Definition and Purpose of Form 8606 for 2016

Form 8606, officially known as the Nondeductible IRAs form, is required by the IRS to report nondeductible contributions to traditional IRAs and certain distributions or conversions that occur during the tax year. In 2016, this form was crucial for taxpayers who made after-tax contributions to their IRAs, as it helped determine the taxable part of these distributions. The primary role of Form 8606 is to ensure proper tracking of IRA contributions that aren't deducted on tax returns, helping avoid double taxation in the future.

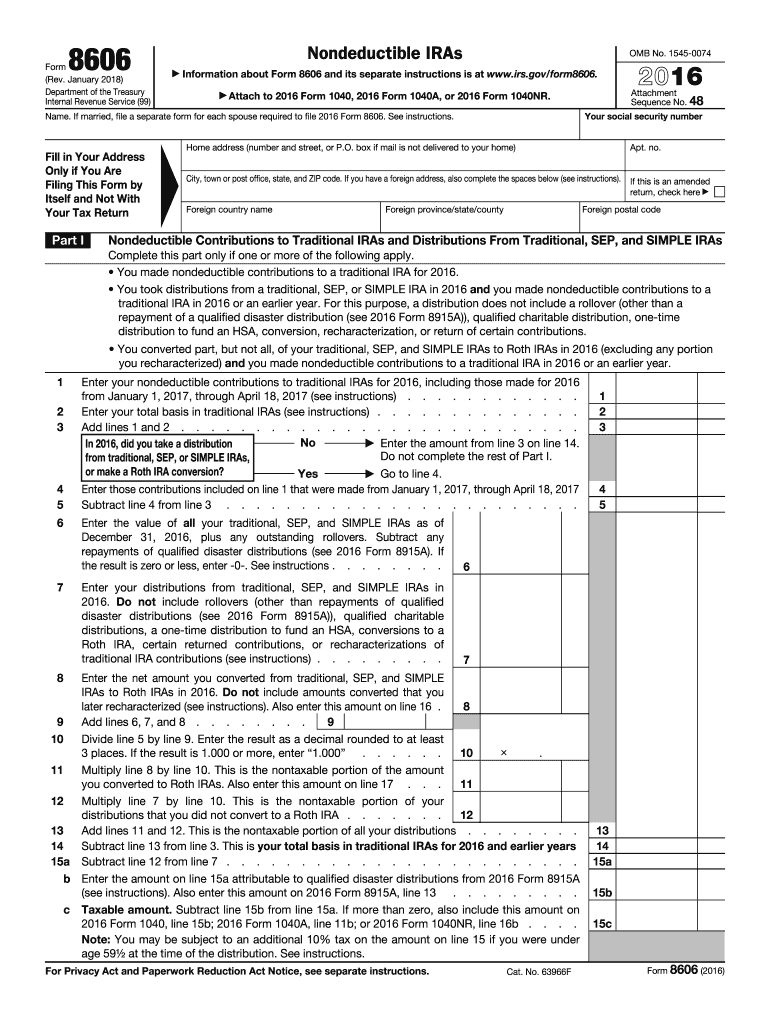

Essential Elements of Form 8606 for 2016

The form includes several critical sections that users need to understand:

- Nondeductible Contributions: Users must report their nondeductible contributions to traditional IRAs, ensuring that these are accurately recorded and distinguished from deductible contributions.

- Roth IRA Conversions: Details on conversions from traditional IRAs to Roth IRAs are required, including the conversion amount.

- Distributions: The form asks for specifics on distributions from traditional, SEP, SIMPLE, and Roth IRAs to calculate the taxable portion.

For taxpayers who only have nondeductible IRAs, reporting using Form 8606 is mandatory, ensuring that the IRS has a clear record of all contributions and distributions.

How to Obtain the 8606 Form for 2016

You can acquire Form 8606 for the 2016 tax year directly from the IRS website. It's essential to have the correct year version to ensure accurate reporting, as tax regulations and form requirements might vary from year to year. Alternatively, tax software such as TurboTax may provide access to the relevant form when filing annual tax returns.

Detailed Steps to Complete the 8606 Form for 2016

- Gather Required Information: Before filling out the form, ensure you have details about all contributions and conversions, as well as your previous year's Form 8606.

- Complete Part I: Report nondeductible contributions made to traditional IRAs. This section determines the basis in traditional IRAs.

- Complete Part II: If applicable, fill this part for Roth IRA conversions, recording the amounts converted from traditional IRAs.

- Complete Part III: This section is for taxpayers who have distributed from Roth IRAs and who may owe taxes on earnings.

- Sign and Submit: Once filled, ensure accuracy by reviewing, signing the document, and attaching it to your tax return if required.

IRS Guidelines and Compliance

The IRS provides specific instructions that accompany Form 8606 to ensure taxpayers can accurately complete and submit it. It is critical to comply with these guidelines to avoid penalties and to ensure the proper tracking of IRA contributions and conversions.

Penalties for Non-Compliance

Failing to file Form 8606 when required may result in a $50 penalty per missed form submission. Additionally, inaccurately reporting your nondeductible contributions can lead to further complications. Therefore, it's essential to complete and file this form accurately and timely.

Who Typically Uses Form 8606

This form is commonly used by individuals who:

- Made nondeductible contributions to a traditional IRA during the tax year

- Converted amounts from a traditional IRA to a Roth IRA

- Took distributions from a Roth IRA but not for five years

These individuals must report using Form 8606 to ensure proper tax treatment of their IRA-related transactions.

Eligibility Criteria for Filing Form 8606

To be required to file this form, the following conditions generally must be met:

- You made nondeductible contributions to your traditional IRA

- You received distributions from an IRA that exceed your basis

- You completed a Roth IRA conversion

This eligibility ensures that all applicable taxpayers properly report IRA transactions that could impact their taxes.

Form Submission Methods

You can submit Form 8606 via electronic filing along with your federal tax return using tax software like TurboTax. In certain cases, individuals may choose to submit a paper form through mail. Understanding these submission options ensures you can choose the most convenient and efficient method for your situation.

Software Compatibility for Form 8606

Several popular tax preparation software, including TurboTax and QuickBooks, support the filling out and submission of Form 8606. These platforms can simplify the process through automation and built-in compliance checks, reducing errors and ensuring accuracy across filings.

Filing Deadlines and Important Dates

Form 8606 should be submitted by the standard tax due date for the applicable tax year. For 2016, this typically fell in April 2017. Keeping track of such deadlines is crucial to avoiding penalties and ensuring every aspect of your tax filing is timely and complete.

Variations and Alternatives to Form 8606 for 2016

While Form 8606 serves a specific purpose, variations and related forms may be necessary depending on your unique financial situation or changes in tax laws. It's essential to verify with a tax professional or the IRS whether any updates or different forms apply to your circumstances for 2016.