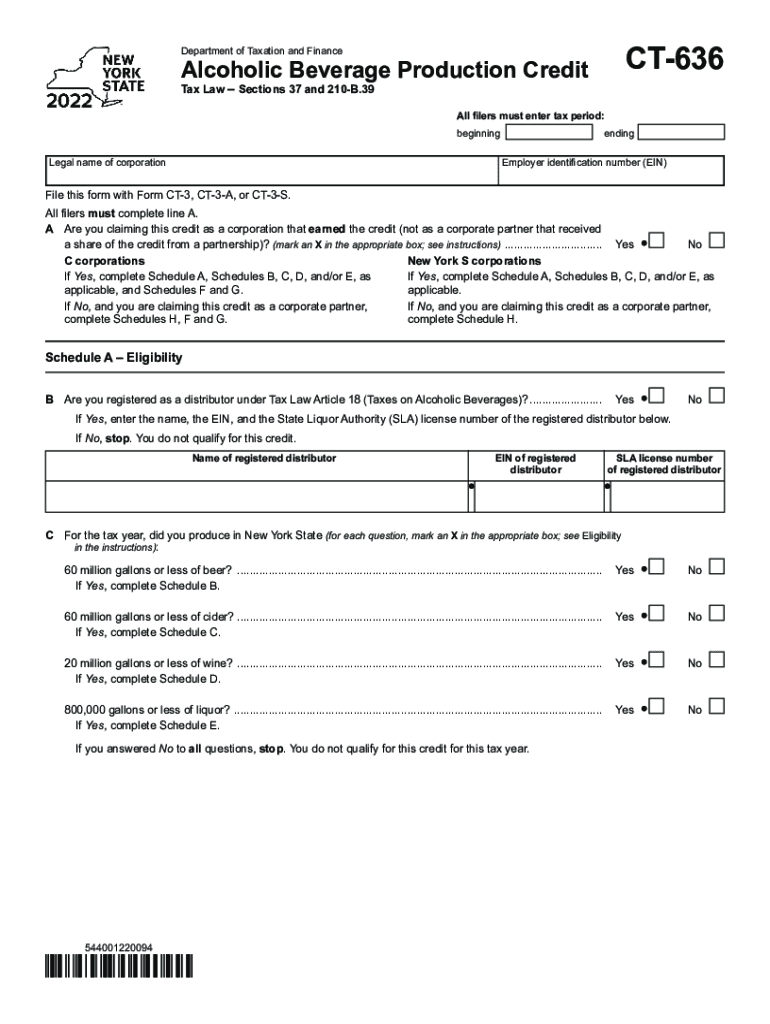

Definition & Meaning

The Form CT-636 Alcoholic Beverage Production Credit Tax Year ... is a tax form utilized by corporations in New York. It is designed to facilitate tax credits based on the production levels of alcoholic beverages such as beer, cider, wine, and liquor. The form allows corporations to claim specific credits, which depend on a structured set of criteria, including production volume and compliance with state regulations. This tax form plays a critical role in managing tax liabilities for businesses engaged in alcoholic beverage production.

Eligibility Criteria

To qualify for the Form CT-636 Alcoholic Beverage Production Credit, businesses must meet several specific requirements:

- Registration as a Distributor: Companies must officially register as distributors of alcoholic beverages in New York.

- Production Thresholds: Companies should produce alcoholic beverages within prescribed limits as set out by the New York State Department of Taxation and Finance.

- Tax Period Compliance: Businesses must adhere to defined tax periods to benefit from the credit. These criteria are crucial in determining the eligibility for claiming the credit, and businesses should evaluate their operations against these benchmarks to ensure compliance.

Key Elements of the Form CT-636

Several key elements define the Form CT-636, outlining the essential components that businesses need to understand:

- Computation Schedules: These are included to assist in calculating the credit amount based on the production levels of alcoholic beverages.

- Specific Sections for Beverage Types: The form is divided into sections addressing the credits for different alcoholic beverages such as beer, cider, wine, and liquor.

- Guidelines for Submission: Detailed instructions on completing and submitting the form, ensuring businesses adhere to procedural requirements. Understanding these elements can significantly impact the accuracy and success of filing for this production credit.

Steps to Complete the Form CT-636

Filling out the Form CT-636 involves several critical steps to ensure all necessary information is accurately reported:

- Gather Necessary Documents: Collect all relevant documentation, including production records and financial statements, supporting the credit claim.

- Complete General Information: Fill in company details, including the legal name and tax identification number.

- Calculate Production Levels: Use the provided schedules to determine applicable credits based on specific production figures.

- Attach Supporting Documents: Include any additional required documents to validate the calculations and declarations made.

- Review for Accuracy: Double-check all entries to ensure compliance with all guidelines. Following these steps helps minimize errors and improves the chance of successfully claiming the production credit.

Important Terms Related to Form CT-636

Understanding specific terms related to the Form CT-636 can assist businesses in accurately completing the form:

- Production Credits: Refers to the financial benefits derived from producing alcoholic beverages under certain conditions.

- Distributor Registration: The process by which a business can become officially recognized as a distributor for tax purposes.

- Computation Schedules: Pre-defined templates that guide corporations in calculating their eligible tax credits. Familiarity with these terms is crucial for navigating the requirements and nuances of the form effectively.

Filing Deadlines / Important Dates

For businesses utilizing Form CT-636, awareness of critical deadlines is vital:

- Annual Tax Filing Deadline: The deadline is generally aligned with the corporation's annual state tax return date.

- Amendment Periods: There are specific periods during which previously filed forms can be amended if errors are discovered.

- State-Announced Changes: Any alterations in filing dates or requirements are often published by the New York State Department of Taxation and Finance. By adhering to these timelines, businesses can ensure prompt and efficient submission of their tax credits.

State-Specific Rules for the Form CT-636

New York enforces several state-specific regulations pertaining to the Form CT-636:

- Production Limits: Defined thresholds exist for various beverage types, dictating the levels at which credits are applicable.

- Differentiated Tax Periods: Specific tax periods must be adhered to according to state law.

- Compliance Requirements: Additional compliance measures may be necessary depending on the beverage type and production locale. These state-specific rules help tailor the form's application to suit New York's legal landscape.

Examples of Using the Form CT-636

Several scenarios illustrate the effective use of Form CT-636:

- Small Brewery: A microbrewery can utilize this form to claim credits on its annual beer production.

- Regional Winery: A winery that meets the production criteria can reduce its tax burden by accurately reporting wine production.

- Cider Mill: Companies producing cider in significant quantities may also benefit from this credit, provided they comply with outlined thresholds. These examples underscore the varied applicability of the form across different segments of the alcoholic beverage industry.

Legal Use of the Form CT-636

Ensuring the form's legal utilization involves strict adherence to established procedures:

- Accurate Representation: All reported production figures must reflect true volumes to prevent legal repercussions.

- Audit Readiness: Corporations should maintain readily accessible records that substantiate all credit claims in case of a state audit.

- Compliance Adherence: Businesses must comply with all state laws, ensuring full legal adherence when claiming credits. These legal stipulations are in place to uphold the integrity and proper usage of the tax credit system.