Definition & Meaning

"Your Insurance Card or Other Document" refers to the official document provided by insurance companies and government programs like Medicaid or CHIP. These documents are crucial for accessing healthcare services and understanding one's health plan details. Typically, they contain vital information like the member's name, unique member ID, group number, and plan type. Insurance cards serve as proof of insurance and assistance in communicating with healthcare providers, ensuring that the correct benefits and coverage are utilized.

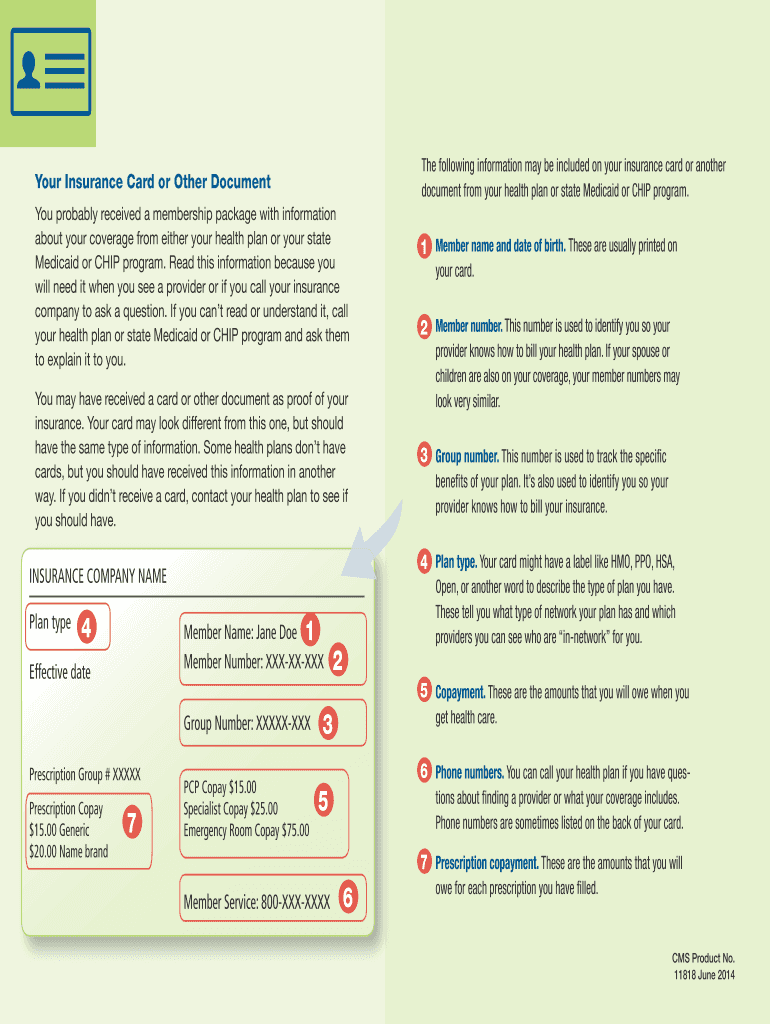

Key Elements of the Insurance Card

Insurance cards generally include several key elements that are essential for both the policyholder and the healthcare providers. They typically feature:

- Member Name and ID: Identifies the policyholder and enables easy retrieval of insurance details.

- Group Number: Associates the policyholder with a specific health plan or employer group.

- Plan Type: Indicates the nature of the insurance coverage, such as Preferred Provider Organization (PPO) or Health Maintenance Organization (HMO).

- Copayment Information: Specifies the out-of-pocket costs for different services, helping policyholders understand their financial responsibilities.

- Insurance Company Contact Information: Provides a direct line for verifying coverage details or addressing issues.

Steps to Use Your Insurance Card

Using your insurance card effectively involves several steps to ensure proper use and understanding of your health coverage:

- Ensure Card Accuracy: Confirm that all personal and coverage details are correct and up to date.

- Present at Medical Visits: Show your card during healthcare appointments to verify coverage and benefits.

