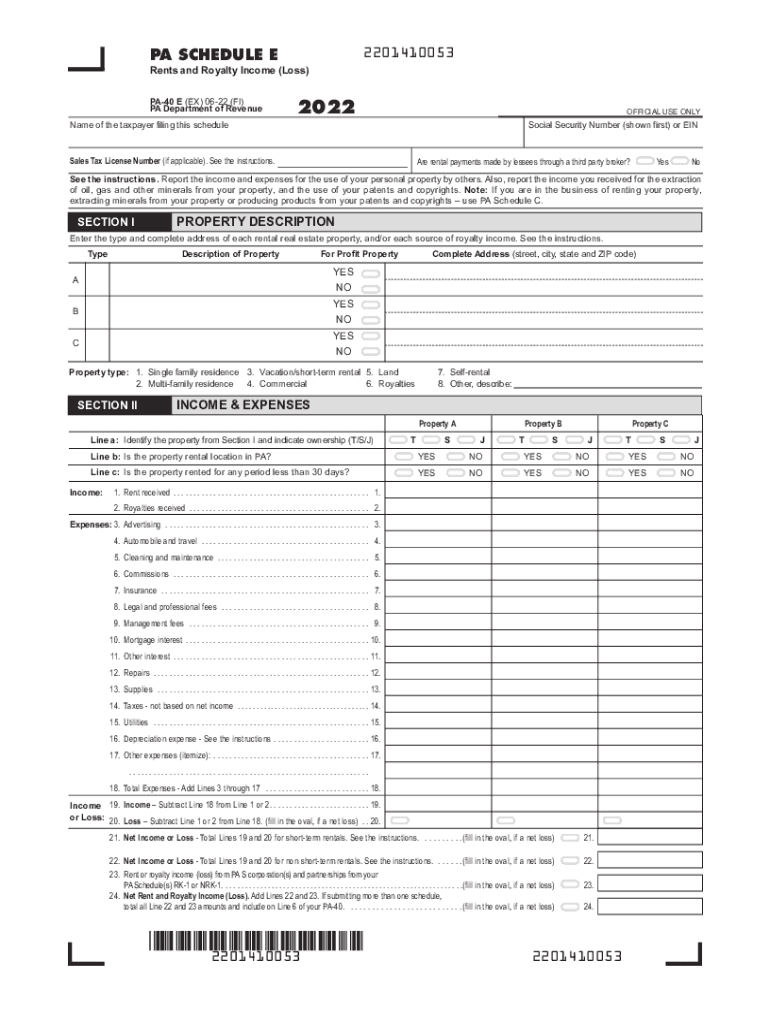

Definition and Purpose of 2022 PA Schedule E

The 2022 PA Schedule E, known as the PA-40 Schedule E for calculating rents and royalty income (loss), is a form used by individual and fiduciary taxpayers in Pennsylvania to declare their net income or loss from such activities. This form is crucial for differentiating between Pennsylvania state-specific rules and federal guidelines, especially for rental income and royalty reporting. Understanding its definition ensures taxpayers meet state requirements correctly, avoiding unnecessary errors and penalties.

How to Use the 2022 PA Schedule E

Users of the 2022 PA Schedule E can follow a clear process to appropriately complete the form. Initially, gather all relevant income and expense records associated with rental properties and royalties. The form requires taxpayers to list property descriptions, detail the type of income received, and report applicable expenses for deducing net income or loss. To guarantee compliance with Pennsylvania regulations, making sure all information aligns with the state’s tax rules is essential.

Step-by-Step Instructions

- Identify Property and Royalties: Begin by listing all rental properties and sources of royalties. Include property addresses and royalty sources for transparency.

- Catalog Income: Enter gross rental income and royalties. Be meticulous to ensure accuracy, as discrepancies may necessitate amendments.

- Report Eligible Expenses: Document allowable expenses such as repairs, insurance, and maintenance against each property. Pennsylvania may have specific guidelines, differing from federal rules.

- Calculate Net Income or Loss: Deduct total eligible expenses from total income to derive net income or loss. This figure should be accurately reported on the PA-40.

- Review and Finalize: Reassess all entries for accuracy, ensuring conformity to Pennsylvania's specific tax codes to reduce errors.

Important Terms Related to the 2022 PA Schedule E

Key Definitions

- Net Income: Earnings after deducting operating expenses from total rental and royalty income.

- Allowable Expenses: Costs like insurance, depreciation, maintenance that reduce taxable income on rental properties.

- Royalties: Payments received for the use of your property, often involving oil, gas, or mineral rights.

Understanding these terms helps ensure taxpayers correctly categorize and report their income and losses, avoiding potential compliance issues.

State-Specific Rules for Schedule E

Pennsylvania’s rules for completing Schedule E highlight significant differences from federal requirements. State-specific allowances, expense deductions, and treatment of income must be carefully followed to ensure compliance. For example, certain depreciation expenses might not align with federal rules, which can influence calculations of deductible income or assets.

Common State Variations

- Depreciation Alignments: Pennsylvania may not follow federal depreciation thresholds; instead, specific state formulas determine these calculations.

- Expense Categories: Only certain expenses may qualify for deductions. Review Pennsylvania’s tax code for definitive guidance.

Filing Deadlines & Important Dates

Timely submission of the PA-40 Schedule E is pivotal. The due date generally aligns with the federal tax filing deadline unless specific extensions are granted. Late submissions may incur penalties, so being aware of cut-off dates is essential for tax planning.

Key Dates

- Standard Deadline: Aligns with the federal tax due date, typically April 15, unless it falls on a weekend or holiday.

- Extension Filing: File for extension by the same due date, providing extra time to complete and ensure accurate submission.

Who Typically Uses the 2022 PA Schedule E

This form is aimed at Pennsylvania residents and entities receiving rental income or royalties. It applies to both individual filers and fiduciaries managing income-producing assets on behalf of another. Understanding user profiles helps ensure accurate utilization of the form.

Examples of Users

- Individual Landlords: Those owning and leasing real estate properties in Pennsylvania for additional income.

- Royalty Holders: Entities or individuals receiving payments for natural resource extractions, often from oil or gas fields.

- Trust and Estate Managers: Fiduciaries responsible for administering trust properties or estates with rental or royalty income.

Key Elements of the 2022 PA Schedule E

Comprehensive understanding of the form's layout enhances its proper completion. The Schedule E includes sections for listing properties, detailing income, reporting expenses, and calculating net income or loss. Each element requires careful attention to align accurately with Pennsylvania tax law.

Detailed Elements

- Property Identification Section: For listing each income-generating asset.

- Income Reporting Fields: Spaces designated for declaring total received income.

- Expense Columns: To record deductible expenses with corresponding documentation.

Examples of Using the PA Schedule E

Real-world applications of the 2022 PA Schedule E demonstrate its importance in tax filing processes. Consider an owner leasing residential apartments or a landowner with natural gas royalties. Both must use the form to accurately reflect their fiscal activities, adhering to state-specific guidance for compliance.

Case Scenarios

- Rental Property Owner: John owns two leased residential properties. He reports the rental income and applicable expenses, ensuring to align entries with state depreciation laws.

- Royalty Income Earners: Sarah receives royalties from gas extraction rights on her land. She must report these as income, deduct allowable expenses, and distinguish these from federal guidelines.