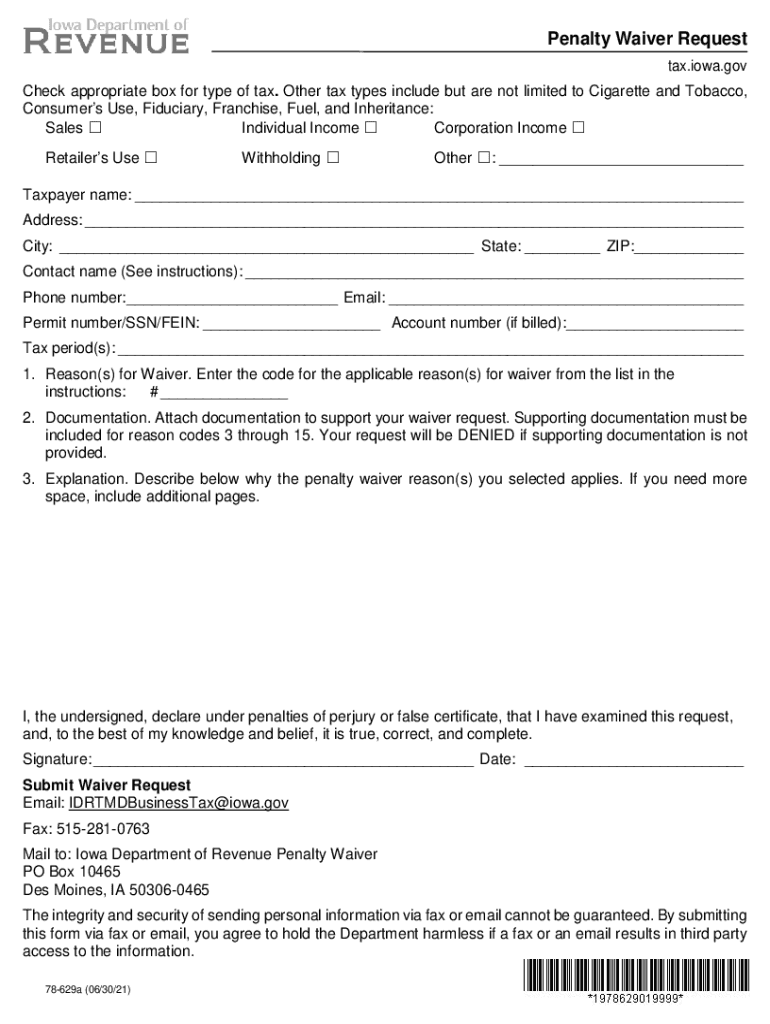

Definition and Purpose of the Penalty Waiver Request 78-629

The Penalty Waiver Request 78-629 form is designed for taxpayers in Iowa seeking relief from penalties related to non-compliance with state tax obligations. This form enables individuals and businesses to formally request the waiver of penalties that have been assessed for various reasons, such as late filings, underpayments, or failure to file tax returns. Understanding the specific requirements and rationale behind this form is crucial for taxpayers looking to navigate the penalty abatement process successfully.

How to Obtain the Penalty Waiver Request 78-629

To access the Penalty Waiver Request 78-629 form, taxpayers can visit the Iowa Department of Revenue's official website. The form can be downloaded directly from the website in a printable format. Alternatively, individuals may request a physical copy by contacting the department via phone or mail, ensuring that all necessary instructions and guidelines are available alongside the form to complete the process accurately.

Steps to Complete the Penalty Waiver Request 78-629

- Gather Required Information: Collect personal details, tax identification numbers, and pertinent tax documents before beginning the form.

- Specify the Tax Type: Indicate the type of tax for which you are requesting a penalty waiver (e.g., individual income tax, corporate tax).

- Explain the Waiver Reason: Provide a detailed explanation of the circumstances leading to the request, including any unavoidable events or errors that contributed to the penalty.

- Attach Supporting Documents: Include relevant documentation to substantiate claims, such as medical records for illness or documentation of natural disasters.

- Review and Submit: Double-check all entries for accuracy before signing and submitting the form via the specified submission method.

Eligibility Criteria for Penalty Waiver

Eligibility for a penalty waiver generally requires demonstrating reasonable cause or substantial justification for non-compliance. Common acceptable reasons include prolonged illness, natural disasters, or reliance on erroneous professional advice. Each case is evaluated individually, with documentation playing a pivotal role in substantiating claims.

Legal Use of the Penalty Waiver Form

Compliance with state tax laws and regulations is essential when using the Penalty Waiver Request 78-629. The form serves as a formal legal document; misrepresentations or false claims may lead to additional penalties or legal consequences. Taxpayers are advised to consult with tax professionals if uncertainty exists about the suitability of their requests.

Key Elements of the Penalty Waiver Request 78-629

- Taxpayer Identification Information: Includes names, addresses, and tax IDs.

- Description of Penalty Type: Specifies the particular penalty the request targets.

- Justification of Request: Details reasons and circumstances for non-compliance.

- Documentation: Supporting evidence that legitimizes the waiver claim.

State-Specific Rules for Iowa

The Iowa Department of Revenue has specific guidelines for evaluating and processing penalty waiver requests. These guidelines reflect the state's policies on tax compliance and penalty abatement and may include specific deadlines, documentation standards, or processing timelines that differ from federal regulations. Awareness of these state-specific rules is crucial for Iowa taxpayers.

Examples of Successful Penalty Waiver Requests

Real-world scenarios highlight various cases where penalty waivers were granted:

- Example One: A taxpayer who missed a filing deadline due to hospitalization successfully provided medical records as evidence.

- Example Two: A small business affected by a significant natural disaster submitted weather reports and insurance claims, resulting in a waiver of penalties for delayed payments.

Required Documentation for Supporting a Waiver Request

- Medical Records: For health-related exemptions, such as surgeries or long-term illness.

- Official Reports: Documents like police or emergency service reports for disasters or theft.

- Professional Correspondences: Communications from advisors or consultants in cases of professional negligence or misinformation.

Understanding these elements and utilizing them effectively increases the likelihood of a successful penalty waiver request, helping taxpayers avoid unnecessary financial burdens.