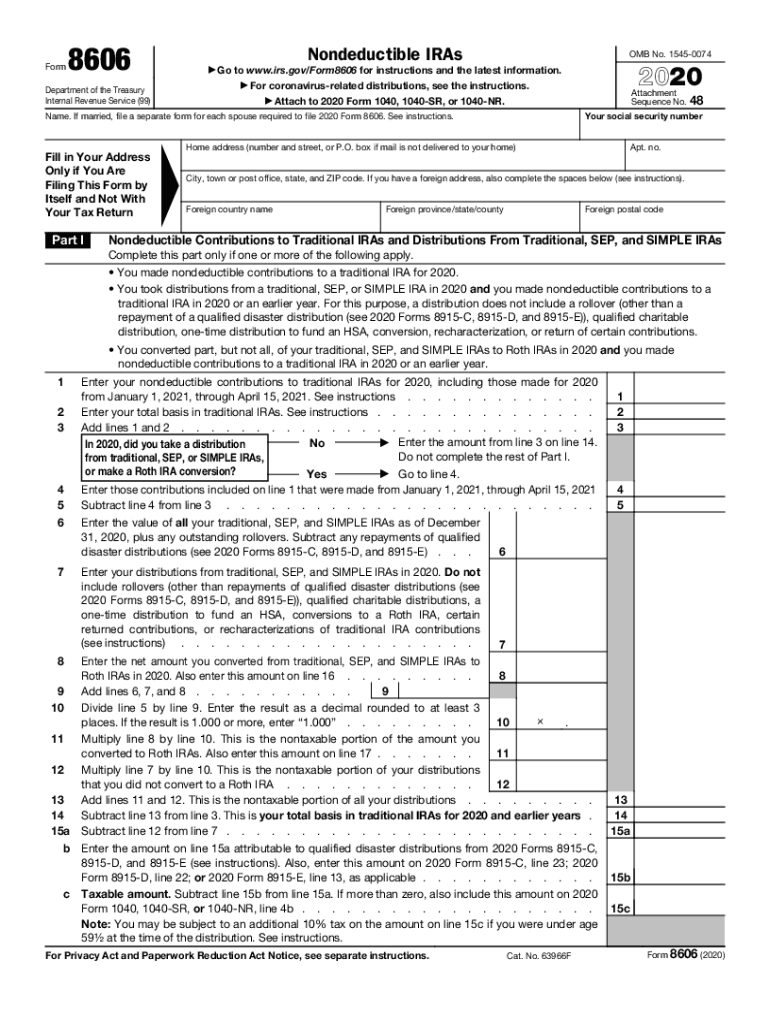

Form 8606 is a tax form used by individuals in the United States to report nondeductible contributions made to traditional IRAs. It is also used for reporting distributions from traditional, SEP, and SIMPLE IRAs when part of the distribution is not taxable. Additionally, the form tracks conversions from traditional IRAs to Roth IRAs and distributions from Roth IRAs that are not qualified. The purpose of Form 8606 is to ensure that taxpayers and the IRS maintain accurate records of after-tax contributions and distributions, helping to ascertain which parts of distributions are taxable and which are not. Understanding this form is crucial for compliance with IRS regulations and ensuring accurate tax reporting on individual returns.

How to Use Form 8606

-

Reporting Nondeductible Contributions: Use Part I of the form to report any nondeductible contributions to traditional IRAs. This helps the IRS track the portion of the IRA that has already been taxed, thus not subject to further taxation upon distribution.

-

Conversions to Roth IRAs: In Parts II and III, report conversions from traditional IRAs to Roth IRAs. This section is critical because conversions may be partially or fully taxable.

-

Distributions from Roth IRAs: Report non-qualified distributions from Roth IRAs to determine if any portion of the distribution is taxable or subject to additional penalties.

-

Distributions from Traditional IRAs: If distributions include both deductible and nondeductible contributions, calculate the taxable and non-taxable amounts to avoid being taxed on previously taxed contributions.

Practical Example

Assume you make a $5,000 nondeductible contribution to your traditional IRA. On Form 8606, you report this in Part I to ensure this contribution is not taxed again in the future.

Steps to Complete Form 8606

-

Gather Necessary Documents: Collect relevant information such as IRA contribution records, conversion details, and previous years' Form 8606, if applicable.

-

Complete Part I: Enter your nondeductible contributions for the tax year. Record any carried forward contributions from previous years.

-

Fill Out Part II When Applicable: Report any conversions to Roth IRAs. Ensure accurate reporting of amounts to be converted to prevent miscomputation of taxable income.

-

Enter Relevant Information in Part III: This part applies if you took distributions from Roth IRAs or want to determine the taxable portion.

-

Review for Accuracy: Carefully check all entries for correct calculations and data accuracy to ensure compliance and avoid IRS scrutiny.

Who Typically Uses Form 8606

Form 8606 is primarily used by individuals who:

- Make nondeductible contributions to traditional IRAs.

- Convert traditional IRAs to Roth IRAs.

- Take non-qualified distributions from Roth IRAs.

- Need to accurately track and report both deductible and nondeductible IRA contributions over time.

It is particularly relevant for taxpayers with retirement savings strategies involving multiple types of IRAs, especially those planning Roth conversions or managing after-tax contributions.

Legal Use of Form 8606

Form 8606 is integral to the legal management of individual retirement accounts (IRAs) under U.S. federal tax law. Filing this form helps individuals report nondeductible contributions, Roth IRA conversions, and non-qualified distributions accurately. Correct filing can prevent issues with tax assessments and ensure compliance with IRS regulations on retirement accounts. Failure to file when required can result in penalties or increased taxes due to inaccurate reporting of taxable income.

Key Elements of Form 8606

- Part I: Focuses on nondeductible contributions and the calculation of the total basis in traditional IRAs.

- Part II: Covers conversions from traditional to Roth IRAs, important for those making strategic tax decisions regarding retirement funds.

- Part III: Pertains to distributions from Roth IRAs, ensuring only the taxable portion is declared.

- Reconciliation: Calculates the taxable portion of distributions from both traditional and Roth IRAs based on reported information.

IRS Guidelines

The Internal Revenue Service (IRS) mandates that Form 8606 must be filed by any U.S. taxpayer who makes nondeductible contributions to a traditional IRA, converts a traditional IRA to a Roth IRA, or takes nonqualified distributions from a Roth IRA. It ensures that taxable amounts are promptly and correctly reported, allowing for precise record-keeping on after-tax contributions and ensuing distributions. IRS guidelines require accurate completion of the form to maintain consistency in tax reporting.

Filing Deadlines and Important Dates

- Deadline for Filing: Form 8606 is typically due on the same date as the individual's federal income tax return, usually April 15th following the tax year in question.

- Extended Filing Date: If an extension for the tax return is filed, Form 8606 can also be submitted by the extended deadline, which is October 15th for most taxpayers.

Adhering to these deadlines ensures proper tax reporting and prevents late filing penalties related to nondeductible contributions or other IRA-related transactions.