Definition and Meaning

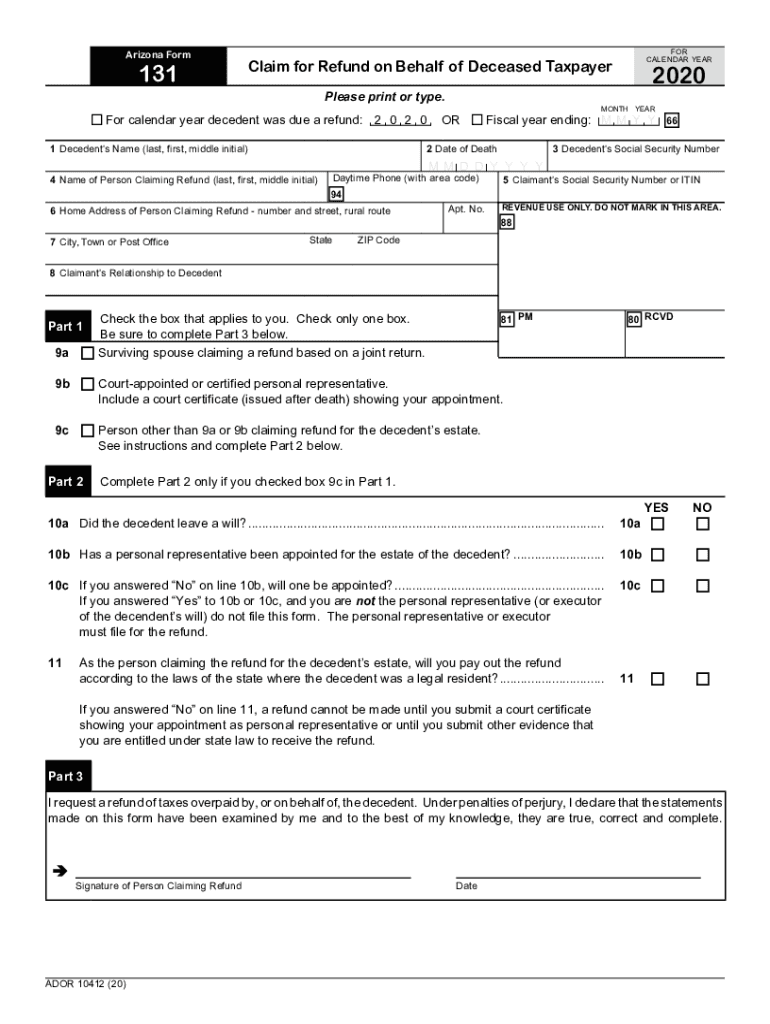

The "For calendar year decedent was due a refund: 2 0 2 0 OR Fiscal year ending: M M Y Y" form pertains to the tax filing process involved when claiming a refund on behalf of a deceased taxpayer. This form is utilized to report the tax refund due for the calendar year 2020 or for a fiscal year ending in a specified month and year (M M Y Y). It encompasses crucial details such as the identification of the decedent, the claimant, and the fiduciary's relationship to the estate. It ensures compliance with the legal procedures for refund claims related to deceased taxpayers in the United States.

How to Use the Form

Using this form requires several steps aimed at ensuring the decedent's financial obligations and entitlements are correctly managed.

- Gather Personal Information: Obtain details about the decedent, including full name, Social Security Number, and the date of death.

- Identify the Claimant: The person claiming the refund on behalf of the decedent must provide their own identifying information and show a legal relationship to the estate.

- Verify Legal Representation: Include documentation appointing a personal representative or executor of the estate if applicable.

- Determine Fiscal Year: Clearly define whether the claim refers to the calendar year 2020 or a specific fiscal year by selecting the appropriate option within the form.

- Ensure Accuracy: Confirm all information matches legal documents, especially data on the decedent's previous tax filings if available.

Steps to Complete the Form

Completing this form requires attention to detail and adherence to the prescribed instructions to avoid delays or rejection.

- Collect Documentation: Secure necessary legal documents such as death certificates and any court appointments of a personal representative.

- Fill Out Each Section: Accurately complete all required sections with the decedent's and claimant’s information.

- Declare Under Penalty of Perjury: Sign the declaration section certifying the accuracy of the information under penalty of perjury.

- Review and Attach Supporting Documentation: Attach all relevant documents, including any previous tax forms or notices from the IRS.

Important Terms Related to the Form

- Decedent: The individual who has passed away and whose tax matters the form addresses.

- Claimant: The person or entity submitting the refund request on behalf of the decedent.

- Fiduciary: A person legally required to act on behalf of the decedent’s estate.

- Fiscal Year: A one-year period companies use for accounting purposes, which does not necessarily align with the calendar year.

IRS Guidelines and Filing Deadlines

Adhering to IRS guidelines is crucial to ensure smooth processing:

- Standard Deadline: Aligns with federal tax filing deadlines, typically April 15 following the calendar year of the decedent's tax period.

- Extensions: May be available by submitting IRS Form 4868 to gain additional time for filing.

Eligibility Criteria

This form is specifically used when:

- The taxpayer has passed away, and a refund is due for their final tax year.

- There is a designated personal representative or fiduciary willing to claim the refund.

- Appropriate legal documentation substantiates the claimant's right to file on the decedent's behalf.

Required Documents for Submission

- Death Certificate: Official document verifying the decedent's death.

- Letters Testamentary or Small Estate Affidavit: If applicable, demonstrating the claimant’s right to manage the decedent’s tax matters.

- W-2s and 1099 Forms: Proof of any income earned by the decedent within the tax period concerned.

Form Submission Methods

This form can be submitted:

- Online: Through the IRS e-file system if part of a larger tax return filing.

- Mail: Conventionally, by sending a paper copy to the IRS address corresponding to the taxpayer’s state of residence.

- In-Person: By visiting a local IRS office or through an authorized tax service representative.

Penalties for Non-Compliance

Failing to accurately or timely submit the form can result in penalties, including:

- Delayed Refunds: Potential postponement of received funds.

- Legal Ramifications: In extreme cases, inaccuracies could lead to scrutiny or audits.

By understanding and implementing these guidelines and steps, individuals can effectively navigate the complexities associated with filing for a decedent's tax refund.