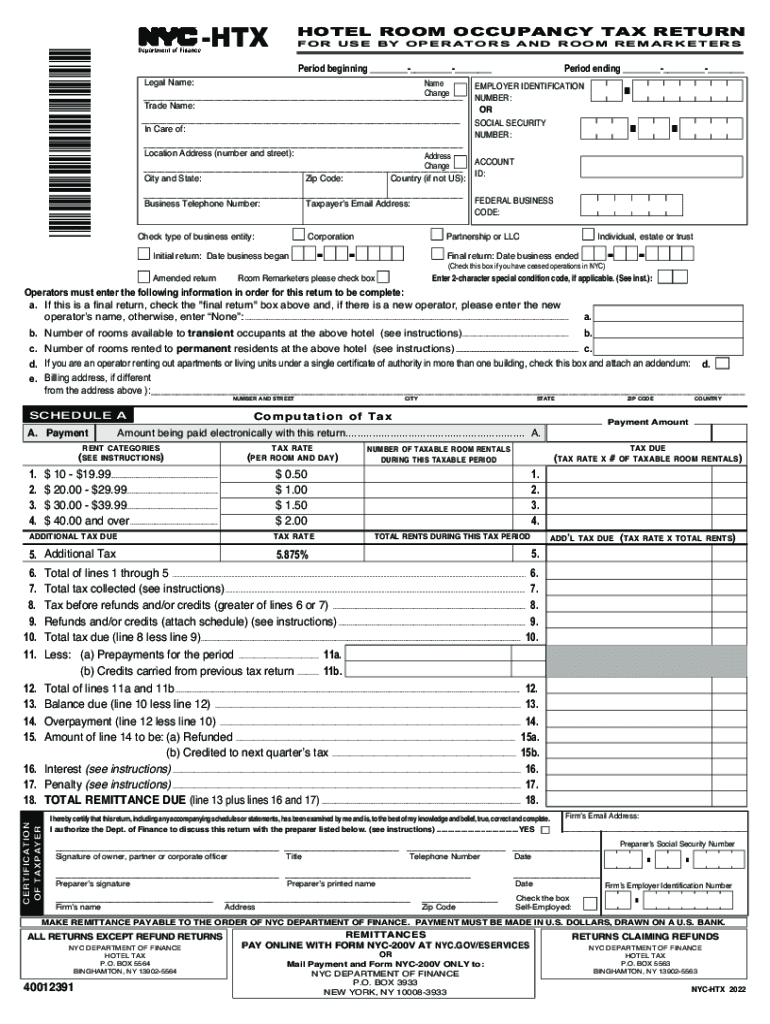

Definition & Meaning

The Request for Ruling Hotel Room Occupancy Tax FLR#024791 is a formal document used by hotel operators and room remarketers to seek clarification on specific tax obligations related to room occupancy. It encompasses the evaluation and interpretation of tax regulations, allowing entities to ensure compliance with New York City's hotel room occupancy tax laws. This form is essential in determining how particular rules apply to unique circumstances, providing businesses with guidance to correctly compute and remit applicable taxes.

Steps to Complete the Request for Ruling Hotel Room Occupancy Tax FLR#024791

- Gather Required Information: Collect all pertinent details about your business, including legal name, business address, and tax identification numbers. Ensure you have comprehensive information about the types of room rentals you offer.

- Understand Tax Regulations: Familiarize yourself with the city-specific rules and recent changes in hotel occupancy tax laws. This will assist in accurately completing the form.

- Complete the Form: Fill out the form with precise information regarding your queries or situations requiring a tax ruling. Provide detailed scenarios or descriptions to facilitate a clear understanding of your request.

- Attach Supporting Documentation: Include any documents that support your request, such as previous tax filings, business contracts, or any correspondence relating to tax obligations.

- Submit the Form: Determine the appropriate submission method, whether online, through mail, or in person, following the guidelines provided by the relevant tax authority.

Who Typically Uses the Request for Ruling Hotel Room Occupancy Tax FLR#024791

- Hotel Operators: Businesses operating hotels in New York City need clarity on how occupancy taxes apply to their specific situations.

- Room Remarketers: Entities involved in reselling room occupancy, such as travel agents or booking platforms, use this form to understand their tax liabilities.

- Tax Professionals: Accountants or legal advisors assisting clients in determining precise tax compliance standards can facilitate filling out and submitting the form.

Key Elements of the Request for Ruling Hotel Room Occupancy Tax FLR#024791

- Legal Name and Business Address: Essential for identifying the entity requesting a ruling.

- Tax Computations and Scenarios: Sections for outlining specific tax questions or scenarios, including detailed descriptions of room rentals.

- Supporting Documentation: A requirement to attach documents that provide evidence or context for the ruling request.

Legal Use of the Request for Ruling Hotel Room Occupancy Tax FLR#024791

This form serves as a formal mechanism to obtain an official interpretation of tax rules applicable to specific business activities within the hotel and accommodation sector. By using this form, businesses can proactively address potential compliance issues and avoid penalties associated with misinterpretation of tax laws. It is legally binding in that it provides a precedent or basis for tax computations once a ruling is issued.

Penalties for Non-Compliance

Failure to obtain or follow a ruling on hotel occupancy tax can result in significant penalties. These might include:

- Fines and Interest: Monetary penalties due to underpayment or late payment of taxes.

- Legal Action: Potential legal proceedings for continued non-compliance or negligence in tax reporting.

- Increased Scrutiny: Enhanced audits or investigations by tax authorities.

State-Specific Rules for the Request for Ruling Hotel Room Occupancy Tax FLR#024791

While this form addresses New York City-specific occupancy tax rules, businesses should be aware of variations in tax regulations if operating in multiple states. Each state may have its own definitions, rates, and filing procedures that impact how hotel occupancy taxes are applied.

IRS Guidelines

Though primarily a state-level tax issue, compliance with the Request for Ruling Hotel Room Occupancy Tax FLR#024791 may also involve alignment with federal tax policies. The IRS provides overarching guidelines for the documentation and reporting of income and expenses related to lodging services, which may impact the information supplied in this request.

Filing Deadlines / Important Dates

Adhering to filing deadlines is crucial to avoid penalties. The specific timing for submitting the Request for Ruling Hotel Room Occupancy Tax FLR#024791 should coincide with any relevant tax reporting periods or changes in business practices. Timeliness ensures that businesses receive the ruling before a tax liability arises.