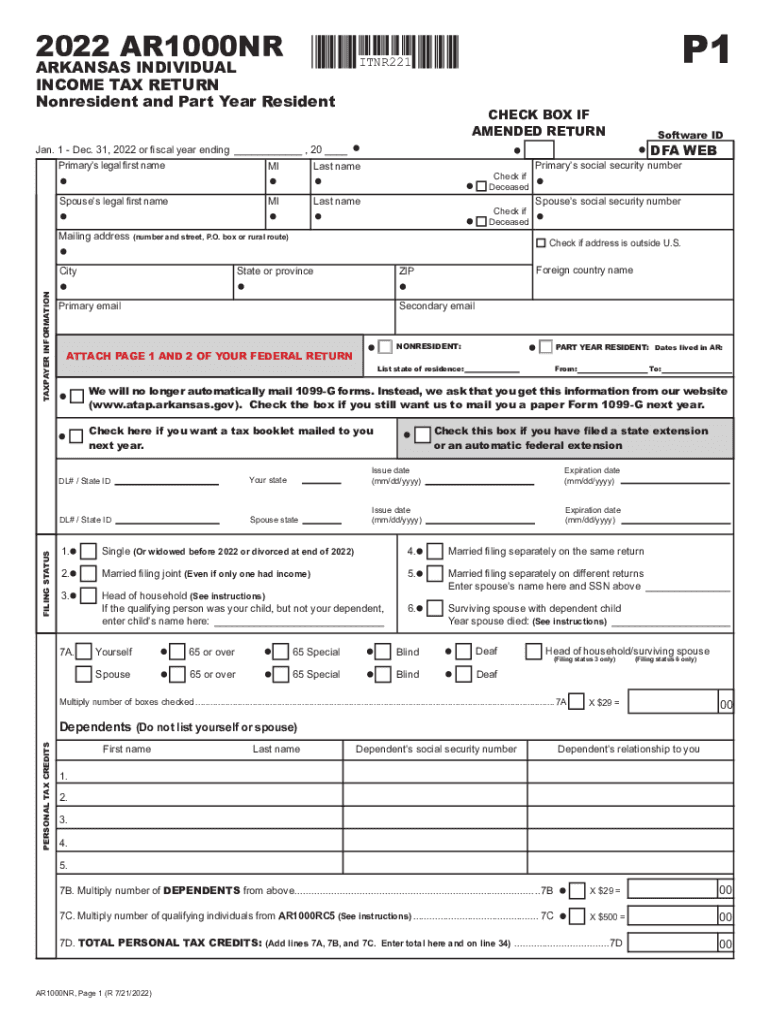

Definition and Meaning of Income Tax Return

An income tax return is a document filed with the Internal Revenue Service (IRS) and, in some cases, with state or local tax agencies, detailing an individual's income, expenses, and other tax-related information. The primary purpose of this form is to calculate the amount of tax owed or the refund due to the taxpayer. It reflects the financial activities over a fiscal year, allowing taxpayers to report earnings from various sources such as employment, investments, and business operations. Accurate reporting is crucial as it determines the correct tax liability and ensures compliance with U.S. tax laws.

How to Use the Income Tax Return

Using the income tax return involves several steps, starting with gathering all necessary financial records. Taxpayers must accurately declare their total income and identify any deductions and credits they are eligible for. The form typically includes sections for personal information, filing status, income declared, tax credits, deductions, and the final tax calculation. It is essential to follow the instructions provided with the form, as errors can lead to penalties or delayed refunds. Consider consulting with a tax professional if your financial situation is complex or using tax software to streamline the process.

Steps to Complete the Income Tax Return

- Gather Documents: Collect W-2s, 1099s, and records of other income sources.

- Choose Filing Status: Select the appropriate filing status, such as single, married filing jointly, or head of household.

- Calculate Income: Report all sources of income as required, including wages and interest income.

- Determine Deductions and Credits: Identify applicable deductions like student loan interest and credits such as earned income credit.

- Fill Out the Form: Complete each section of the form with accurate information.

- Review: Check for accuracy to avoid rejections or amendments.

- Submit: File the form via the IRS e-file system, through mail, or using tax software.

IRS Guidelines and Important Terms

Understanding IRS guidelines is critical for filing an accurate income tax return. Common terms include:

- Adjusted Gross Income (AGI): Total income minus specific deductions.

- Taxable Income: Income subject to tax after deductions.

- Tax Credits: Amounts that directly reduce tax liability.

- Deductions: Expenses that reduce taxable income.

- Withholding: Taxes withheld from wages to prepay tax liability.

Filing Deadlines and Important Dates

The standard deadline for filing a federal income tax return is April 15th of the following year. If this date falls on a weekend or legal holiday, it is extended to the next working day. Taxpayers can request an extension to October 15th, giving them extra time to prepare. However, an extension to file is not an extension to pay; taxes owed are still due by the original deadline to avoid interest and penalties.

Required Documents for Filing

When filing an income tax return, ensure you have the following documents:

- W-2 Forms: Issued by employers to report earnings and taxes withheld.

- 1099 Forms: Reporting other income like self-employment, interest, and dividends.

- Receipts: For deductions such as business expenses or charitable contributions.

- Identity Documents: Such as a Social Security number or Individual Taxpayer Identification Number (ITIN).

Form Submission Methods

Taxpayers can choose from several methods to submit their income tax return:

- Online: Using IRS e-file, an authorized e-filing service, or tax software.

- By Mail: Sending paper returns to the appropriate IRS address based on location.

- In-Person: Some IRS offices accept hand-delivered forms, though this option is less common.

Penalties for Non-Compliance

Failing to file a tax return or pay taxes owed by the deadline can result in penalties and interest. The IRS may impose a failure-to-file penalty, generally 5% of the unpaid tax for each month the return is late, up to a maximum of 25%. Additionally, a failure-to-pay penalty of 0.5% per month applies to taxes not paid by the deadline. To avoid these, taxpayers should file on time and pay any taxes owed, even if they cannot pay the full amount, to reduce penalties.

Digital vs. Paper Versions of the Income Tax Return

Taxpayers have the option to file either digital or paper versions of their income tax return. Online filing is generally faster, as it reduces errors, ensures immediate confirmation of receipt, and speeds up the refund process. In contrast, paper filing may take longer due to manual processing, although some individuals prefer it for record-keeping or complexity reasons. Regardless of the method, both versions require precise and thorough completion to ensure compliance with tax laws.