- Verify Network Providers: Contact your insurer or use their website to confirm that your doctor is in-network, which can affect the cost of services.

- Understand Copayments: Be aware of your copayments for office visits, emergency care, and prescriptions, which are often listed on the card.

- Reach Out for Clarifications: Utilize the contact information on the card for any queries about your coverage.

How to Obtain Your Insurance Card

Obtaining an insurance card is a straightforward process upon enrolling in a health insurance plan. Here’s how to acquire it:

- Enrollment in a Plan: Once enrolled in an insurance plan, either through an employer, private insurer, or government program, an insurance card is generated.

- Await Direct Mailing: Insurance cards are typically sent by mail; however, electronic versions might also be available via email or the insurance provider’s website.

- Replacing a Lost Card: Request a replacement through your insurance provider's website or by contacting their customer service if you misplace your card.

Important Terms Related to Insurance Cards

Understanding several technical terms related to insurance cards can enhance the user’s grasp of their benefits:

- Premium: The regular fee paid for the insurance coverage.

- Deductible: The amount the insured must pay out-of-pocket before the insurance company begins coverage.

- Out-of-Pocket Maximum: The total a policyholder would be responsible for during a policy period, after which the insurer covers 100% of allowed amounts.

- Network Providers: Healthcare providers who have an agreement with the insurer to offer services at discounted rates.

Digital vs. Paper Version

Both digital and paper versions of insurance cards are used today, offering different benefits and functionality:

- Paper Version: Traditional, easy to present during visits but susceptible to being lost or damaged.

- Digital Version: Often available through insurance apps or online accounts, digital versions are easily accessible on smartphones and reduce the need for physical storage, although they require an electronic device for use.

Legal Use of Your Insurance Card

Insurance cards must be used legally, respecting all prescribed norms:

- Insurance Fraud Prohibition: Using another person’s insurance card or allowing someone to use yours for unauthorized services is illegal.

- Verification of Identity: Always ensure that services rendered under your insurance card match your identity and accurate personal details.

- Updates and Renewals: Ensure timely updates or renewal of your insurance card details when there are changes in employment, marital status, or basic personal information.

State-Specific Rules

Some states have specific rules affecting insurance cards, such as:

- Minimum Coverage Requirements: Certain states may require insurance policies to meet specific minimum criteria for benefits.

- State-Sponsored Programs: Programs like Medicaid can have varying conditions based on state, including different eligibility thresholds and coverage limits.

- Provider Networks: The range of in-network providers can differ significantly from state to state, affecting the copayment and coverage for services.

Examples of Using Your Insurance Card

Real-world scenarios highlight the importance of insurance cards:

- Routine Check-ups: Using your card for annual wellness visits can ensure coverage for preventive services without out-of-pocket costs.

- Emergency Situations: Presenting your card upon emergency room admission ensures that the hospital has the necessary details to process claims swiftly.

- Medication Purchases: At pharmacies, insurance cards facilitate verification of prescription coverage and copayment processing.

Form Submission Methods: Online vs. Mail

Submitting applications and claims associated with your insurance card can be done through various methods:

- Online Submission: Offers convenience, faster processing, and status tracking through insurer portals or apps.

- Mail Submission: Still a viable method for those who prefer paper documentation or lack consistent internet access; however, it often requires longer processing times.

Form Variants: Related Documents

Different types of related documents to the insurance card include:

- Additional ID Cards: Cards for dependents or additional members covered under the same policy.

- EOB Statements: Explanation of Benefits, detailing recent healthcare services received and the insurer’s payment.

- Claim Forms: Necessary for reimbursement in certain situations, such as when seeking care from out-of-network providers.

Who Issues the Form

Insurance cards are issued by various entities depending on the nature of the insurance:

- Private Insurance Companies: Such as Aetna, Cigna, or UnitedHealthcare.

- Employer-Sponsored Plans: Typically managed by Human Resources departments in collaboration with private insurers.

- Government Programs: Including Medicare, Medicaid, or CHIP, managed through applicable state or federal agencies.