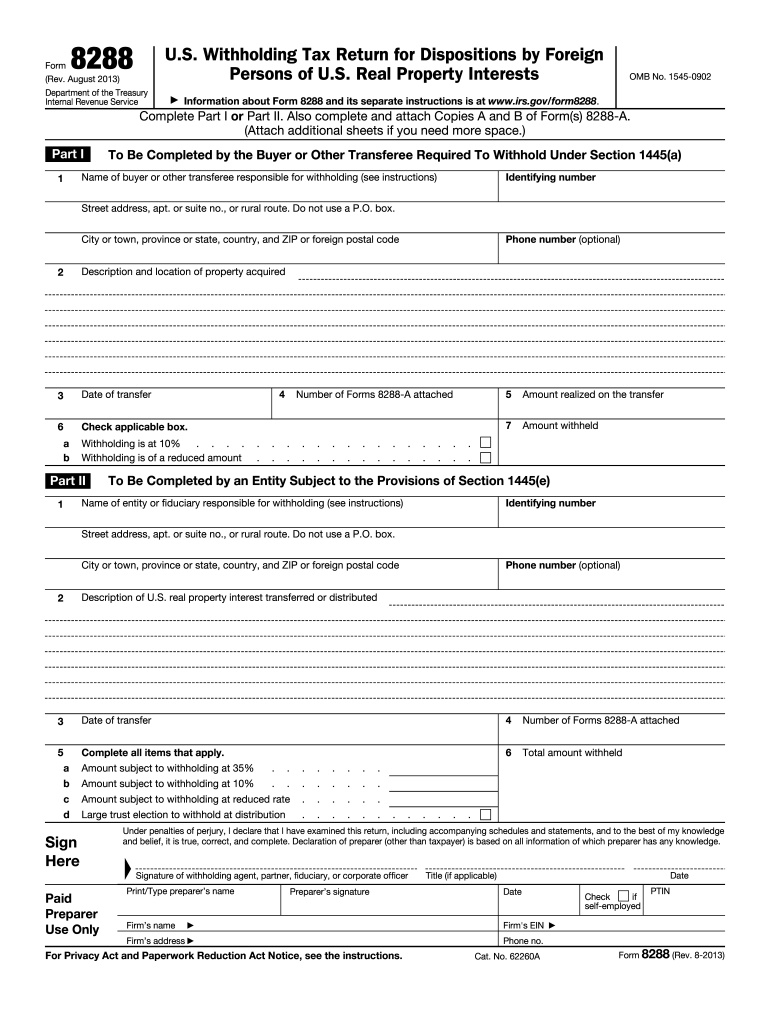

Definition and Purpose of IRS Form 8288

IRS Form 8288, commonly used in 2013, is a U.S. Withholding Tax Return required by foreign persons disposing of U.S. real property interests. Under Section 1445(a) of the Internal Revenue Code, this form mandates that buyers or transferees report the acquisition and withhold a specified percentage of the proceeds for tax purposes. It encompasses various sections to accurately capture the buyer's identification, detailed property information, the transfer date, and the amount withheld. Completing this form correctly is crucial to ensuring compliance with U.S. tax laws for foreign transactions involving real estate.

Step-by-Step Instructions for Completing IRS Form 8288

-

Identify the Parties Involved:

- Clearly list the buyer's or transferee's information.

- Include the seller's or transferor's name and taxpayer identification numbers.

-

Provide Property Information:

- Enter a description of the property, including the address and specific details.

- Note the date of transfer and the total consideration paid for the property.

-

Calculate and Enter Withholding Amount:

- Use applicable percentages to determine the withholding amount based on the total sales price.

- Ensure all calculations are clearly documented within the designated sections.

-

Final Steps:

- Review the form for any errors or missing information.

- Sign and date the form before submission.

How to Obtain IRS Form 8288

-

Online Access:

- Download the form directly from the Internal Revenue Service website. This option provides the most current version and any related instructions.

-

Paper Copies:

- Request a paper form by contacting the IRS directly or visiting an IRS office.

Who Typically Uses IRS Form 8288

This form is primarily used by foreign individuals or entities involved in the sale of U.S. real property interests. Real estate professionals, buyers, and transferees are common users, often working in conjunction with legal or financial advisors to ensure compliance with relevant tax laws. Understanding the role of each party is crucial, as misreporting can result in significant penalties.

Key Elements of IRS Form 8288

-

Proper Identification:

- Full names, addresses, and taxpayer identification numbers (TIN) for both the buyer and seller.

-

Transaction Details:

- Exact property address, brief description, and associated sale particulars.

-

Withholding Information:

- Specific instructions on calculating the withholding tax under FIRPTA guidelines (Foreign Investment in Real Property Tax Act).

Important Terms Related to IRS Form 8288

-

FIRPTA: A U.S. tax law requiring foreign persons to pay taxes on the disposition of real property interests at the point of sale.

-

TIN: Taxpayer Identification Number, a required piece of information that helps track tax obligations for both buyers and sellers.

-

Withholding Agent: The entity responsible for withholding the appropriate tax amount and submitting it to the IRS as part of the transaction process.

Legal Use of IRS Form 8288

The legal framework surrounding IRS Form 8288 ensures accurate reporting and tax compliance for international parties involved in U.S. property transactions. Ensuring the correct completion and timely submission of this form protects parties from potential penalties or interest charges due to non-compliance.

Filing Deadlines and Important Dates for IRS Form 8288

-

Submission Timeline:

- Typically, the form should be filed within 20 days of the property transfer. This ensures adherence to IRS guidelines and avoids late penalties.

-

Important Dates:

- Be aware of any changes to filing deadlines, particularly in the context of financial year-end processes or any IRS advisories that might affect submission rules.

Penalties for Non-Compliance with IRS Form 8288

Failure to comply with IRS Form 8288 filing requirements can result in significant penalties. These may include financial penalties based on a percentage of the required withholding, additional interest charges, and potential legal consequences. To mitigate such risks, ensure thorough understanding and adherence to all specified IRS guidelines and deadlines.

Examples of Using IRS Form 8288

-

Scenario 1: Foreign Seller:

- A non-resident alien selling a U.S. condominium must file Form 8288, with the buyer withholding 15% of the sale price for taxes.

-

Scenario 2: Corporate Sale:

- A foreign corporation disposing of an office building must comply with withholding regulations, using Form 8288 to report and remit the specified tax amount.

These detailed explanations aim to provide a comprehensive understanding of IRS Form 8288, helping users navigate its complexities effectively.