Definition & Purpose of 2017 Form 8949: Sales and Other Dispositions of Capital Assets

The 2017 Form 8949 is an Internal Revenue Service (IRS) form essential for reporting the sale and other dispositions of capital assets. This form is used to document the capital gains and losses incurred by taxpayers during a given tax year. It distinguishes between short-term and long-term transactions and requires the taxpayer to specify whether basis information was previously reported to the IRS. By capturing critical transaction details such as proceeds, dates, and adjustments to gain or loss, the form plays a central role in calculating the capital gains or losses that must be reported on a taxpayer’s Schedule D.

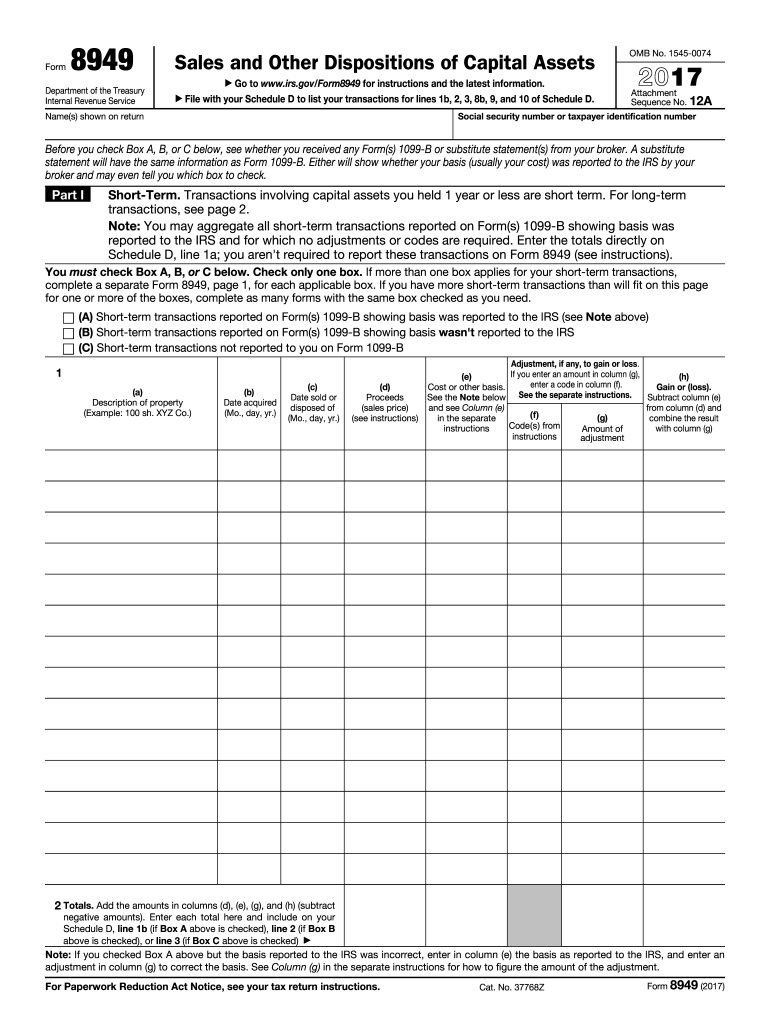

Detailed Transaction Reporting

For accurate tax reporting, the IRS mandates the inclusion of each capital asset transaction on Form 8949. This involves providing comprehensive details, such as:

- A brief description of the asset sold, such as type and quantity.

- The acquisition and sale dates, establishing if the asset was held long-term or short-term.

- Proceeds received from the sale or disposition.

- Any adjustments that affect the gain or loss, ensuring precise taxable amounts.

Steps to Complete the 2017 Form 8949

Filing the 2017 Form 8949 requires careful attention to detail. Accurate completion involves several steps:

- Gather Necessary Information: Start by collecting all relevant documents, such as brokerage statements and sales records, which provide transaction details.

- Classify Transactions: Determine if each transaction is short-term or long-term based on the holding period, usually before or after one year, respectively.

- Report Proceeds: For each transaction, record the gross proceeds received from the sale of the asset.

- Calculate Adjustments: Adjust reported gains or losses by accounting for costs such as commissions and fees, using the IRS codes for specific adjustments.

- Summarize Each Category: Tally totals for each classification to compute the overall gain or loss for short-term and long-term assets separately, as this will impact overall tax liability.

Important Terms Related to the 2017 Form 8949

Understanding key terms associated with the 2017 Form 8949 is crucial for correct usage and compliance:

- Capital Asset: Any property owned by a taxpayer for investment or personal purposes. Examples include stocks, bonds, and real estate.

- Basis: The original cost of a capital asset, vital for calculating capital gain or loss. Adjustments may increase or decrease the basis.

- Short-term vs. Long-term: Short-term refers to assets held for one year or less, while long-term applies to assets held for more than one year. Tax implications can differ significantly between these categories.

Legal Use of the 2017 Form 8949

Compliance with IRS regulations dictates the proper use of Form 8949. It is legally required for taxpayers who sell or dispose of reportable capital assets. Failing to file or misreporting can result in penalties or legal repercussions. The form accurately documents financial activities affecting tax obligations, thereby ensuring lawful adherence to tax requirements.

Form Submission Methods: Online and Paper

Taxpayers can submit the 2017 Form 8949 through various channels:

- Online Submission: Many users prefer e-filing using tax preparation software integrated with IRS systems. This streamlines data input, reduces errors, and provides quicker processing times.

- Physical Submission: Alternatively, paper filings are accepted. Taxpayers must complete the form manually and mail it to the IRS office corresponding to their state, ensuring compliance with all paper form guidelines and deadlines.

IRS Guidelines for Filing 2017 Form 8949

The IRS provides detailed guidelines to assist taxpayers in accurately completing and filing Form 8949. These guidelines encompass stipulations for:

- Grouping Transactions: Taxpayers must separate transactions not reported to the IRS from those that are, using the appropriate IRS codes.

- Adjustments and Reporting: Particular attention is required for adjusting costs and ensuring all entries are verifiable against reported amounts on brokerage statements.

- Filing with Schedule D: Form 8949 must accompany Schedule D when submitted, as it details the information summarized thereon to determine the capital gains tax.

Who Typically Uses the 2017 Form 8949

Typically, individuals or entities engaged in capital asset transactions are required to use Form 8949. This includes:

- Individual Investors: Those trading stocks, bonds, or other securities.

- Real Estate Investors: Individuals disposing of property for investment purposes.

- Business Entities: Corporations and partnerships reporting the sale of business-related capital assets must include this form in their tax documentation.

Taxpayer Scenarios Involving 2017 Form 8949

Several taxpayer scenarios necessitate the use of the 2017 Form 8949:

- Self-employed Traders: Individuals actively buying and selling for personal investment or business operations.

- Retirees with Investment Portfolios: Required to report gains or losses from asset dispositions.

- Students with Investment Income: Those earning income through part-time investing or asset sales need to disclose these transactions.

By adhering to these structured guidelines, taxpayers ensure compliance with IRS standards while effectively managing their tax obligations related to capital asset transactions.