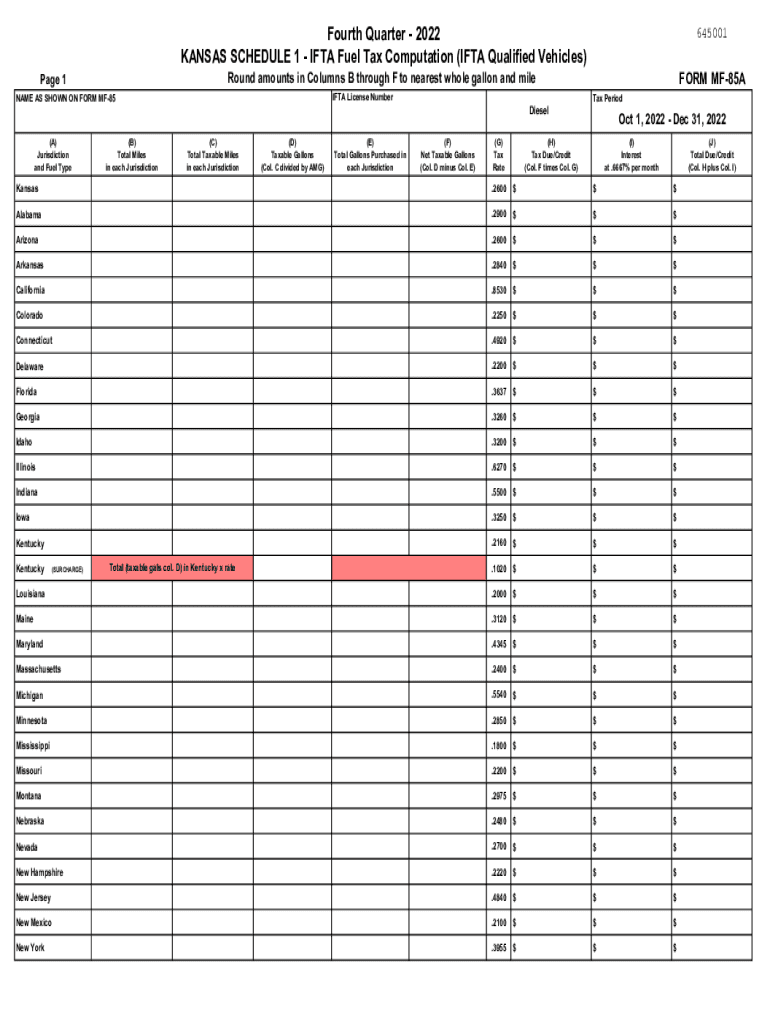

Definition & Meaning

The IFTA Inc 4thq2022 Gasoline - Kansas Department of Revenue form is a fuel tax computation document used by qualified motor carriers operating across multiple jurisdictions. This form, often referred to as IFTA Schedule 1, is essential for calculating fuel taxes for each jurisdiction in which the carrier operates. The main components of the form include total miles driven, taxable miles, gasoline gallons purchased, net taxable gallons, applicable tax rates, and the total tax due or credit for each jurisdiction.

Steps to Complete the IFTA Inc 4thq2022 Form

To accurately complete the IFTA Inc 4thq2022 Gasoline form:

-

Collect Necessary Data: Gather all travel and fuel purchase records for the fourth quarter of 2022. This includes total miles driven and gallons of gasoline purchased in each jurisdiction.

-

Calculate Total Miles: Record the total distance traveled by the fleet. This figure is crucial for determining taxable miles.

-

Determine Taxable Miles: Subtract any non-taxable miles (such as exempt miles under specific jurisdiction regulations) from the total miles.

-

Input Gallons Purchased: Enter the total gallons of gasoline purchased in each jurisdiction.

-

Compute Net Taxable Gallons: Use the formula: [Total gallons purchased - Taxable gallons] for each jurisdiction.

-

Apply Tax Rates: Input the jurisdiction-specific tax rates to calculate the taxes due or any credit owed.

-

Review and Finalize the Form: Double-check all entries and calculations for accuracy before submission.

Key Elements of the Form

The IFTA Inc 4thq2022 Gasoline form includes several critical elements that need careful attention:

- Jurisdiction: Each section in the form corresponds to a specific jurisdiction where operations occurred.

- Total Miles vs. Taxable Miles: Distinguishing between these metrics is essential for correct tax computation.

- Fuel Purchases: Accurate records of fuel purchases are crucial for determining net taxable gallons.

- Tax Rates: These vary by jurisdiction and significantly impact the total tax due.

Legal Use of the IFTA Inc 4thq2022 Form

Utilizing the IFTA Inc 4thq2022 Gasoline form comes with legal obligations:

- Compliance: Filing this form ensures compliance with the International Fuel Tax Agreement (IFTA) requirements.

- Record Keeping: Maintain accurate records for auditing purposes.

- Deadlines: Adherence to submission deadlines is imperative to avoid penalties.

Important Terms Related to the IFTA Inc 4thq2022 Form

Understanding key terms is crucial for accurate form completion:

- Qualified Vehicles: Typically encompasses vehicles that are used for interstate commerce and have a gross vehicle weight exceeding 26,000 pounds.

- Jurisdiction: Refers to a member state or Canadian province under IFTA.

- Taxable Miles: Miles traveled liable for fuel taxes in a jurisdiction.

- Net Taxable Gallons: The adjusted quantity of gallons subject to fuel tax after accounting for purchases and usage.

Filing Deadlines and Important Dates

For the IFTA Inc 4thq2022 Gasoline form, the filing deadlines are:

- Fourth Quarter Deadline: Generally due by January 31st of the following year.

- Grace Periods and Extensions: Check specific jurisdiction policies for grace periods or options for filing extensions.

Penalties for Non-Compliance

Failing to submit the IFTA Inc 4thq2022 form by the deadline can lead to:

- Monetary Fines: Penalties are often a percentage of the taxes owed.

- Interest Charges: Additional interest may accrue on unpaid taxes.

- Revocation of IFTA License: Non-compliance can lead to suspension of your ability to operate interstate.

State-Specific Rules for the IFTA Inc 4thq2022 Form

Although the IFTA framework aims for consistency, variations exist:

- Specific Exemptions: States may offer exemptions for particular types of travel, such as government vehicles or certain agricultural equipment.

- Tax Rate Differences: Tax rates vary significantly from state to state and can impact total liability.

Examples of Using the IFTA Inc 4thq2022 Form

Consider these examples:

-

Scenario 1: A Kansas-based trucking company files their IFTA form covering operations in Missouri, Oklahoma, and Nebraska, calculating tax liabilities based on state-specific tax rates and total travel metrics.

-

Scenario 2: A fleet manager explores potential fuel credits due to overpayment when estimates were initially higher than actual fuel usage.

Each situation requires precise data tracking and careful adherence to the form's instructions to optimize tax outcomes.