Definition and Meaning

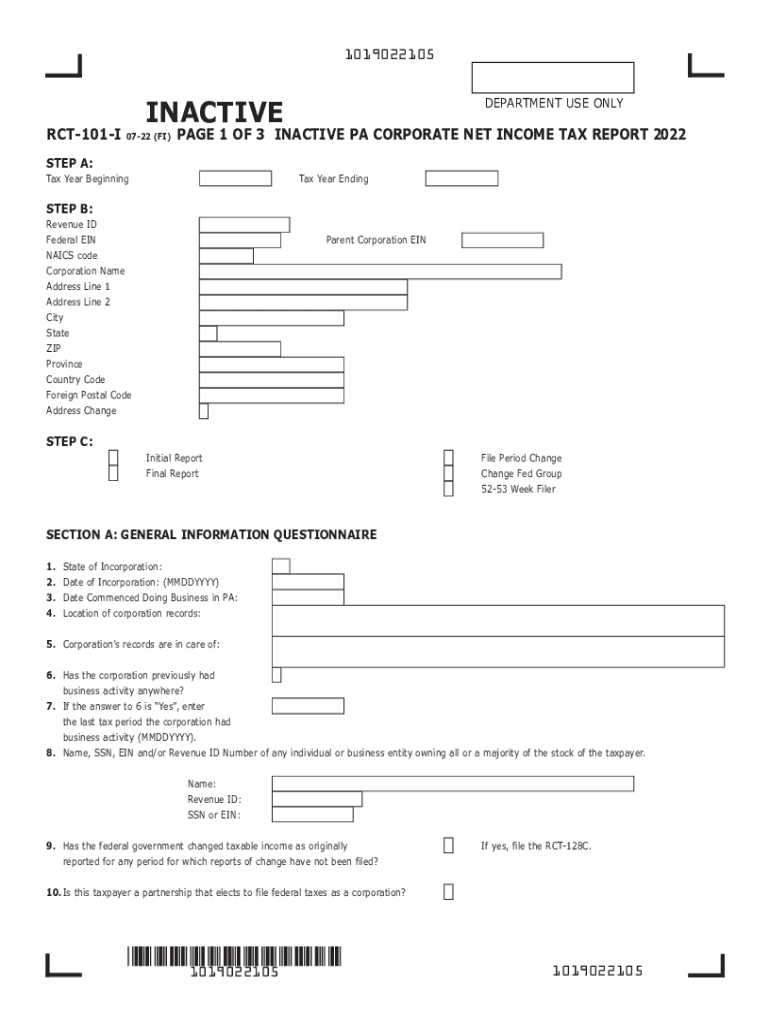

The "2022 Inactive PA Corporate Net Income Report (RCT-101-I)" refers to a specific tax form used by inactive corporations in Pennsylvania to report their net income. Inactive corporations are those that have not conducted business activities or held assets during the tax year. This form is essential for maintaining compliance with the Pennsylvania Department of Revenue and ensuring that even inactive entities fulfill their tax-reporting obligations. The distinction between inactive and active corporations is crucial as active corporations are required to file a different form, the RCT-101, due to their business activities and financial holdings.

Steps to Complete the 2022 Inactive PA Corporate Net Income Report (RCT-101-I)

-

Gather Information: Collect all relevant details about the corporation, such as its legal name, address, Employer Identification Number (EIN), and fiscal year-end.

-

Complete General Information Section: Include general information about the corporation, ensuring accuracy in details like the federal employer identification number, date of incorporation, and the reason for inactive status.

-

Fill Out the Inactive Declaration: This section requires you to declare under penalty of law that the corporation was inactive during the entire tax year. Certify that there were no sales, receipts, or income generated.

-

Document Corporate Status Changes: Report any significant changes in the corporation's status, such as mergers, changes in ownership, or dissolution plans, if applicable.

-

List Corporate Officer Details: Provide the names, titles, and contact information of the current corporate officers. This information is critical for official communication and compliance purposes.

-

Review and Sign: Ensure all sections are properly filled out, review for errors or omissions, and a corporate officer must sign the document to validate the submission.

Key Elements of the 2022 Inactive PA Corporate Net Income Report (RCT-101-I)

- General Information: Basic corporate details that establish the entity's identification.

- Inactive Declaration: A mandatory section for confirming the inactivity of the corporation.

- Status Changes: Disclosure of any alterations in corporate structure or plans.

- Corporate Officers: Current leadership information for record-keeping and accountability.

Important Terms Related to the 2022 Inactive PA Corporate Net Income Report (RCT-101-I)

- Inactive Corporation: An entity that does no business and holds no assets.

- RCT-101-I: The form designation specific to inactive corporate entities.

- PA Corporate Net Income Tax: A state tax on the net income of corporations, applicable to active entities or as a compliance form for inactive ones.

Who Typically Uses the 2022 Inactive PA Corporate Net Income Report (RCT-101-I)

Inactive corporations registered in Pennsylvania are required to use this form. These entities typically include:

- Companies that have ceased operations but remain legally recognized.

- Businesses that no longer engage in transactions or generate income.

- Corporations holding no assets within a fiscal year.

Filing Deadlines and Important Dates

- Annual Deadline: This form is typically due alongside other Pennsylvania corporate income tax filings, generally following the close of the corporation's tax year.

- Extension Requests: If an extension is necessary, the appropriate forms must be filed in advance, following the Pennsylvania Department of Revenue guidelines.

Penalties for Non-Compliance

Failure to file the RCT-101-I by the deadline can result in penalties and fines imposed by the state. Maintaining compliance helps avoid costly penalties that accumulate over time. It is important to ensure timely and accurate submissions to prevent adverse legal and financial consequences for the corporation.

Digital vs. Paper Version

Corporations have the option to file the RCT-101-I either online through the Pennsylvania Department of Revenue system or by submitting a paper version. The digital method often provides quicker processing times and instant confirmation of receipt, while the paper version may be preferred by those who favor traditional methods or lack digital access.

Required Documents

To complete the RCT-101-I effectively, gather the following:

- Legal identification documents, including corporate registration details.

- Any supporting documentation that verifies the corporation's inactive status.

- Names and responsibilities of current corporate officers to ensure accurate reporting.

Each document plays a pivotal role in verifying the information provided on the form, supporting the corporation's inactive claim, and ensuring compliance with state regulations.