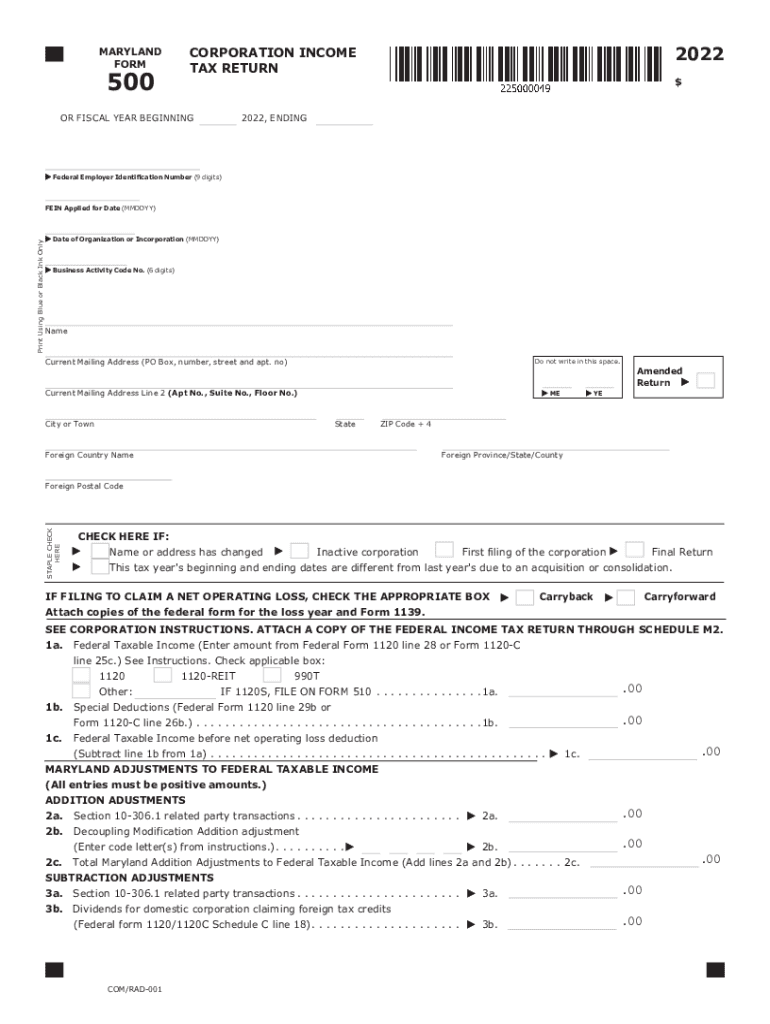

Definition and Purpose of the Corporation Income Tax Return

The Corporation Income Tax Return is a formal document required by the Internal Revenue Service (IRS) for corporations operating within the United States. This form serves as the primary method for corporations to report their income, gains, losses, deductions, and credits to determine their annual income tax liability. The form is essential for maintaining compliance with federal tax laws, and failure to submit it accurately and on time can result in significant penalties.

- Federal Tax Obligations: Corporations must report their federal taxable income derived from all sources and apply applicable deductions and credits.

- Compliance and Transparency: Ensures corporations are transparently disclosing their financial activities to the government.

- Financial Insights: Provides a detailed financial overview of a corporation's fiscal year, influencing strategic business decisions.

Steps to Complete the Corporation Income Tax Return

Completing the Corporation Income Tax Return requires a thorough understanding of both financial information and tax regulations. Here is a detailed step-by-step guide:

- Gather Financial Documents: Collect statements, receipts, and previous tax returns.

- Calculate Federal Taxable Income: Start by determining the total revenue and subtracting deductible expenses.

- Adjust Income for State Requirements: Adjustments may be necessary based on state-specific tax laws.

- Complete Deductions and Credits Sections: Identify all applicable deductions and available tax credits.

- Review and Double-Check Entries: Ensure all information is accurate and complete before submission.

- Submit the Form: Forms can be submitted electronically or via mail as per IRS guidelines.

Who Typically Uses the Corporation Income Tax Return

The form is utilized by various types of corporate entities that operate within the U.S. that need to report their annual income tax information:

- C Corporations: Regular corporations subject to corporate income tax.

- S Corporations: Must submit different forms but may use information from the Corporation Income Tax Return for state-level reporting.

- Foreign Corporations: If conducting business or deriving income in the U.S.

- Financial Institutions and Banks: Required for federal compliance.

Key Elements of the Corporation Income Tax Return

Several essential components make up the Corporation Income Tax Return:

- Federal Employer Identification Number (FEIN): Unique identifier used for all tax filings.

- Business Activity Code: Provides information on the primary business activity.

- Income and Deductions: Detailed sections for income statement components.

- Tax Computation and Credits: Outlines the calculation of tax liability and any applicable credits.

- Authorization: Signatures of authorized individuals ensuring accuracy and responsibility.

Important Terms Related to Corporation Income Tax Return

Understanding specific terminology is crucial for accurately completing the form. Here are some important terms:

- Apportionment of Income: Process of determining taxable income for states where the corporation operates.

- Deferred Income Tax: Taxes incurred but not payable within the current fiscal year.

- Schedule M-1 Adjustments: Reconciles book income with taxable income.

Filing Deadlines and Important Dates

Ensuring timely submission is critical for compliance:

- Annual Filing Deadline: The deadline is typically the 15th day of the fourth month following the end of the corporation's fiscal year, commonly April 15 for calendar year taxpayers.

- Extension Requests: Corporations can file for an extension using IRS Form 7004, which grants an additional six months.

- Estimated Tax Payments: Corporations must make quarterly estimated tax payments to avoid penalties.

Required Documents for Submission

To complete the Corporation Income Tax Return accurately, prepare the following documents:

- Income Statements and Balance Sheets: Essential for calculating taxable income.

- Previous Tax Returns: Useful to reference for consistency and verification.

- Receipts and Invoices: Support claims for deductible expenses.

- Salary and Payroll Records: Necessary for payroll tax deductions.

Penalties for Non-Compliance

Corporations must adhere to IRS regulations to avoid hefty penalties:

- Late Filing Penalties: Failure to file on time results in penalties up to 5% of the unpaid taxes for each month, up to a maximum of 25%.

- Accuracy-Related Penalties: Up to 20% of the underpayment due to negligence or substantial understatement.

- Interest Charges: Imposed on unpaid taxes from the original due date until payment is made.

Digital vs. Paper Version of the Form

Corporations have options when it comes to submitting their tax returns:

- Digital Submission: The electronic option is faster, facilitates error checking, and provides immediate confirmation.

- Paper Submission: Traditional method, though slower and subject to manual checking delays.

- Software Compatibility: Many tax preparation software programs are compatible with the IRS e-file system, improving accuracy and efficiency.