Definition and Meaning

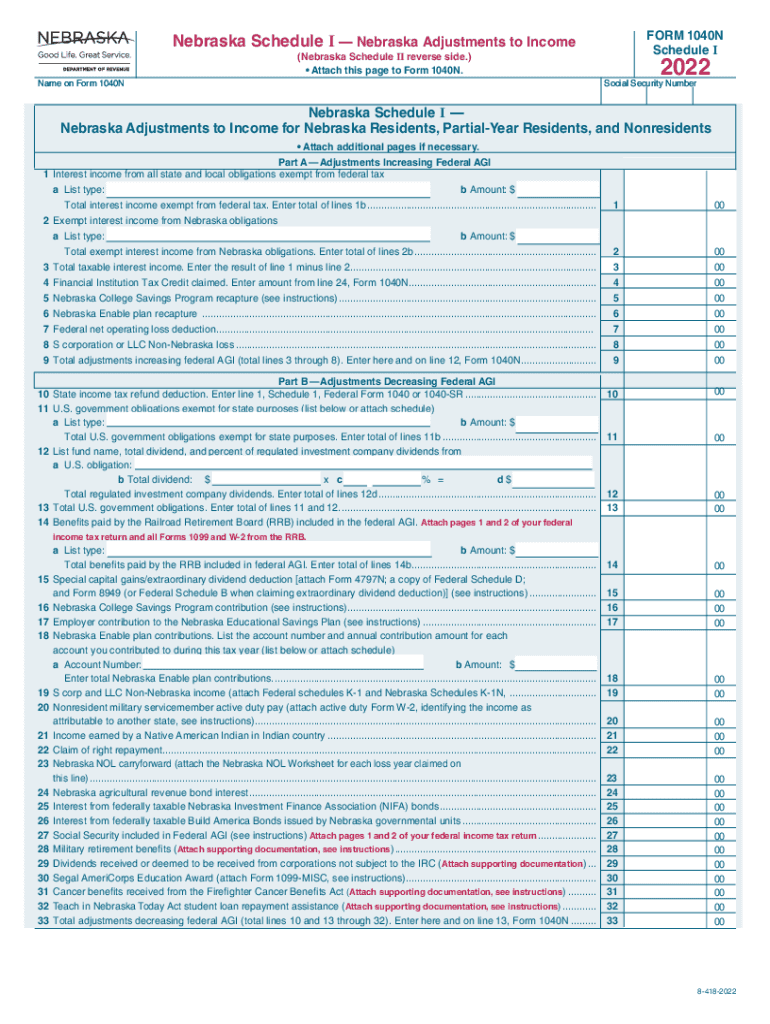

Nebraska Schedule I, part of the state’s tax forms, specifically addresses adjustments to income reported on Form 1040N for residents, partial-year residents, and nonresidents in Nebraska. These adjustments play a crucial role in accurately determining state tax liabilities, ensuring that income reported to the federal government is correctly adjusted to reflect Nebraska-specific tax rules. By understanding these adjustments, taxpayers can identify opportunities for deductions or credits that may reduce their overall tax burden at the state level.

How to Use Nebraska Schedule I Adjustments to Income

Nebraska Schedule I is used primarily by individuals who need to adjust their federal adjusted gross income (AGI) for state tax purposes. The form captures specific modifications that Nebraska law requires to be made to the federal AGI to comply with state tax regulations. To use the form:

- Identify applicable income adjustments based on residency status.

- Gather documentation supporting adjustments, such as receipts or financial statements.

- Accurately input adjustments, ensuring alignment with Nebraska tax laws.

Nebraska Schedule I assists in calculating the correct taxable income necessary for completing Form 1040N and determines if additional tax is owed or if a refund is due.

Steps to Complete Nebraska Schedule I

Completing Nebraska Schedule I involves a series of methodical steps to ensure accurate reporting:

- Review Residency Status: Determine whether you are a resident, partial-year resident, or nonresident, as this affects how adjustments are applied.

- List Adjustments: Identify all federal adjustments that require modification according to state rules.

- Input Adjustments: Carefully enter each adjustment in the appropriate sections, paying particular attention to the nature of the income and the reason for the adjustment.

- Calculate: Compute the Nebraska-specific adjustments to produce the state-adjusted gross income.

- Verify: Cross-check all entries for accuracy before finalizing the schedule.

Following these steps helps avoid discrepancies and potential penalties.

Important Terms Related to Schedule I Adjustments

Understanding key terminologies associated with Schedule I is vital for proper form completion:

- Adjusted Gross Income (AGI): The federal AGI that requires adjustment for state-specific rules.

- Residency Status: Classification as a resident, partial-year resident, or nonresident affecting which adjustments apply.

- Deductible Contributions: Specific charitable or investment contributions allowed under Nebraska rules but not deductible federally.

- Federal Adjustments: Base adjustments established under federal tax law, subject to modification for Nebraska purposes.

Familiarity with these terms ensures that taxpayers can accurately navigate the nuances of the form.

Key Elements of Nebraska Schedule I

Nebraska Schedule I comprises essential elements that must be carefully considered:

- Income Modifications: Includes state-specific additions and subtractions from federal AGI, such as state incentives or nondeductible federal adjustments.

- Documentation Requirements: Submission necessitates supporting documentation for each adjustment claimed.

- Statutory Guidelines: Legislative rules governing the allowable modifications to income.

Each element plays a pivotal role in ensuring compliance and accuracy, underpinning the broader tax filing process.

IRS Guidelines and Their Relation to Nebraska Schedule I

While Nebraska Schedule I specifically caters to state tax filings, understanding IRS guidelines is imperative:

- Federal and State Differences: IRS rules set the baseline AGI, but Nebraska modifies it via Schedule I.

- Consistency in Filing: Align federal and state filings to avoid discrepancies, leveraging IRS guidelines as a reference for calculating initial figures before adjustments.

- Legislative Updates: Stay informed on any IRS changes that might impact Nebraska adjustments to maintain compliance.

The relationship between federal guidelines and Nebraska Schedule I is integral to accurate tax reporting.

Required Documents for Completing Schedule I

A successful Schedule I filing requires specific documentation:

- Federal Tax Return: Especially key sections detailing AGI.

- Income Sources: Documentation including W-2s, 1099s, and other income statements.

- Adjustment Justifications: Receipts or proof of deductible events, such as charitable contributions or educational expenses.

Ensuring these documents are accessible streamlines the completion process and substantiates claimed adjustments.

Filing Deadlines and Important Dates

Critical dates to remember when handling Nebraska Schedule I:

- Tax Filing Due Date: Aligns with federal deadlines, typically April 15, ensuring complete submissions.

- Extension Requests: If required, file for extensions following both federal and state procedures prior to the original deadline.

- Amendment Periods: Deadlines for modifications to filed returns may vary; typically within three years of the original filing.

Awareness and adherence to these timelines are essential to maintain compliance and avoid late penalties.

Examples of Using Nebraska Schedule I Adjustments

Practical use cases illustrate how Nebraska Schedule I adjustments impact tax situations:

- Educational Deductions: Tuition paid to Nebraska educational institutions might be added to reduce taxable income.

- Incentive Programs: Participation in state-specific incentive programs, such as renewable energy credits, potentially adjusts income.

- Multiple Income Streams: Adjustments for diverse income sources like farming or freelance work compare federal and state regulations.

These examples highlight the form's application, helping taxpayers leverage adjustments for optimal tax outcomes.