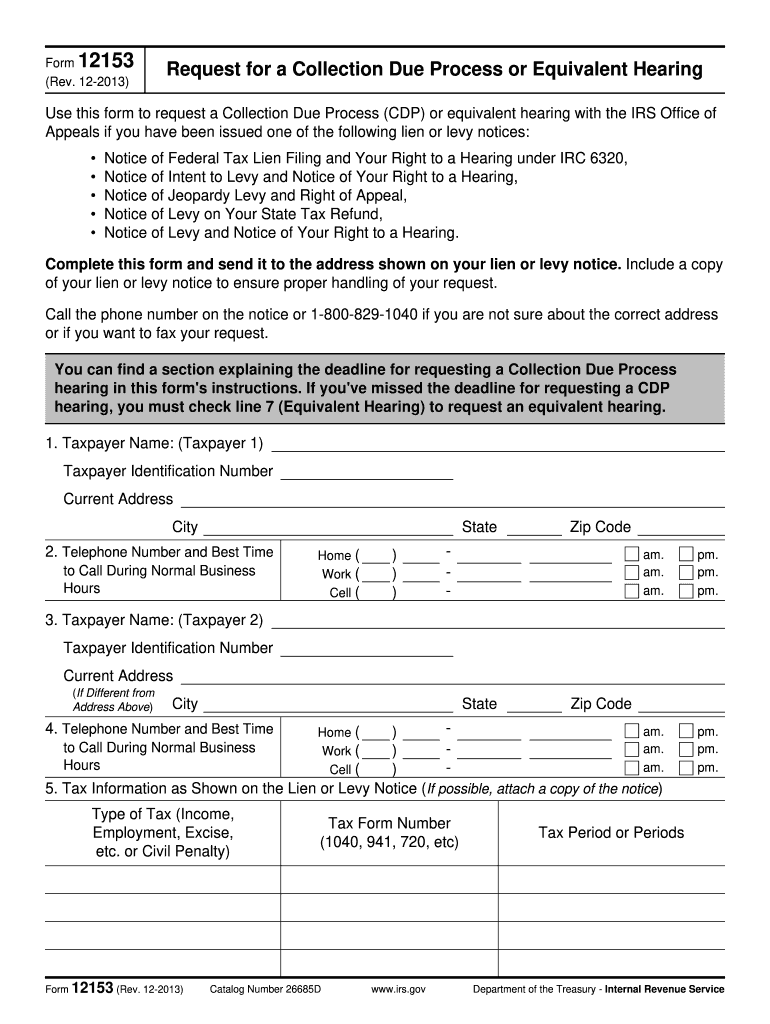

Definition & Purpose of IRS Form 12153

IRS Form 12153, known officially as the "Request for a Collection Due Process or Equivalent Hearing," serves an essential purpose for taxpayers. This form is used to formally request a hearing with the IRS Office of Appeals to contest or resolve disagreements concerning federal tax liens or levies. The collection due process hearing provides taxpayers a platform to dispute the IRS's decisions on tax collection matters, enabling an independent review of their case.

How to Use IRS Form 12153

When utilizing IRS Form 12153, it is crucial to understand the contexts in which it applies. The form is used to request a Collection Due Process (CDP) hearing when a taxpayer receives a Notice of Federal Tax Lien or a Notice of Intent to Levy. To effectively use the form:

- Complete all required sections with accurate and current information.

- Clearly specify reasons for requesting the hearing, such as disputes over tax amounts or procedural errors by the IRS.

- Attach any supporting documentation that strengthens your case.

Submitting IRS Form 12153 initiates a dialogue with the IRS Appeals Office, allowing taxpayers to present their case for reconsidering IRS actions.

Steps to Complete IRS Form 12153

Completing IRS Form 12153 requires attention to detail to ensure that your request for a hearing is considered valid and timely. Follow these steps for precision:

- Identify Your Tax Matter: Clearly state the type of tax dispute, whether it involves a lien or a levy.

- Complete Personal Information: Include your name, address, taxpayer identification number, and contact details.

- Detail Reasons for the Hearing: Provide specific reasons for disputing the IRS’s action. Detail any errors or circumstances justifying the reconsideration of the lien or levy.

- Provide Supporting Evidence: Attach relevant documents, such as financial statements or prior correspondence with the IRS, to support your claims.

- Submit the Form: Send the completed form to the appropriate IRS office, following mailing instructions provided on the form to ensure correct delivery.

These steps ensure your form is adequate for processing and follow-up by the IRS.

Filing Deadlines and Important Dates

Adhering to filing deadlines is vital when dealing with IRS Form 12153. The form must be submitted within 30 days from the date on the IRS notice to preserve your right to a CDP hearing. If you miss this deadline, you may still request an equivalent hearing, but this alternative lacks certain legal rights such as moving the case to Tax Court.

- 30-Day Deadline: Essential for a full CDP hearing request.

- Timely Submission: Protects your right to litigation options if needed.

A prompt response within set timelines preserves your appeals options and strengthens your negotiation position.

Required Documents for IRS Form 12153

Supporting documentation is a core component of a complete IRS Form 12153 submission. Essential documents include:

- Tax Notices Received: Original IRS lien or levy notices.

- Financial Records: Income statements, expense details, and bank records.

- Prior Correspondence: Any letters or forms previously exchanged with the IRS that are relevant to your case.

Including comprehensive documentation aids in clarifying your position and can expedite resolution.

Form Submission Methods (Online / Mail / In-Person)

Submitting IRS Form 12153 accurately is crucial for effective processing. The primary methods include:

- Mail: Traditional and often recommended, using certified mail for proof of submission.

- In-Person: Submission at a local IRS office ensuring receipt confirmation.

While online filing is not typical for Form 12153, it's important to adhere to the official IRS instructions provided on the form and confirmation of the accepted submission method.

Key Elements of IRS Form 12153

IRS Form 12153 includes several critical sections, each needing thorough completion:

- Your Information: Include personal and contact information.

- Reason for Request: Clearly articulate why you're requesting a hearing.

- Proposed Solutions: Suggest potential resolutions or negotiations, such as installment plans or offer in compromise.

Each element is designed to capture necessary details to allow for a thorough review by the IRS appeals office.

Legal Use of IRS Form 12153

A submitted IRS Form 12153 begins a legal process allowing you to dispute IRS collection activities. The form’s completion and submission enable:

- Protection Against Collection Actions: While pending appeal, IRS is typically prohibited from levy actions.

- Independent Review: Ensures a neutral party evaluates your case, providing a fair process for resolution.

Utilizing this form provides taxpayers with a structured method to legally dispute and resolve tax collection issues.