Definition & Meaning

Form 1094-C is an IRS transmittal form used by Applicable Large Employers (ALEs) in the United States to report health insurance offer and coverage information for employees. ALEs are defined as employers with 50 or more full-time equivalent employees. The form serves as a summary of the employer’s health insurance offerings and must be filed alongside each employee's Form 1095-C. This form includes information such as the employer's identification, contact details, and the certification of eligibility for various IRS relief methods.

How to Use the 2016 Form 1094-C

Employers use the 2016 Form 1094-C to report their compliance status under the Affordable Care Act (ACA). This involves documenting the health coverage offered to employees throughout the year. Employers fill out this form to indicate whether the organization meets ACA requirements for offering insurance, including details about the coverage provided and the number of full-time employees. The form is integral for confirming whether an employer potentially owes a Shared Responsibility Payment for not offering adequate health coverage.

Key Elements of the 2016 Form 1094-C

The 2016 Form 1094-C comprises several critical sections:

-

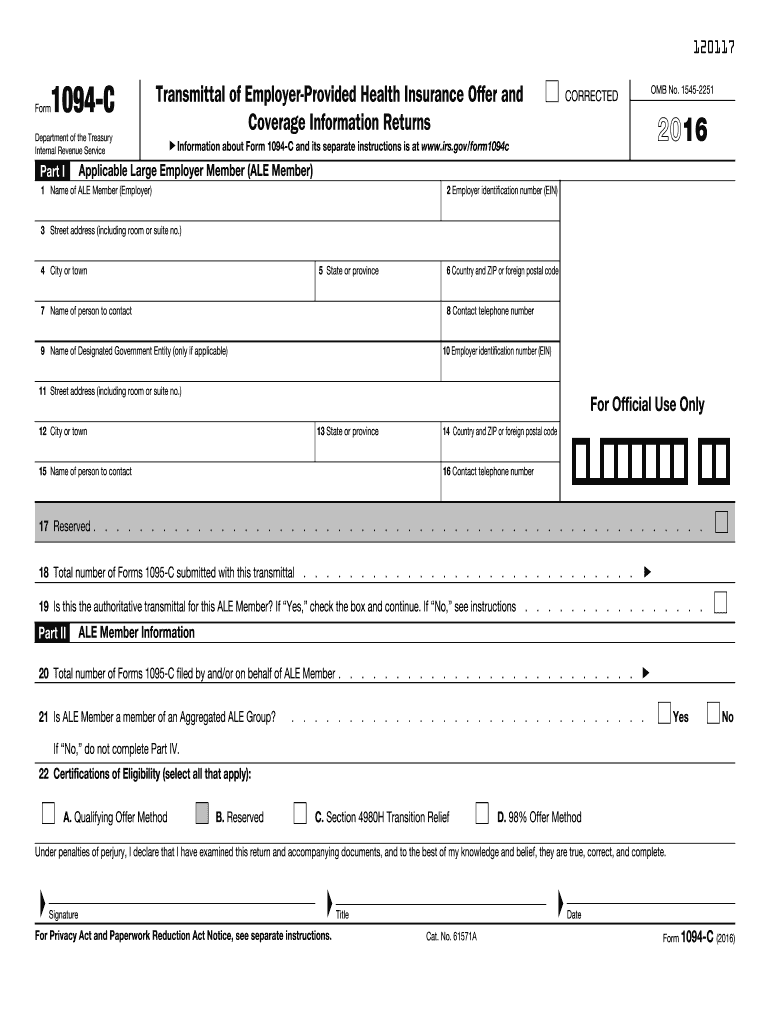

Part I: Employer Information

This section captures the basic identification details of the employer, including name, EIN, and contact information. -

Part II: ALE Member Information

Employers detail whether they offered health insurance coverage to at least 95% of their full-time employees and their dependents. -

Part III: Certification of Eligibility

This part includes certifications of eligibility for any transition relief or exceptions applicable under ACA for the reporting year. -

Part IV: Aggregated ALE Group Members

Employers belonging to a group of companies report information for each entity within that group.

Steps to Complete the 2016 Form 1094-C

-

Gather Employer Information: Collect all necessary details, like employer name, EIN, and contact information.

-

Determine ALE Status: Verify whether the company qualifies as an ALE by reviewing employee count and structure during the year.

-

Complete Part I of the Form: Fill in basic employer information accurately.

-

Document Coverage Offers: Provide details in Part II about the percentage of full-time employees offered healthcare coverage.

-

Indicate Certifications in Part III: Include any certifications of eligibility for IRS transition relief that applied.

-

Submit by Filing Deadline: Ensure the form is filed by the IRS deadlines to avoid penalties.

Why Should You Use Form 1094-C?

Using Form 1094-C is a statutory requirement for ALEs to comply with the ACA. It confirms the employer's commitment to providing health coverage and helps avoid potential penalties. Compliance demonstration through Form 1094-C is crucial for maintaining eligibility for transition relief and ensuring accurate health coverage information is sent to the IRS.

Legal Use of the 2016 Form 1094-C

Form 1094-C is used legally to demonstrate ALEs' efforts to comply with health coverage provisions under the ACA. This documentation is essential for the IRS to determine if an employer meets ACA requirements and whether they owe any Shared Responsibility Payments. Incorrect or fraudulent reporting on this form can lead to significant legal repercussions, including penalties and audits.

IRS Guidelines & Filing Deadlines

The IRS offers detailed instructions for completing and filing Form 1094-C. Employers must submit the form alongside any required employee Form 1095-Cs. The deadline for filing with the IRS is generally by March 31 for electronic submissions, or the previous month's end for paper filings.

Penalties for Non-Compliance

Failure to accurately complete or submit the 2016 Form 1094-C can result in significant IRS penalties. Non-compliance may involve fines for late filing, incorrect information, or failure to issue forms to employees. Employers are encouraged to review IRS guidelines thoroughly to avoid these fines and maintain compliance with ACA regulations.

Digital vs. Paper Version

When filing Form 1094-C, ALEs have the choice to submit either electronically or as a paper form. Electronic filing is recommended for larger employers due to efficiency and the IRS’s push towards digital submissions for accuracy and logistical reasons. Paper filing remains an option but may involve higher error risk due to manual processing steps.

These sections comprehensively cover essential aspects of the 2016 Form 1094-C, offering detailed guidance for employers regarding its use, completion, and submission.