Definition of the Maryland Nonresident Withholding Tax

The Maryland Nonresident Withholding Tax is a tax imposed on nonresidents who sell or transfer real property in Maryland. The primary purpose of this tax is to ensure that the state collects its fair share of taxes on income generated within its jurisdiction. This withholding is calculated based on the sale price and other transaction details to preemptively account for state tax obligations that might arise from the property sale.

Key Aspects of the Withholding Tax

- Who It Affects: The tax primarily targets nonresident individuals or entities selling real estate in Maryland. This includes corporations, partnerships, or any legal entities with no permanent establishment in the state.

- Justification: By withholding this tax at the point of sale, Maryland ensures that nonresidents fulfill their state income tax responsibilities before leaving the jurisdiction. It simplifies tax compliance for out-of-state sellers, minimizing post-sale tax complications.

How to Use the Maryland Nonresident Withholding Tax Form

Understanding how to correctly use the relevant form is crucial for nonresidents engaging in property transactions in Maryland. The primary document for this process, often known as the MD Form MW506NRS, is utilized to report and calculate the required withholding at the time of sale.

Steps for Using the Form

- Download the Form: Access the form through Maryland’s official tax website or consult with a licensed tax professional.

- Complete the Required Information: Include details such as taxpayer identification number, property address, and sale details.

- Calculate Withholding Amount: Utilize the form’s instructions to accurately determine the tax amount based on the sale price and applicable tax rates.

- Submit with Payment: Mail or electronically file the completed form along with the calculated withholding to the Maryland Comptroller’s office.

Steps to Complete the Maryland Nonresident Withholding Tax Form

Accurate completion of the Maryland Nonresident Withholding Tax form requires careful attention to detail to ensure compliance and avoid penalties. Here is a step-by-step guide:

- Gather Necessary Documents: Obtain records related to the property transaction, including the sale agreement and any related settlement documents.

- Enter Personal Details: Fill out your name, address, and taxpayer identification number at the top of the form.

- Detail Property Information: Provide specifics about the property, including address and parcel number.

- Calculate Gross Proceeds and Expenses: Use transaction details to determine the gross proceeds and any settlement expenses that may affect the withholding amount.

- Figure the Withholding Tax: Follow the percentage rates as noted in the instructions to compute the withholding required.

- Submit for Approval: After filling out the form, submit it together with the appropriate withholding payment before the property settlement date.

Eligibility Criteria for the Maryland Nonresident Withholding Tax

This tax is specifically applicable to certain individuals and entities, depending on their residency status and the nature of their property transaction in Maryland.

Who Must Pay

- Nonresident Individuals and Entities: Any sellers or transferors of real property in Maryland who do not qualify as state residents.

- Foreign Entities: Corporations or partnerships with no fixed business presence in Maryland.

Exemptions and Special Circumstances

- Residents Selling Principal Residence: May qualify for exemptions if the sale involves their primary residence.

- Installment Sales: Specific rules apply, potentially affecting the initial withholding requirement.

Filing Deadlines and Important Dates

Compliance with deadlines is critical to avoid interest charges or penalties associated with late payments.

Key Dates

- Submission Deadline: The completed form and payment should be submitted before or on the date of the property settlement.

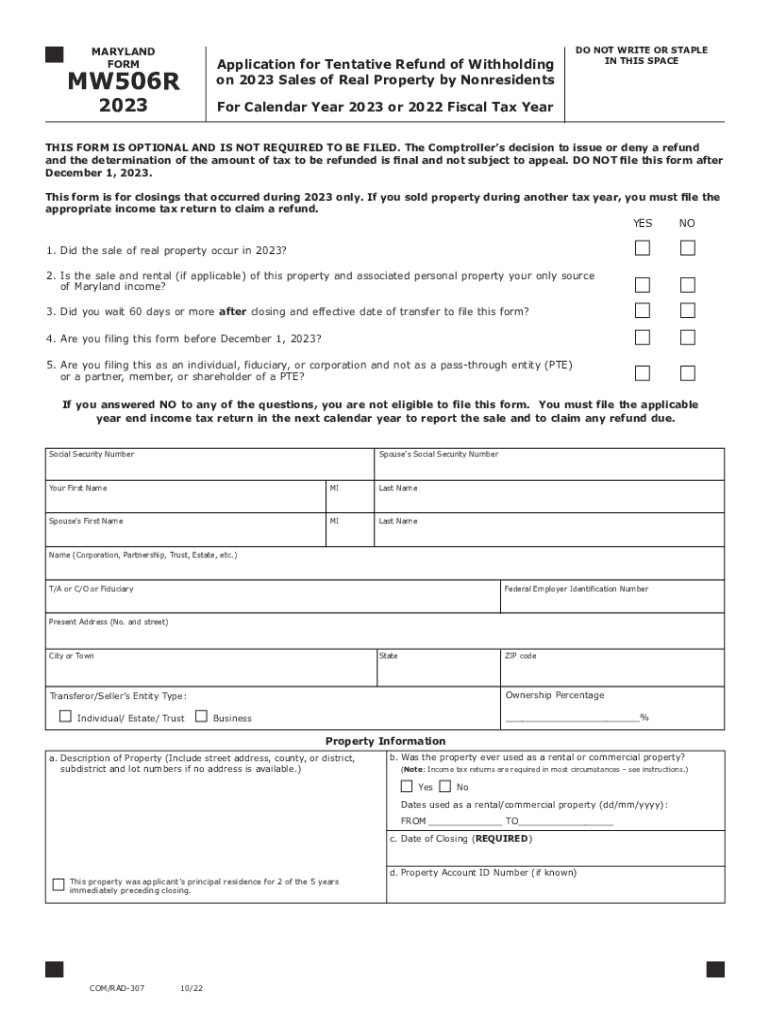

- Refund Application (Form MW506R): For those eligible, applications for a tentative refund of excess withholding should be filed by December 1, 2023.

Consequences of Late Filing

Failure to submit the form and payment on time could result in additional penalties and interest imposed by the state of Maryland.

Examples of Nonresident Withholding Tax Applications

Real-world scenarios illustrate the practical application of this tax in various contexts, offering clarity to potential taxpayers.

Example Scenarios

- Sale by a Nonresident Individual: John, a nonresident of Maryland, sells a vacation home and must withhold 7.5% of the total sales price as state tax.

- Foreign Corporation Selling Property: XYZ Corp, headquartered in another state, sells commercial property in Maryland and must calculate the relevant withholding based on corporate tax rates.

Legal Use and Restrictions of the Form

Legal considerations and restrictions guide the accurate application of the Maryland Nonresident Withholding Tax and ensure that taxpayers meet all regulatory requirements.

Legal Compliance

- Form Integrity: It is crucial to provide accurate and truthful information, as any misrepresentation can lead to legal consequences.

- Double-check Before Submission: Reviewing the form for completeness and accuracy minimizes the risk of noncompliance.

Penalties for Non-Compliance

Failure to adhere to the Maryland Nonresident Withholding Tax requirements can result in severe financial repercussions and legal issues.

Types of Penalties

- Late Payment Penalties: These can amplify over time if the withholding is not remitted by the due date.

- Interest on Unpaid Taxes: Interest is calculated from the transaction date on any unpaid withholding tax.

Avoiding Penalties

- Ensure timely submission and remittance of taxes using accurate calculations.

- Seek professional guidance if uncertain about any aspect of the form or process.