Definition and Meaning of Schedule A (Form 8804)

Schedule A (Form 8804) pertains to the calculation of penalties for the underpayment of estimated Section 1446 tax by partnerships. It is instrumental for partnerships in reporting obligations to the Internal Revenue Service (IRS) concerning any discrepancies in estimated tax payments, specifically targeting foreign partner income allocations. This form ensures that the partnership complies with tax regulations regarding withheld income effectively connected to U.S. trade or business activities.

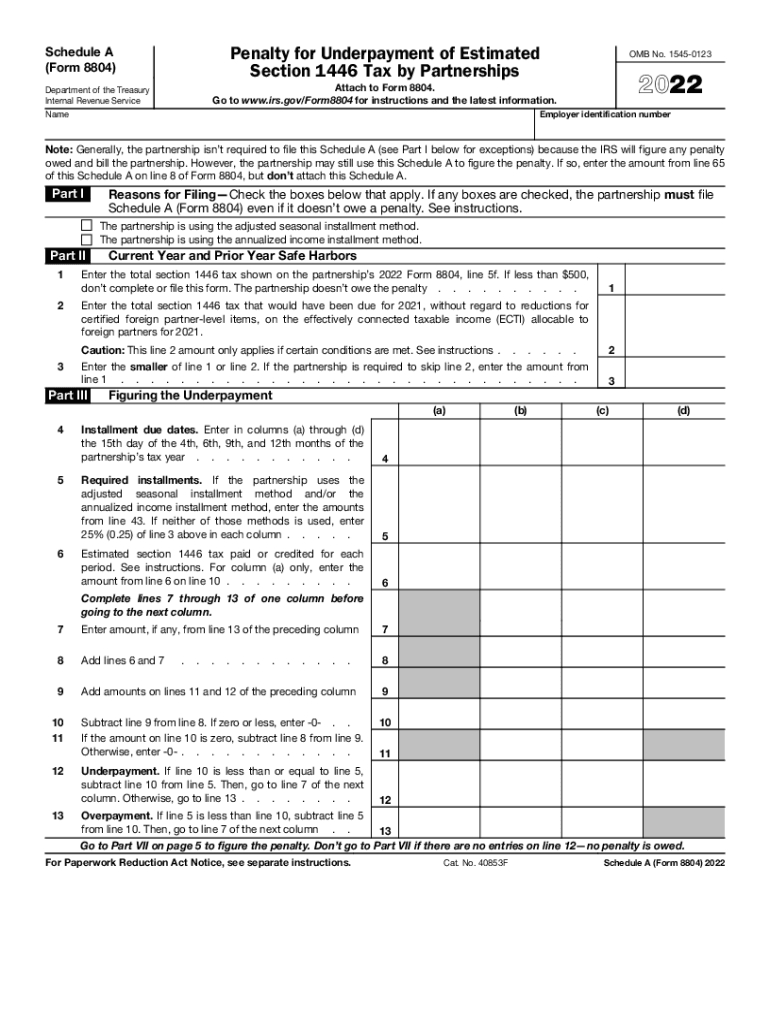

How to Use Schedule A (Form 8804)

- Determine Tax Amounts: Calculate the total estimated Section 1446 tax payments required for foreign partners' effectively connected income.

- Enter Installment Data: Record the amounts relevant to quarterly installments for the fiscal year.

- Calculate Underpayment: Identify any discrepancies between estimated taxes and actual payments.

- Determine Penalty: Utilize IRS guidelines within the form to establish penalties based on underpayment amounts.

This process allows partnerships to account for the fiscal responsibilities tied to foreign partner income and aligns with the IRS's regulatory framework for federal tax calculations.

Obtaining Schedule A (Form 8804)

Partnerships can acquire Schedule A (Form 8804) directly from the IRS website, ensuring they use the official form version for the relevant tax year. This document is available for download in PDF format, with the convenience of accessing it online eliminating mailing delays. Adaptations for digital completion are supported by compatible tax filing software, facilitating seamless integration into electronic tax submission processes.

Steps to Complete the Form

- Enter Partnership Details: Start by filling in basic information such as the partnership's name, tax year, and EIN.

- Calculate Estimated Payments: Provide comprehensive details for all payment periods throughout the year.

- Assess Underpayment Risks: Analyze prior installment payments and estimate potential underpayment.

- Compute Penalties: Follow IRS-provided tables and instructions to decide potential penalties for underpaid amounts.

These steps ensure accurate and timely completion of tax obligations associated with Section 1446.

Importance of Filing Schedule A (Form 8804)

Filing Schedule A (Form 8804) is crucial to avoid costly penalties associated with underpayment of taxes on foreign partners' income. It represents compliance with federal tax regulations, preserving the partnership's standing with legal tax obligations and minimizing financial risks. This vigilance during submissions streamlines IRS interactions, reducing post-filing queries or adjustments.

Key Elements of the Form

- Foreign Partner Tax Details: Involves calculations involving foreign partner income effectively connected with U.S. business operations.

- Installment Payments: Specific focus on quarterly installment due dates and associated amounts.

- Penalty Assessments: Dedicated sections for determining precise underpayment penalties according to IRS guidelines.

These components highlight critical compliance areas for partnerships in the context of international income provisions.

Filing Deadlines and Important Dates

It is mandatory for partnerships to stay informed of key filing dates to prevent penalties and interest charges. Typically, installment payments align with quarterly IRS tax payment deadlines. However, specific due dates may vary annually, stressing the importance of checking IRS announcements for any changes or special considerations relevant to the filing year.

Penalties for Non-Compliance

Failure to accurately complete and submit Schedule A (Form 8804) can result in significant penalties, primarily associated with underpayment of Section 1446 taxes. Penalties generally comprise a percentage of unpaid tax amounts, compounded with interest penalties where applicable. Timely and precise filing preserves financial health and legal compliance for partnerships.

IRS Guidelines

The IRS provides notable guidelines and clarifications for filling out Schedule A (Form 8804), including detailed penalty calculation methods and examples. These guidelines are integral to understanding obligations under Section 1446 and are available on the IRS website or through their comprehensive annual tax filing instructions.

Taxpayer Scenarios and Relevant Examples

Partnerships engaged with foreign partners must address scenarios like varying income levels and different types of U.S.-sourced income. Examples include:

- Income Variance: Calculating underpayment for partners with fluctuating quarterly revenue streams.

- Income Source Differentiation: Determining penalties based on distinct streams, such as passive income versus active business conduct.

These examples depict practical applications and ensure proficient utilization of Schedule A (Form 8804) for tax compliance.