Definition & Purpose of Form 8822-B

Form 8822-B is a document used by businesses to inform the Internal Revenue Service (IRS) about changes concerning their responsible party, mailing address, or business location. This form is crucial for entities with an Employer Identification Number (EIN) to keep the IRS updated about key business information. The responsible party is typically someone with the authority to control, manage, or direct the entity's finances and operations, such as a chief executive officer or trustee. If any changes occur regarding this role, or if there are updates to business addresses, filing Form 8822-B becomes necessary to maintain current IRS records and ensure proper correspondence for tax purposes.

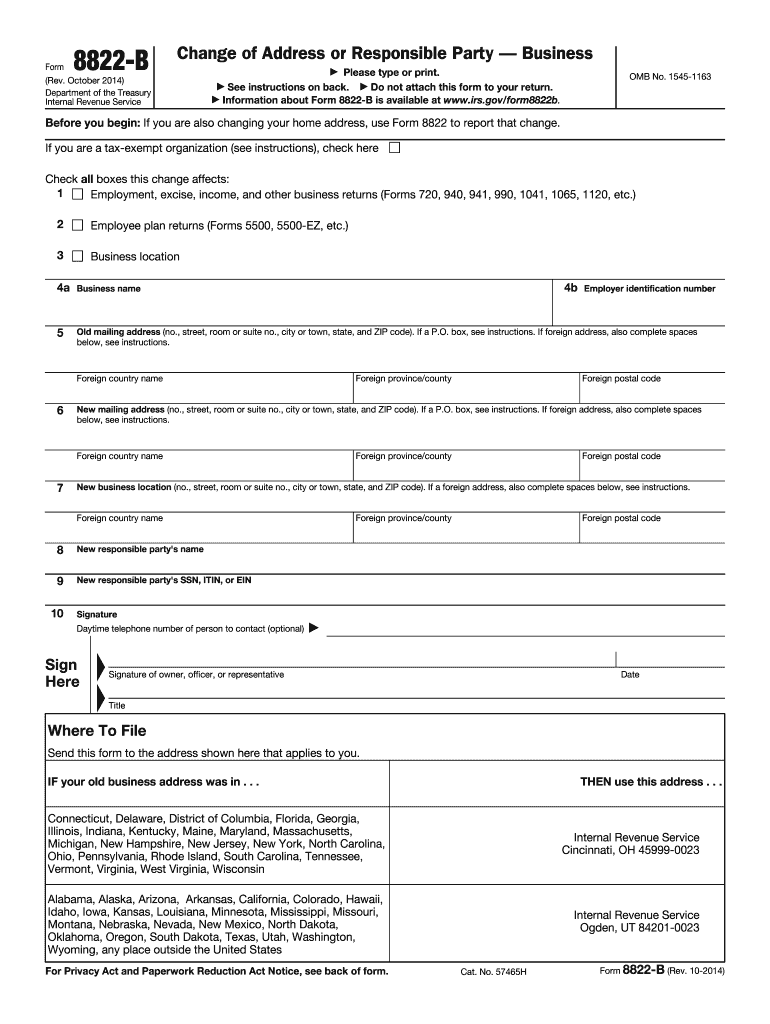

Steps to Complete Form 8822-B

To successfully complete Form 8822-B, you should follow these detailed steps:

- Obtain the Form: Access Form 8822-B from the IRS website or request a physical copy via mail.

- Provide Entity Information:

- Enter the name of your business entity and the EIN.

- Specify the old address and any new mailing or business location changes.

- Identify Responsible Party:

- Fill in the details of the new responsible party, including their name and Social Security Number or Taxpayer Identification Number.

- Additional Information:

- Include any other relevant changes or corrections to your entity's details as required.

- Signature and Date:

- Ensure the form is signed by an authorized individual, typically the new responsible party, and dated accurately.

- Submission: Submit the completed form as directed, typically via mail to the address provided in the IRS instructions.

Importance of Filing Form 8822-B

Filing Form 8822-B is essential for maintaining open and accurate communication channels with the IRS. Changes concerning a responsible party or business address can affect your business's tax filings, notices, and overall compliance. Timely filing ensures that all IRS correspondence reaches the correct party without delay, thus preventing potential miscommunication or legal penalties. Moreover, it helps safeguard your business against any discrepancies or issues that might arise from outdated information in IRS records.

Common Users of Form 8822-B

Entities typically required to file Form 8822-B include corporations, partnerships, and sole proprietorships with an EIN. Organizations undergoing structural changes, such as mergers or acquisitions that result in a new responsible party, also need to file this form. Furthermore, newly established businesses needing to update initially reported information are regular users. The form applies to any organization with a need to report changes as per IRS guidelines to remain compliant and ensure accurate tax administration.

Legal Implications and Compliance

The legal use of Form 8822-B is governed by the IRS's regulations concerning business entities. Failure to file the form within 60 days of any relevant change can result in penalties, including a $500 fine for not notifying the IRS of a change in the responsible party. This underscores the importance of understanding and adhering to the filing requirements. Compliance not only avoids potential financial penalties but also maintains the integrity of your business records with the IRS.

Key Elements of the Form

Form 8822-B is structured to collect specific information essential for updating IRS records accurately:

- Identification Section: Requires details about the business entity, such as the name and EIN.

- Address Change Details: Includes sections to report old and new addresses for mailing and business locations.

- Responsible Party Information: Identifies the new responsible party, their role, and pertinent identification numbers.

- Signatures: A section for the signature of an authorized representative is crucial for validation.

Each section is vital in ensuring a comprehensive update is provided to the IRS, thus preventing complications.

IRS Guidelines and Filing Deadlines

According to IRS guidelines, Form 8822-B must be filed within 60 days following a change in the identity of the responsible party or business address. Filing beyond this period can result in penalties. It is advisable to consult the latest IRS publications or seek professional legal advice regarding any specific filing instructions or updates to guidelines to ensure full adherence to the regulations.

Submission Methods and Considerations

Currently, Form 8822-B is filed via mail. It’s important to ensure that you use the correct mailing address based on your business's location as per the IRS instructions to avoid delays. While online filing isn't available for this form, it’s crucial to retain copies of the form and any related correspondence for your records. Consideration should also be given to employing certified mail services to provide proof of submission and ensure timely processing.

By addressing the necessary sections and adhering to the IRS's requirements, businesses can maintain compliance and avoid penalties, ensuring seamless communication with the IRS.