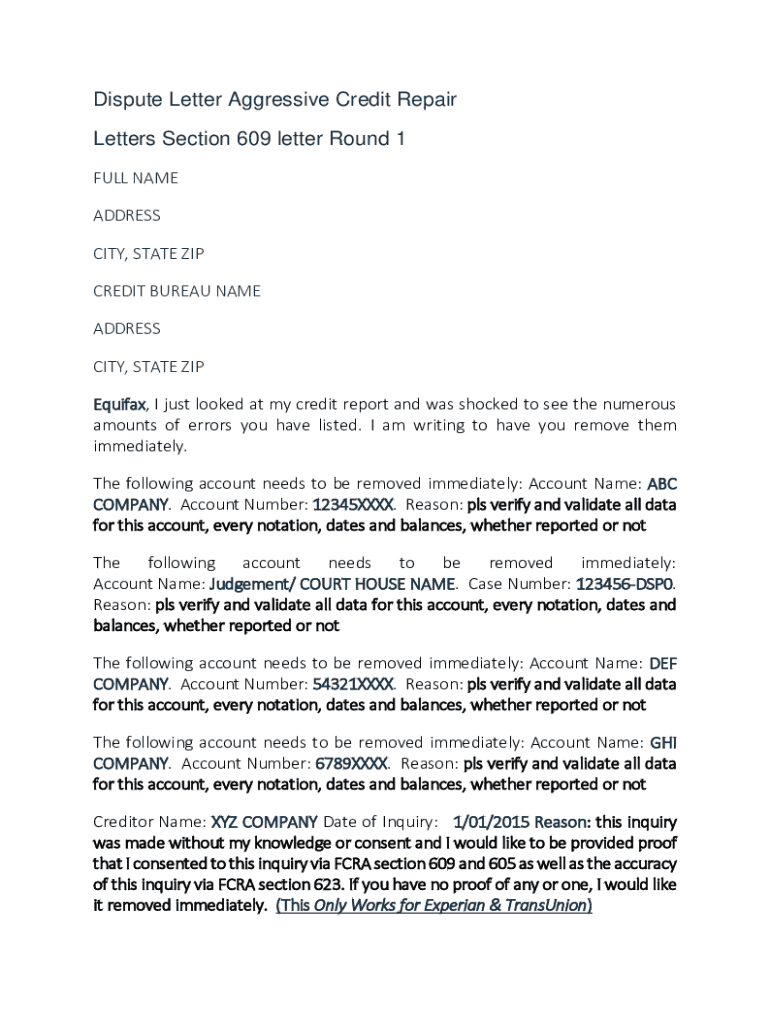

Definition and Meaning of the 609 Letter Template

The 609 letter template serves as a formal request for the removal of inaccurate or unverifiable information from a consumer’s credit report. This process is rooted in the Fair Credit Reporting Act (FCRA), which grants consumers the right to dispute any erroneous details impacting their creditworthiness. The term “609” specifically refers to the section of this act that outlines consumer rights regarding credit reports and addressing inaccuracies.

When utilizing the 609 letter, individuals can assert their right to challenge items that are either misleading or unverifiable, facilitating the process of maintaining an accurate credit history. The template typically includes personal information, details of the disputed items, and requests for documentation verifying the legitimacy of those entries.

How to Use the 609 Letter Template

Using the 609 letter template effectively requires a detailed approach. The key steps include:

-

Gather Necessary Information:

- Collect personal identification such as name, address, and Social Security number.

- Identify the inaccurate or unverifiable entries on your credit report.

-

Customize the Template:

- Insert your specific information into the 609 letter template.

- Clearly state the items you dispute and provide a brief explanation for each.

-

Send the Letter:

- Mail the letter to the appropriate credit bureau. Ensure to use certified mail for a documented trail.

- Maintain a copy of the letter for your records.

-

Wait for a Response:

- Credit bureaus are typically required to investigate disputes within 30 days. Track the response closely.

-

Review the Outcome:

- Once the investigation concludes, evaluate the outcome and take further action if necessary.

When following these steps, make sure that each element of the letter is clear and concise to facilitate the review process by the credit bureau.

Steps to Complete the 609 Letter Template

Completing a 609 letter template involves several distinct steps. Here’s a practical breakdown:

-

Identify Your Rights: Understand your rights under the FCRA and how they apply to your credit report.

-

List Disputed Items: Create a precise list of the items on your credit report that you believe require dispute.

-

Fill in Personal Information: Ensure that your name, address, and Social Security number are correctly included at the top of the letter.

-

Detail the Disputes: For each disputed item:

- Provide the account number or identifier.

- Explain why you believe the information is incorrect or unverifiable.

-

Request Documentation: Explicitly request copies of any documentation that supports the legitimacy of the reported information.

-

Include Identification: Attach copies of personal identification to verify your identity without sending original documents.

-

Send and Track: Send the letter via certified mail, if possible, and retain a receipt for tracking purposes.

Following these steps will enhance the likelihood of successfully challenging inaccurate credit entries.

Key Elements of the 609 Letter Template

The effectiveness of a 609 letter relies on specific key elements being included within its structure. These elements may include:

- Personal Information: Your full name, address, and contact details.

- Disputed Item Details: Precise information about each entry being disputed, including account numbers and creditor information.

- Reason for Dispute: A clear, concise rationale for why each entry is believed to be inaccurate or unverifiable.

- Request for Verification: An explicit request for the credit bureau to provide documentation that verifies the legitimacy of the disputed information.

- Signature: A signature line to validate that the request comes directly from you.

Incorporating these key components ensures that your 609 letter is authoritative and thorough, promoting the best chances for a favorable outcome.

Legal Use of the 609 Letter Template

The 609 letter template is designed to comply with legal guidelines set forth by the FCRA. This statute provides consumers the foundational rights necessary to dispute inaccurately reported credit entries. The legal usage of this letter involves:

- Identification as a Consumer Dispute: The letter acts as a consumer dispute request, formally signaling the intent to challenge misleading information.

- Right to Access Documentation: The FCRA grants consumers the right to request verification of the information listed in their credit reports.

- Documentation Retention: It is important to retain copies of both the letter and any correspondence received in response, as this documentation may be vital for future disputes or legal matters.

By adhering to the legal framework surrounding the 609 letter, consumers can ensure they are exercising their rights appropriately and effectively.

Examples of Using the 609 Letter Template

Practical examples can illuminate how the 609 letter template is utilized in real scenarios. Consider the following cases:

-

Example 1: A consumer notices a collection account on their credit report that they believe is due to mistaken identity. They use the 609 letter template to dispute this account, outlining their reasons and requesting supporting documentation from the credit bureau.

-

Example 2: An individual finds an erroneous late payment entry from a credit card company. By employing the 609 letter template, they clearly articulate their payment history and provide evidence of on-time payments, thereby requesting a review of this inaccurate entry.

-

Example 3: A consumer discovers a debt that has been paid off but still appears as outstanding. They draft a 609 letter to the credit bureau, including proof of payment and a request to remove the item from their report.

These examples illustrate various situations where the 609 letter template can be employed to challenge inaccuracies, ultimately supporting the consumer's right to a fair credit report.