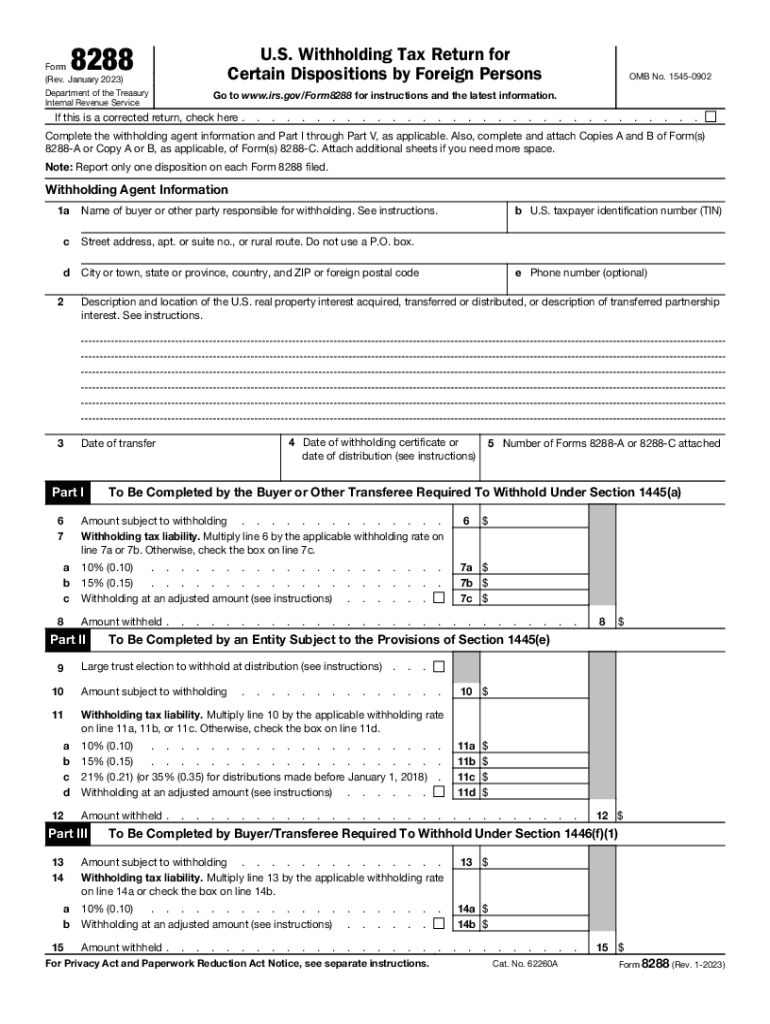

Definition and Purpose of IRS Form 8288

IRS Form 8288, known as the U.S. Withholding Tax Return for Dispositions by Foreign Persons, is used to report the withholding tax obligation for the disposal of U.S. real property interests by foreign persons or entities. This form is crucial in ensuring compliance with the requirements under the Foreign Investment in Real Property Tax Act (FIRPTA). The form primarily documents the details of the property disposition and the associated withholding taxes that the transferee is obligated to withhold and remit to the IRS.

Importance of FIRPTA Compliance

FIRPTA mandates that the buyer of a U.S. real estate interest from a foreign person must withhold tax to ensure that the IRS receives tax dues related to the transaction. IRS Form 8288 facilitates this by providing a structured means to report and remit those amounts. Compliance is vital as non-compliance can lead to significant penal actions.

Who Should Use IRS Form 8288

The form is typically used by buyers, transferees, or agents involved in the acquisition of U.S. real estate interests from foreign sellers. It is not filed by the foreign transferor but rather by the person responsible for withholding the tax, often the buyer or their agent, who ensures the IRS receives the applicable tax. This responsibility underscores the importance of understanding one's role in the transaction to avoid compliance issues.

Responsibilities of Withholding Agents

The withholding agent must calculate the appropriate withholding amount—typically fifteen percent of the sales price—and ensure timely submission to the IRS. They must accurately complete Form 8288, covering details like the transferee’s information, property details, and calculations of the withholding tax.

Filing Deadlines and Important Dates

Form 8288 must be submitted to the IRS within twenty days of the date of the transfer of property. This tight timeline requires prompt action following the transaction. Filing deadlines are critical, as missing them could result in penalties and interests charges accruing on the taxes that should originally have been withheld.

Considerations for Timely Filing

To adhere to these timelines, it is advisable that withholding agents prepare documents in advance, where foreseeable, and maintain an organized checklist to gather the required information promptly.

Key Elements of IRS Form 8288

Form 8288 consists of several sections that must be completed with accuracy. These include:

- Transferee Information: Includes the name, address, and identification numbers of the buyer or withholding agent.

- Transferor Information: Captures details about the foreign seller, such as nationality and identification numbers.

- Property Description: Concerns details about the real estate being transferred, such as address or legal description.

- Withholding Calculations: Involves computing the correct withholding amount based on the total sales price or portion allocable to the foreign seller.

Steps to Complete Form 8288

- Gather Information: Collect details about the parties involved and the property.

- Fill Out Identification Sections: Enter the relevant details for both transferee and transferor.

- Describe the Property: Accurately provide property details to avoid any discrepancies.

- Calculate Withholding: Use the applicable rate to determine the withholding amount.

- Review and Submit: Carefully review the form for accuracy before submitting to the IRS.

Edge Cases and Exceptions

Certain exceptions allow for reduced withholding, such as obtaining a withholding certificate or small amount transactions—care should be taken to explore these possibilities when applicable.

Alternatives to IRS Form 8288

While IRS Form 8288 is specific to certain transactions under FIRPTA, alternative forms or certificates may apply if exemptions or reductions from withholding tax are requested or approved. Understanding these alternatives ensures compliance with IRS requirements while potentially benefiting from reduced tax withholding.

Withholding Certificates

To qualify for reduced withholding, apply for a withholding certificate through IRS Form 8288-B. This process involves proving that a reduced tax obligation is appropriate for the transaction.

Penalties for Non-Compliance

Failure to file IRS Form 8288 or to remit the proper withholding amount can result in severe penalties, including fines and interest charges on the unremitted taxes. The IRS holds the withholding agent accountable, thus highlighting the importance of compliance with all FIRPTA requirements to avoid financial and legal repercussions.

Mitigation Strategies

For any potential compliance issues, seeking advice from a tax professional or legal advisor can mitigate risks and ensure accurate and timely fulfillment of obligations when using IRS Form 8288.