Definition & Meaning

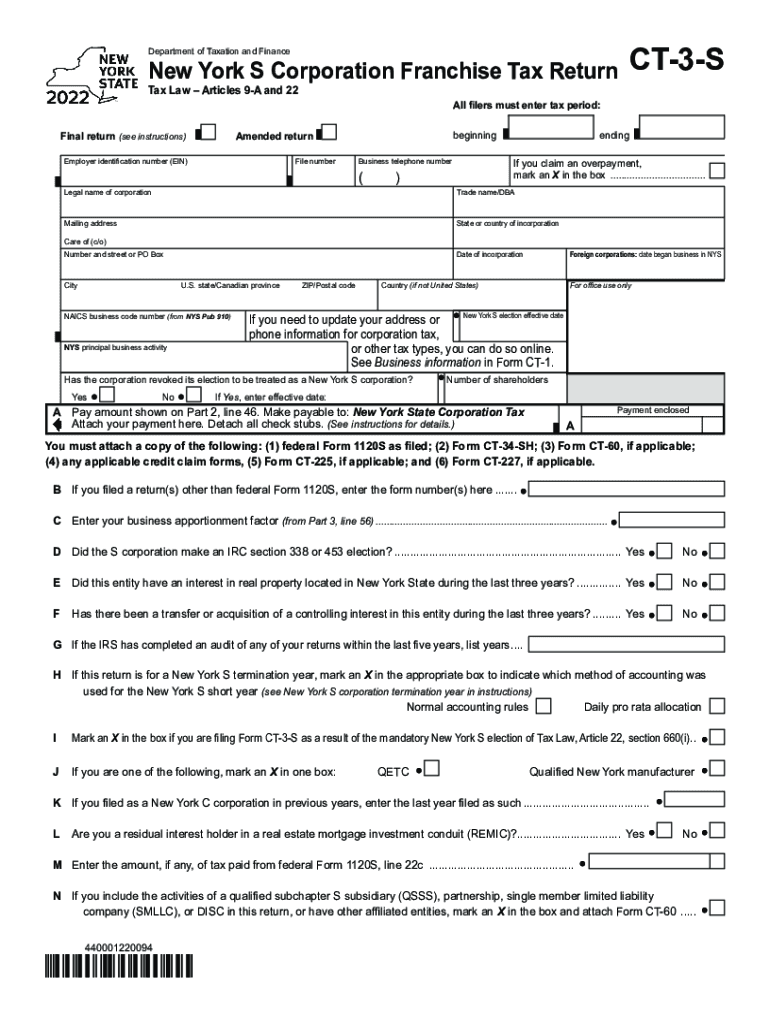

Form CT-3-S, the New York S Corporation Franchise Tax Return for Tax Year 2022, is a tax form used by S corporations operating in New York State to report their franchise tax obligations. This form is a critical component for S corporations to maintain compliance with state tax requirements, ensuring they accurately report their income, deductions, and various tax credits applicable under New York State law. The primary purpose of this form is to determine the tax liability of the S corporation based on its New York source income.

Steps to Complete the Form CT-3-S

- Gather Required Information: Collect detailed records of the corporation's income, expenses, assets, and liabilities for the tax year 2022.

- Fill in Corporate Information: Enter the corporation's legal name, address, employer identification number (EIN), and business activity description on the top of the form.

- Report Income and Expenses: In the income section, detail the corporation's gross income and allowable deductions. Ensure accurate computation to avoid discrepancies.

- Calculate Tax: Use provided guidelines to compute the franchise tax. Include any apportionment factors if the corporation operates both within and outside New York State.

- Review and Attachments: Attach necessary schedules and forms, such as those for credits or previous year overpayments.

- Submit: Ensure the form is signed by an authorized officer of the corporation before submission.

Who Typically Uses the Form CT-3-S

This form is mainly used by S corporations doing business in New York State. These entities have elected S corporation status for federal tax purposes, allowing income, losses, deductions, and credits to flow through to shareholders. Companies that primarily benefit from this form include those looking to handle state-specific tax responsibilities while enjoying the federal tax benefits of a pass-through organization.

State-Specific Rules for the Form CT-3-S

New York State imposes specific rules on S corporations, including unique apportionment standards depending on the nature and location of the business activity. S corporations must understand these localized rules to accurately complete Form CT-3-S. For example, there may be different calculations for businesses operating across state lines or engaging in particular industries.

- Unique apportionment rules may apply based on business location.

- Specific credits may be available depending on industry and investment activities.

- Failure to comply with state-specific regulations could result in penalties or additional taxes.

Key Elements of the Form CT-3-S

- Corporate Details: Essential information on the business, including legal structure and state operations.

- Income Lines: Sections dedicated to gross receipts and deductions.

- Tax Computation: Fields for calculating franchise tax liability.

- Schedules and Attachments: Required additional documents for credits and specific exemptions.

- Signature and Declaration: Authorization section for final sign-off by a corporate officer.

IRS Guidelines

While the primary jurisdiction for Form CT-3-S is New York State, federal regulations influence parts of the filing process. The IRS requires that S corporations maintain certain records that align with federal tax submissions, which in turn affect the accurate completion of state tax returns.

- Ensure alignment between federal and state submissions.

- Understand federal definitions of income and deductions that affect state taxes.

- Utilize IRS guidelines to verify shareholder allocations and profit distributions.

Filing Deadlines / Important Dates

For the 2022 tax year, Form CT-3-S should be filed by March 15, 2023, coinciding with the federal S corporation tax filing deadline. For corporations on a different fiscal year, the form is due on the 15th day of the third month after the end of the corporation's tax year.

- Late submissions possibly incur penalties.

- Extensions might be available in specific situations, requiring additional form submission.

Form Submission Methods

Form CT-3-S can be submitted electronically through the New York Department of Taxation and Finance's online services or mailed to the specified address. Each method comes with its recommendations:

- Online Submission: Quicker processing and confirmation of receipt.

- Mail Submission: Ensure sufficient postage and use certified mail for record-keeping.

- In-Person Submission: Possible at designated state offices, though less common for this form type.

Penalties for Non-Compliance

Failing to file the Form CT-3-S in a timely manner or submitting inaccurate information can result in fines, interest on owed taxes, and other legal consequences. New York State imposes stringent penalties to ensure compliance:

- Monetary fines based on outstanding tax liabilities.

- Interest charges from the original due date to the payment date.

- Potential audits and further investigation by the tax authority.

Required Documents

Having the right documents ready before completing the form significantly simplifies the process. These typically include:

- Income Statements: Detailed records of revenue and expenses.

- Balance Sheets: For accurately reporting financial position.

- Supporting Schedules: For credits, deductions, and modifications.

- Corporate Officer List: Contact information for responsible parties.